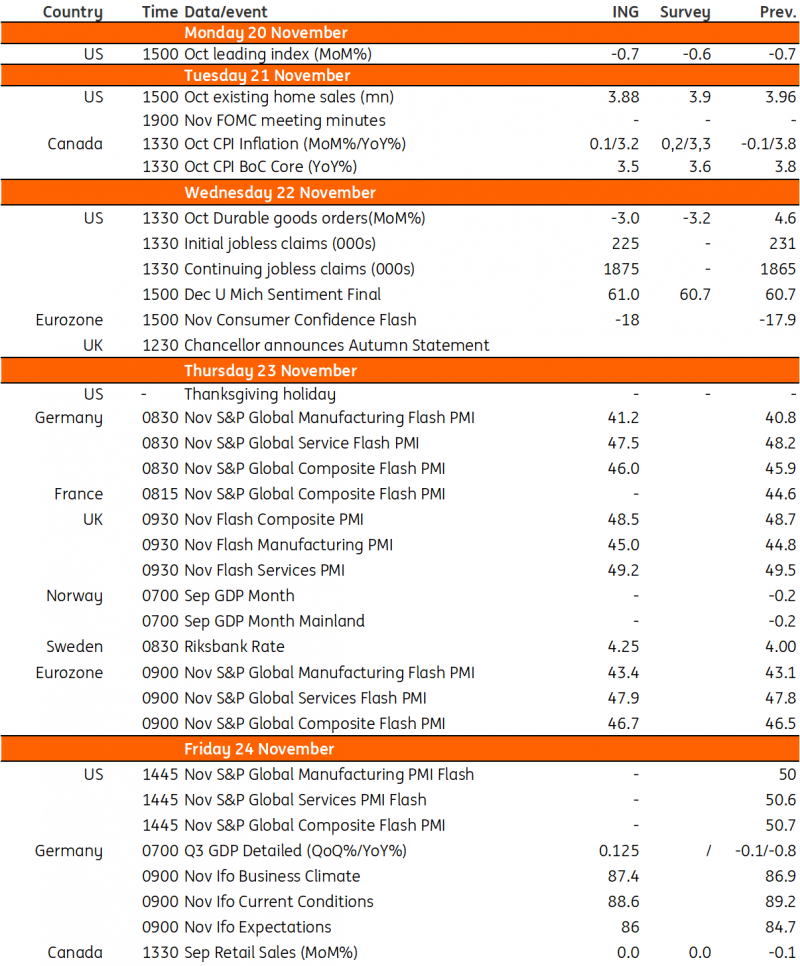

Key events in developed markets next week

All eyes will be on the 1 November FOMC minutes next week, although they're unlikely to be especially market-moving. In the eurozone, we don't expect any pickup in PMI data, while over in the UK, there'll be limited room for tax cuts as the Autumn Budget is unveiled. In Sweden, a weaker SEK could tip the balance in favour of a Riksbank rate hike

US: We expect home sales to drop to new cycle lows

Next week is a holiday-shortened week in the US, which should bring some calm to the market after recent big swings. Slowing inflation and softening labour data have reinforced the view that the Federal Reserve has finished hiking interest rates, with momentum now building behind the view that the central bank will be in a position to aggressively cut rates next year. There are now nearly 100bp of cuts priced, with May seen as the potential starting point. We continue to see the risk of a more intense slowing in economic activity, which could mean the Fed ends up cutting interest rates more aggressively than the market is currently pricing.

In terms of data for next week, we will be closely following housing, durable goods orders and jobless claims numbers. Home builder sentiment is plunging in the wake of mortgage rates increasing to 8%, leading to even weaker mortgage application numbers. Consequently, we expect existing home sales to drop to new cycle lows. Meanwhile, durable goods orders will fall sharply due to Boeing order book-induced volatility, so we will be putting more emphasis on the core measure (which excludes defence and aircraft orders) and that should continue ticking higher. Jobless claims numbers will probably be the biggest market mover. Initial claims are still pretty low, indicating that firms are reluctant to fire workers, but continuing claims are climbing, which suggests a growing reluctance to hire – effectively signalling that the labour market is cooling, but isn’t collapsing. Another big rise in jobless claims could prompt the market to more aggressively anticipate rate cuts next year.

We will also see the minutes of the 1 November FOMC meeting, but this is likely to be less market-moving than usual, given the post-meeting softness in data. We have already heard from several Fed officials who have welcomed the direction of the numbers but commented that they want to see more of the same to be sure that inflation is on the path to 2%.

Eurozone: We don't expect a meaningful pickup for PMI's in November

Next week will be all about confidence data for the eurozone. Consumers have become more downbeat again recently, despite fading inflation and decent nominal wage growth. A consumption-led rebound is expected for 2024, but current data doesn't suggest that this will happen at the start of the year. Think more towards the second half of 2024, when real wage growth should be somewhat stronger still. The PMIs have been pretty weak, too. We don't expect any meaningful pickup for November as the economy suffers from weak consumption, slowing investment and sluggish external demand at the moment. A modest negative GDP growth rate for the fourth quarter is our base case for the time being.

UK: Limited room for tax cuts as UK Chancellor unveils Autumn Statement

UK Chancellor Jeremy Hunt is likely to be gifted with a rare bit of good news as he gears up for his Autumn Statement on 22 November. Not only has borrowing come in £20 billion lower than forecast so far this fiscal year, but new projections from the Office for Budget Responsibility (OBR) are likely to show that he has a little more wriggle room to play with whilst still meeting his main fiscal goal of lowering debt as a share of GDP within five years. Higher interest rates push up debt interest, but that'll be more than offset by higher revenues linked to higher inflation. Our rough estimates suggest the Chancellor will be landed with roughly £15 billion in “headroom” against his fiscal targets, an increase from the £6.5 billion available back in March. Still, that's not much by historical standards and means the Chancellor has little room to play with. Don't expect any major changes this week.

Sweden: Weaker SEK next week could tip the balance in favour of a Riksbank rate hike

Next week’s Riksbank decision looks like a 50/50 call. The central bank told us back in September that it was considering another rate hike this month, but in many respects, the case for further tightening has diminished. The jobs market – often cited by policymakers as a clear area of resilience – does appear to be cooling. Vacancy levels are falling quickly now, unemployment appears to have bottomed, and surveys show that a lack of labour is much less of a constraint for businesses than it was a few months ago. Services inflation is still too high, though pricing intentions are clearly falling in these industries. The latest core CPIF reading was more-or-less in line with the Riksbank’s forecast. And finally, the housing market remains vulnerable despite a tentative stabilisation earlier this year.

Then again, the Riksbank is visibly worried about currency weakness. The krona was mentioned 50 times in the most recent meeting minutes, and next week’s decision will in no small part depend on how SEK trades between now and then. On a trade-weighted basis, the currency is actually a little stronger than what had been assumed in September’s projections, though this is a little artificial given the Riksbank’s FX selling.

Over the next week, our FX team expects a pullback in risk-sensitive currencies like SEK, along with a USD rebound in the coming days. If that happens, it may well tilt the balance towards a hike, and we’ve pencilled in a rate rise for that reason alone. The lack of another scheduled meeting until February is also a consideration. There’s a decent chance of a pause however, not least because the Riksbank is increasingly a hawkish outlier in the developed market central bank space.

Key events in developed markets next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

17 November 2023

Our view on next week’s key events This bundle contains 3 Articles