Key events in EMEA next week

In the EMEA region this week, we expect the Turkish Central Bank to raise its policy rate. In Poland, recent rapid disinflation may have led to outright deflation in July

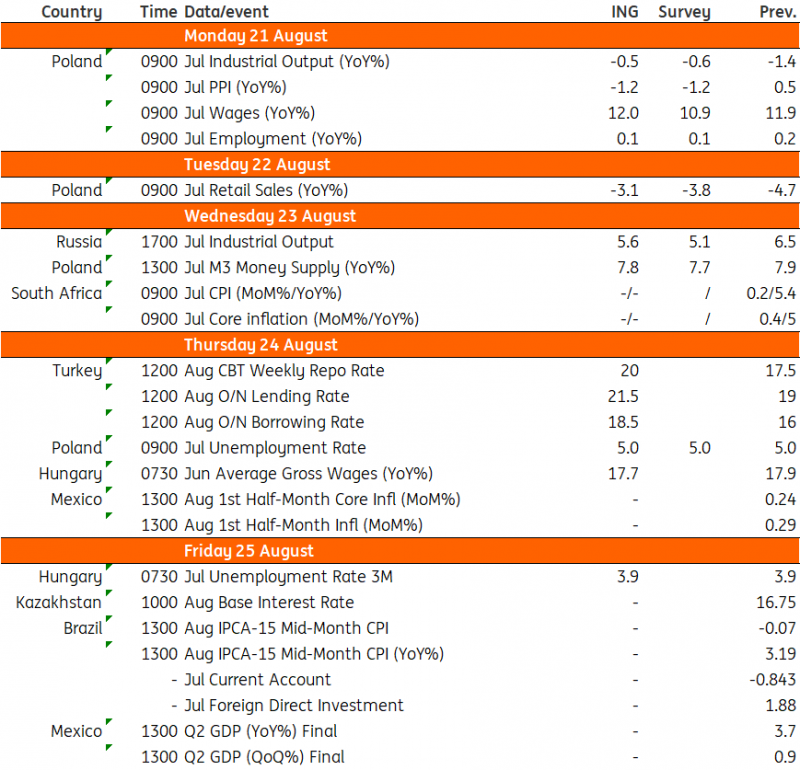

Turkey: Central bank expected to raise the policy rate

We expect the Turkish Central Bank to raise the policy rate (one-week repo rate) by 250bp to 20% on 24 August. Since the start of the ongoing policy shift to a more orthodox stance, the bank has hiked by 900bp from 8.5% and taken initial steps to ease “liraisation” targets and security maintenance requirements, but the macro-prudential policy framework is still largely in place.

Whether the appointment of new members to support the policy shift will lead to a revision in the pace of tightening will be more evident at this month's Monetary Policy Committee meeting.

Hungary: Labour market data take centre stage

In Hungary, the upcoming week is about the labour market and we don’t see any significant surprises here. Wage growth will remain sound on the back of the ongoing labour shortage (especially in manufacturing and leisure-related sectors). However, it will still lag inflation and we expect to see the continued deterioration of household purchasing power.

The latest unemployment rate will reflect an unusually tight labour market in a four-quarter technical recession. As employers are still hopeful that better days are ahead, they are trying to keep the labour in-house even if it means they need to give up some profit. The mindset is that during a boom, the structural labour shortage will put those who are laying people off now in a difficult situation when they want to fill roles again.

Poland: Industrial output seems to be bottoming out

Industrial output (July): -0.5% year-on-year

Poland’s industrial output seems to be bottoming out, but recent developments in China (the general economic slowdown) and Germany (the poor performance of industry) has increased the risk of further weakness of Polish manufacturing in the coming months. New orders paint a bleak outlook for future output. At the same time, the most acute phase of destocking is probably behind us. Surveys and leading indicators are mixed. On the one hand, businesses declare they expect improvement in economic conditions in the third quarter, but at the same time foresee softer demand in the months ahead. We project industrial output to remain subdued in the third quarter and experience a more visible rebound in the fourth quarter.

PPI (July): -1.2% YoY

We forecast that recent rapid disinflation has led to outright deflation in July. Prices in manufacturing have been falling on a monthly basis since November 2022 and are lower than a year ago. Declines in energy prices (coal, oil) play an important role in the turnaround in producer prices. We expect PPI deflation to prevail until at least the end of 2023, which should facilitate a further decline in CPI inflation given the lag between the two gauges of prices.

Wages (July): +12.0% YoY

Wages growth in the enterprise sector has stabilised around 12%YoY in recent months. Despite a high reference base from July 2022, we still project a 12%YoY wage increase in July this year due to high bonuses in mining as employees benefited from the exceptional profitability of the sector in 2022. We expect wage growth to continue rising at a double-digit pace over the medium term due to shortages of labour supply and a substantial increase in the minimum wage in 2024.

Employment (July): +0.1% YoY; Unemployment (July): 5.0%

We forecast that in July, employment in the enterprise sector was at a similar level to a year ago. The level of employment has been declining slightly in recent months and stalled in July. Still, the registered unemployment rate remains low and in July it stood at 5.0%, i.e. at the same level as in June.

Retail sales (July): -3.1% YoY

According to our forecasts, July was yet another month of decline in retail sales of goods, but the situation seems to be stabilising as lower inflation has allowed for a return of real growth in wages. The gap between nominal and real sales narrowed, pointing to slowing goods inflation. But, we expect a visible improvement in household consumption in the fourth quarter as the real purchasing power of households improves further.

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

18 August 2023

Our view on next week’s key events This bundle contains 3 Articles