Key events in EMEA next week

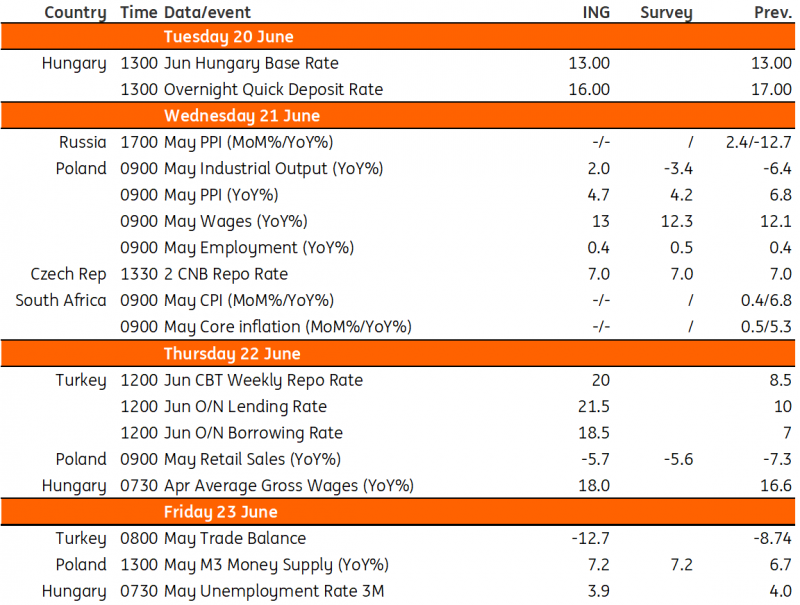

The Czech National Bank is due to meet on Wednesday with rates expected to remain unchanged, although the governor will still be pushing a hawkish message. The National Bank of Hungary meets as well, with 100bp cuts to the top-end of the interest rate corridor expected

Hungary: 100bp cuts to the top-end of the interest rate corridor and to the effective rate

The highlight of the week is the National Bank of Hungary’s rate-setting meeting. Though EUR/HUF is now at a higher level than a week or so ago, on a monthly comparison, nothing has changed. Forint was around 375 versus the euro when the Monetary Council met last time. In this regard, FX market stability won’t be an issue when it comes to the continuation of the effective rate-cut cycle.

Other submarkets (bonds, swaps) are behaving well and the general market sentiment is supportive as well. Indicators of external balances are improving, while disinflation accelerated in May. This looks like a perfect setup for a “copy-paste” decision on 20 June. We see 100bp cuts to the top-end of the interest rate corridor and to the effective rate (the overnight quick deposit tender). The latter will sit at 16%.

The forward guidance and the tone will remain unchanged as well, in our view. This means that the approach remains cautious and gradual and the decisions ahead are still data and sentiment driven with the base case (if everything goes well) being the continued easing until the merger of the base rate and the effective rate at 13%. Other than this, we can focus on the labour market data in Hungary, where we expect a negligible improvement. Here we point to technical factors (the dropping unemployment rate) and labour shortage (accelerating wage growth) as the main drivers.

Turkey: Key rate expected to be 20% at the June MPC meeting

Following the appointment of new names to the Ministry of Treasury and Finance and the Central Bank of Turkey (CBT) in the aftermath of the elections, expectations for a pivot towards more conventional monetary policy have increased significantly. Accordingly, given that the 12M inflation expectation is at almost 30% in the Market Participants Survey of the CBT, and assuming that an adjustment in the policy rate will take not one but a few steps, we expect the key rate to be 20% at the June Monetary Policy Committee meeting. But President Erdogan’s latest statements increase the upside risks to our call.

Poland: PPI Inflation continues to fall as retail sales remain subdued

Industrial production: -2.0% year-on-year (May)

The industrial output decline continued in May, albeit at a slower annual pace than in April, but manufacturing remains under pressure as German and European industries underperform. The PMI survey points to a slight improvement in output and new orders last month. The boost from the automotive industry is waning as the backlog of works declines and previous orders are increasingly executed.

PPI inflation: 4.7% YoY (May)

The PPI index has been falling since February and we forecast that May marked a fourth consecutive month of declines. We estimate that prices declined in all sections of industry in May vs. April, with the potential exception of water supply. Declines in manufacturing prices are among others driven by cheaper coke and refined petroleum products. At the same time, we expect a further decline in energy prices and lower prices in mining and quarrying. The PPI index usually leads CPI with some delay, so a short-term downward trend in consumer inflation is expected to continue.

Wages: 13.0% YoY (May)

We forecast that wage growth continued rising robustly in May. Surveys suggest that businesses still plan wage increases and potentially even higher than in 2022. Moreover, in 2024 the minimum wage will increase by more than 20%, which makes us believe that double-digit growth of wages will be continued next year as well – especially given that the labour market remains tight. The LFS unemployment in Poland is the lowest in the EU and employment increased sizably in the first quarter of this year.

Employment growth: 0.5% YoY (May)

Enterprise sector employment seems to have been in a soft patch and the low annual growth of employment is mainly linked to supply-side constraints. Structural factors (a decline in the working-age population) continue to weigh on employment prospects over the medium term. At the same time, employment remains resilient to short-term headwinds.

Retail sales: -5.7% YoY (May)

Retail sales remained subdued in May, but the scale of annual decline should be somewhat lower than seen in the previous two months. Wages continue to expand at double-digit levels, so observed disinflation should gradually lead to the recovery in real disposable incomes of households and allow a rebound in purchases later this year. Still, consumption is expected to remain negative in year-on-year terms in the second quarter for the third quarter in a row.

Czech Republic: No hikes, no cuts

The Czech National Bank will meet on Wednesday and we expect rates to remain unchanged. The reasons for hiking rates mentioned by the board have disappeared in recent weeks and the main focus will be on the vote split. In May, three of the seven members voted for a hike. We expect some votes for a hike to remain for hawkish central bank communication. We expect a 5:2 vote split in the baseline scenario, however central bankers voting for a hike in May have not been very vocal of late and so it is hard to assess how they see weaker inflation or wage growth.

Overall, the vote split will thus be the main question for Wednesday's meeting, which will determine the outcome. However, the governor will still be pushing a hawkish message of higher rates for longer, and premature pricing of rate cuts by the market. We see the first rate cut at the end of the year.

Key events in EMEA this week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

16 June 2023

Our view on next week’s key events This bundle contains 3 Articles