Key events in EMEA next week

It's a big week for EMEA activity data, find out what our economists will be looking out for

The CIS Space: improving economic activity in Russia

In the CIS space, Kazakhstan's preliminary GDP growth estimate for 2017 may reveal around 4% growth.

Russia will have its key macro data for January, which may reveal a pick-up in real wages growth due to public wage indexation, but on the back of some base-effect related weakness in retail sales. Still, we expect to see improving momentum in economic activity in coming months.

Poland: monthly data to support strong growth

We expect monthly data for January to present a rosy picture of the economy with industrial production accelerating to 8% year-on-year and even stronger retail sales (9.2% year-on-year above market consensus at 7.3% year-on-year). Such figures should support strong GDP growth exceeding 5% year on year in 1Q18.

Croatia: a rating upgrade from Moody's?

We expect Moody’s to follow the other two major rating agencies and improve at least the rating outlook for Croatia from stable to positive with reasonable chances for a rating upgrade on improving debt metrics.

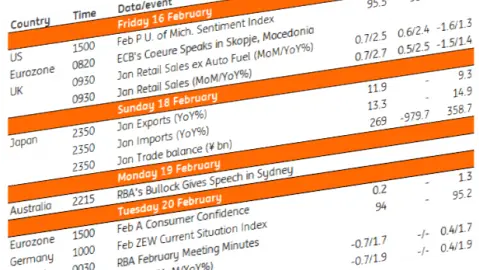

EMEA Economic Calendar

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

15 February 2018

Our view on next week’s key events This bundle contains 3 Articles