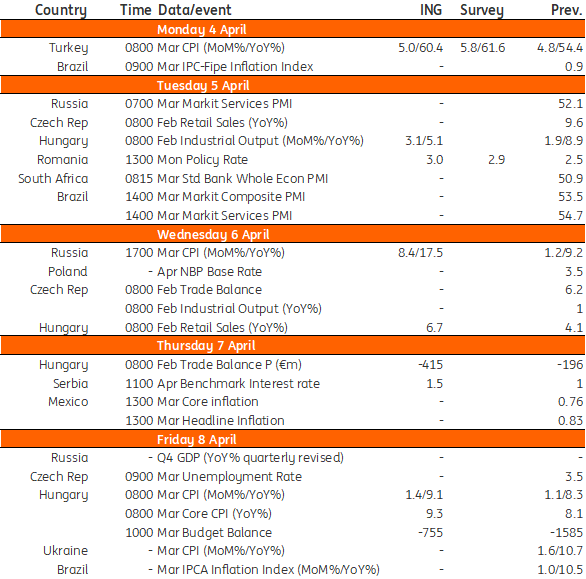

Key events in EMEA next week

The Hungarian economy will show strong industrial output and retail sales figures, but high inflation remains the primary concern across emerging markets

Hungary: Solid growth in industry but inflation persists

Next week is going to bring us a very busy economic calendar in Hungary. Regarding economic activity, we see the February industry and retail sales performances to be strong based on big data and government transfers. Despite the sound growth in industry, trade balance deterioration will continue on the worsening terms of trade due to rising prices in the commodity complex. However, these data are referring to the past and hardly reflect the full economic impact of the Ukraine war. What will however reflect that is the March inflation print. We see headline inflation rising further both on a monthly and yearly basis. Despite anti-inflationary measures, the year-on-year headline figure could move above 9%, alongside core inflation. In our view, the core reading could surpass the headline reading for the first time since early 2021.

Turkey: Continued upside price pressures

Despite there being some impact from VAT cuts on food products introduced in mid-February, annual inflation will maintain its uptrend to 60.4% (5.0% on a monthly basis) in March from 54.4% a month ago, given significant upside pressures on commodity prices – particularly in energy and agricultural commodities, in addition to the impact of FX pass-through, deteriorating expectations, and pricing behaviour.

EMEA Economic Calendar

Download

Download article

1 April 2022

Our view on next week’s key events This bundle contains 2 ArticlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more