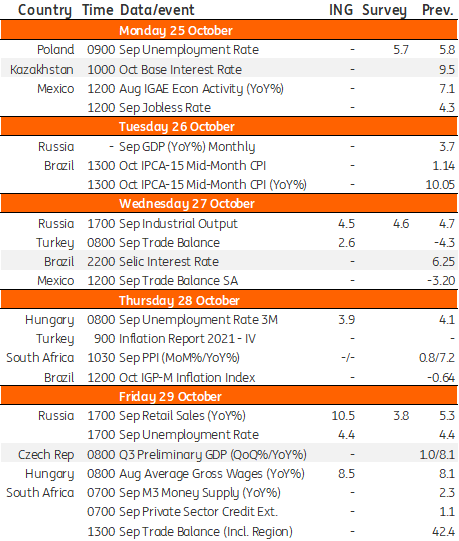

Key events in EMEA next week

Increased social payments could increase retail sales in Russia, whilst global supply chain disruptions will continue to weigh on industrial production. In Hungary, the lack of labour will drive wage growth in the near future.

Russian economic activity for September affected by one-offs

Russian economic activity data for September should be distorted by a massive RUB700 bn (0.6% GDP) social payments disbursement, ahead of the parliamentary elections. We do not discount the possibility that retail trade growth might show material but temporary acceleration in September vs. the 5.3% YoY increase seen in August.

Meanwhile, the picture for industrial production is mixed, as the commodity extraction sectors might benefit from the easing of OPEC+ constraints and higher global demand for other commodities. However, locally-focused manufacturing could suffer from the limited supply of intermediary and investment imports because of disruptions to global supply chains.

For 4Q21 we expect moderation in the local economic growth, outside of the export-focused sectors, as the catch up with pre-pandemic levels of activity is largely over. The budget and monetary policy signals are not very supportive, and the epidemic situation in Russia has worsened. This is causing the government to re-introduce soft restrictions in the form of non-working days in the first week of November. The latter should not have a sizeable impact on activity, as non-working days are legally less restrictive as regular weekends and holidays, and the first week of November already has 2 official public holidays.

Nevertheless, the current situation of record-high new Covid cases and record-high mortality, along with a sluggish vaccination rate, is a reminder of the medium-term risks to the local economic growth trend. For the local policy mix, this is complicated by the fact, that the global inflationary picture is deteriorating, which prevents the local central bank from easing its approach.

Hungary: Stronger wage growth expected as labour supply issues continue

In Hungary next week it is all about the labour market data. More and more companies are complaining about the lack of labour. In this respect, we don’t expect a swift change in the unemployment rate, only a gradual improvement to 3.9%. When it comes to wages, the labour shortage is pushing wage growth higher, especially in August, when a lot of seasonal work started in agriculture. The accommodation and hospitality sectors are also facing an uphill battle when it comes to wage settlements for newcomers. As a result, we expect the trend in wage growth to strengthen.

EMEA Economic Calendar

Download

Download article

22 October 2021

Our view on next week’s key events This bundle contains 3 ArticlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more