Key events in EMEA next week

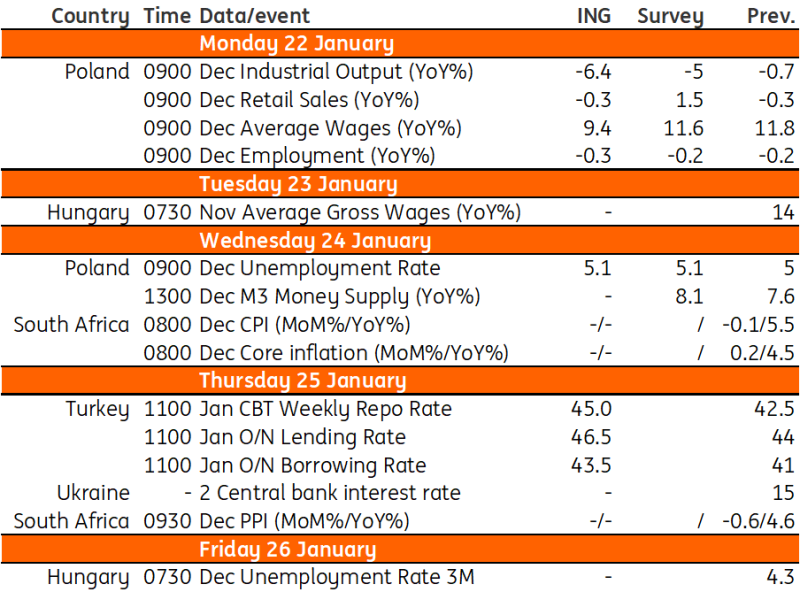

Next week brings a flurry of data releases in Poland, including the unemployment rate, which increased to 5.1% after running at an all-time low of 5% since July. The Central Bank of Turkey has signalled that its tightening cycle will be completed as soon as possible, and we expect one more hike by 250bp in the January MPC meeting

Poland: Unemployment rate inches up to 5.1% after running at all time lows since July

Industrial output (December): -6.4% YoY

After some encouraging signs in the beginning of the fourth quarter of last year, industrial output weakened again afterwards as global manufacturing remains under pressure and external demand remains soft. We project awful December reading, amplified by negative calendar effects. Industry remains the weakest spot of the economy and is the main drag to economic recovery that in the fourth quarter was slower than we had expected.

Retail sales (December): -0.3% YoY

While real disposable income of households has improved alongside falling inflation, consumer demand rebound remains slow. Our estimates suggest that the winter holiday period didn't bring much good news for retailers. We still see household consumption rebounding in 2024, but the pace of recovery was weak towards the end of 2023. Demand for durable goods is particularly soft, with the exception of car sales.

Wages (December): 9.4% YoY

December is traditionally a month of bonus payments in mining, but last year, some of those payments had already taken place in October. If this reduces December payments, we may see a temporary slowdown in average wage growth to a single-digit pace amid a high reference base. Nevertheless, robust wage growth is expected to continue this year. From 1 January the minimum wage went up from PLN 3600 a month to PLN 4242 a month (gross). In the 2024 state budget, the government plans a 30% wage increase for teachers and 20% for civil servants.

Employment (December): -0.3% YoY

We forecast further easing in the enterprise employment level in December and negative annual readings are here to stay for quite some time. The scale of deterioration is negligible given the recent performance of the economy and the negative output gap, confirming that structural factors (i.e., unfavourable demographics) keep the labour market tight.

Unemployment rate (December): 5.1%

Our forecast and the Ministry of Family Labour and Social Policy estimates both point to a slight seasonal increase in the number of those unemployed in December last year. As a result, the registered unemployment rate inched up to 5.1% after running at all-time-low of 5.0% since July.

Turkey: We expect one more hike by 250bp to 45% in January MPC

Last month, the Central Bank of Turkey provided guidance that its tightening cycle would be completed as soon as possible. The bank also reiterated that the monetary tightening required for the sustained price stability would be maintained as long as necessary. Accordingly, we expect one more hike by 250bp to 45% in the January MPC metting, and then for the central bank to remain mute until the late third quarter or early four quarter of the year.

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

19 January 2024

Our view on next week’s key events This bundle contains 3 Articles