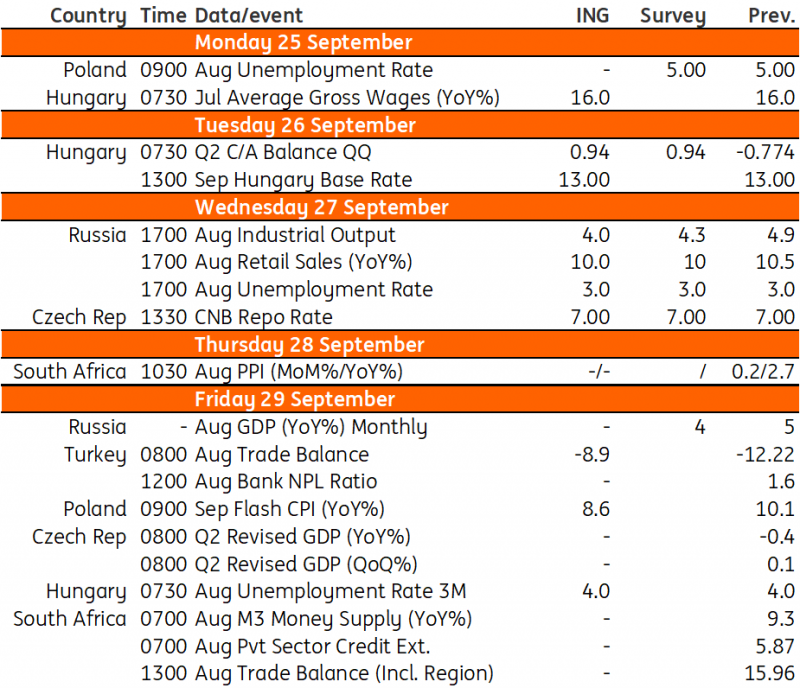

Key events in EMEA next week

The Czech National Bank will hold its monetary policy meeting next week. In Hungary, we expect the central bank to merge the key and effective rates at 13%. Further sharp declines in annual inflation are expected in Poland in September

Czech Republic: the debate on rate cuts begins

The Czech National Bank (CNB) will hold its monetary policy meeting next Wednesday, which we believe will be the last meeting before it begins to discuss the real possibility of rate cuts. This time there will be no new central bank forecast and the board will only discuss an internal update on the situation. For now, it seems that the CNB may be happy with the numbers coming out of the economy. Board members have already indicated that the September meeting will be used to discuss the rate-cutting strategy, so we could see some details from this discussion. In any case, the CNB will try to sell future rate cuts with a hawkish and cautious tone.

Our forecast remains unchanged – a first 25bp rate cut in November alongside a new central bank forecast. Of course, the risks here are clear. The central bank could wait for the January inflation number and cut rates at the start of next year. However, we believe that the combination of faster-falling inflation, weak economic numbers and FX at current or stronger levels will be a reason for the board to cut rates in November and avoid too much monetary tightening and inflation near the target in January.

Hungary: September rate-setting meeting

The key event in Hungary next week is the National Bank of Hungary's (NBH's) September rate-setting meeting. We expect the central bank to merge the key and effective rates at 13%, ending phase one of normalisation. We don't expect any groundbreaking changes in the forward guidance. This means that the tone will remain generally hawkish, leaving all options open; from a pause to a 100bp cut at the upcoming meetings, as the decision-making process is now agile and data-driven.

We can expect a lot of market volatility as the markets may feel some disappointment, but to be fair, this September meeting won't be able to bring any more hawkish action to the table and words alone won't be enough for the markets to rethink their rate cut expectations, which were deemed excessive by the NBH last time.

Besides the monetary policy event, we will see the latest labour market data, where the big picture will remain unchanged, showing strong nominal wage growth and a relatively low unemployment rate despite the four-quarter technical recession. The current account will move into surplus on the basis of preliminary monthly data, showing a marked improvement in external balances.

Poland: further sharp declines expected in annual inflation

Unemployment (August): 5.0%

Data from the Ministry of Family and Social Policy indicate that the number of registered unemployed barely changed in August versus July. That confirms our estimate that the unemployment rate remained unchanged at 5.0%. The labour market remains tight due to unfavourable demographics.

Flash CPI (September): 8.6% YoY

A further sharp decline in annual inflation is expected in Poland in September – to 8.6% year-on-year from 10.1%YoY in August. Several factors are expected to contribute to disinflation in September apart from the high reference base from September 2022, when prices went up by 1.6% month-on-month.

First, we expect further month-on-month declines in food prices. Second, the government lifted the limit on electricity consumption which qualifies for a price freeze for households. Third, the price policy of the main national supplier of gasoline and diesel has resulted in lower prices at the pumps, despite mounting crude oil prices and a weaker zloty versus the US dollar.

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

22 September 2023

Our view on next week’s key events This bundle contains 3 Articles