Key events in EMEA next week

Next week in Poland, we will see the release of core inflation, industrial output, and employment data. We expect inflation to continue to moderate while the labour market should remain tight. In Turkey, we expect the central bank to wait for March inflation data to decide on a rate move, though the possibility of policy strengthening has increased

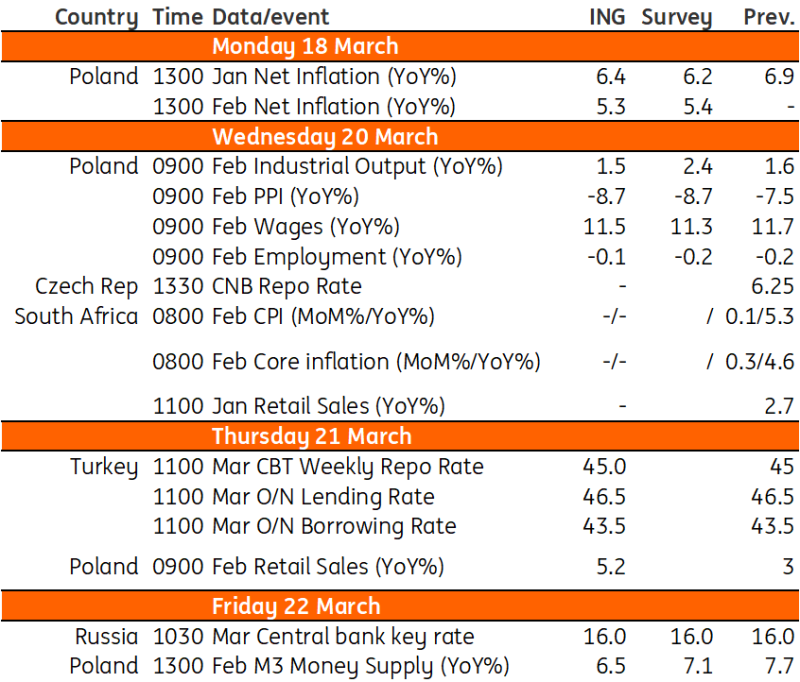

Poland: Inflation expected to moderate as the labour market remains tight

Core inflation (Feb): 5.3% YoY

After an annual update of the CPI basket weights, the National Bank of Poland will publish January and February core inflation data. We forecast that core inflation excluding food prices continued to moderate in early 2024, mainly due to the high reference base from early 2023, but momentum likely remained elevated. According to our estimates, core inflation fell from 6.9% year-on-year in December 2023 to 6.4% YoY in January and 5.3% YoY in February this year. Over the medium term, we see core inflation boosted by a tight labour market which translates into robust wage growth and buoyant services prices.

Industrial output (Feb): 1.5% YoY

According to our forecasts, industrial output growth remained subdued in February, although recent PMI readings give some hope of recovery. At the same time, the picture for the European industrial sector remains dismal. Exporters are also under increasing pressure from the zloty strengthening and competition from cheap imported goods.

PPI (Feb): -8.7% YoY

Producer prices continue falling and PPI deflation is substantial in annual terms reflecting, among other things, global deflationary pressure from tradable goods and declining energy prices after an earlier shock. We estimate that manufacturing prices were little changed vs. January, but substantial month-on-month price declines took place in mining and energy supply. We project PPI deflation to continue in the coming months.

Wages (Feb): 11.5% YoY

Wages in the enterprise sector continue to rise at a double-digit pace. The labour market remains tight and the scarcity of labour, along with high minimum wage increases, puts upward pressure on wages. It is yet to be seen whether or not the 20% increase in wages in the public sector and 30% hike in wages for teachers will have a ripple effect on the enterprise sector (competition for workers).

Employment (Feb): -0.1% YoY

The annual update of the enterprises sample did not introduce any significant changes in employment trends from January. The level of employment remains little changed and we expect it was only slightly lower than in February last year. Supply-side constraints are still the predominant factor curbing employment growth, but demand for labour also cooled in some industries. Still, the labour market remains tight and unemployment in Poland is among the lowest in the EU.

Retail sales (Feb): 5.2% YoY

We expect continued improvement in retail sales on the back of robust growth of real disposable incomes of households (lower inflation, continued double-digit growth in wages). The rebound is somewhat restrained by the higher propensity to save, but we judge that the scale of income growth leaves enough room for both higher spending and savings to be rebuilt. In our view, household consumption will be the main driver of economic growth this year.

Turkey: We expect the CBT to wait for March inflation data

After an acceleration in the exchange rate lately, the Central Bank of Turkey responded by introducing additional macro-prudential measures and increased liquidity sterilisation efforts. Accordingly, financial conditions have started tightening again, with upward pressure on lending and deposit rates. Annual inflation, meanwhile, was higher than expected in February standing at 67.1% on the back of an across-the-board increase in prices. We expect that the CBT will prefer to wait for the March inflation data before deciding on any rate move and should remain on hold this month, though a possibility that the policy response might be strengthened by an additional 250bp rate hike has also increased with recent developments.

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

15 March 2024

Our view on next week’s key events This bundle contains 3 Articles