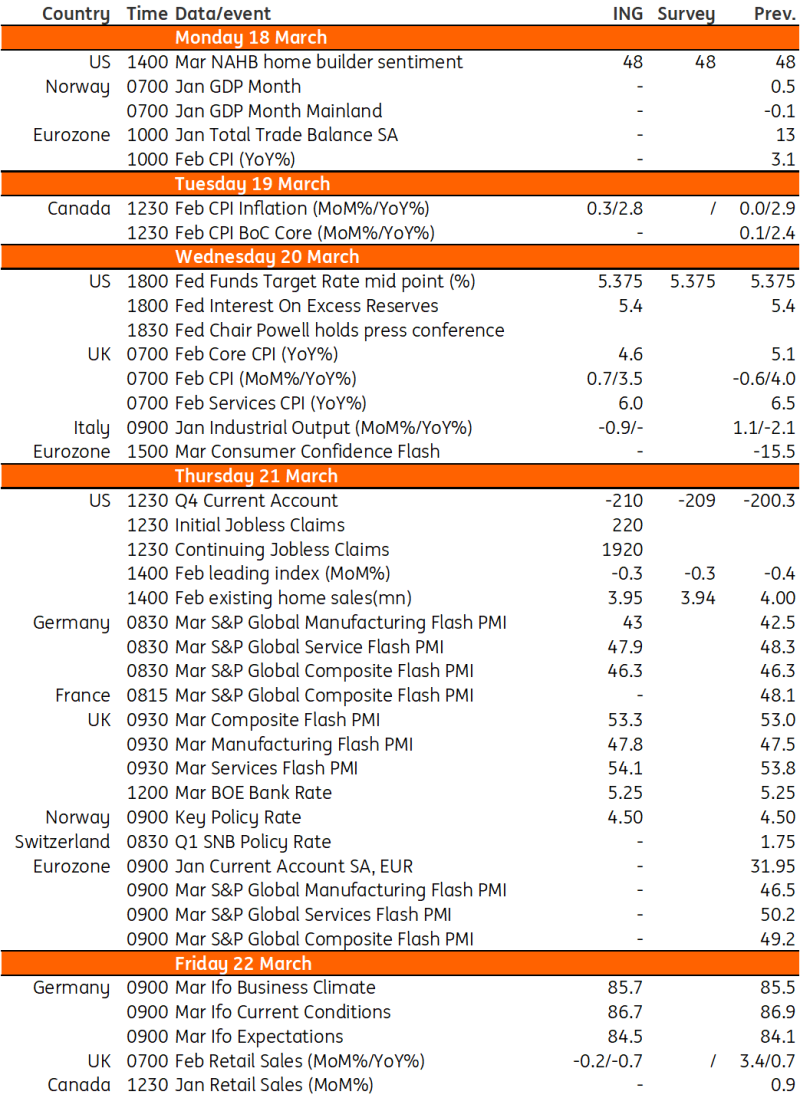

Key events in developed markets next week

The Federal Reserve's policy meeting takes centre stage next week. We see the next move as a cut in June following a series of hot data releases. In the UK, all eyes will be on the release of inflation data, before the Bank of England meeting on Thursday. In our view, the first rate cut will come in August

US: We think the next move is a cut in June

Next week’s highlight will be the Federal Reserve’s FOMC meeting. US growth, jobs and inflation data remain too hot for the Federal Reserve to contemplate imminent interest rate cuts. There are some people that think the Fed may need to hike rates further, but we don’t see this happening. We (like the market) think the next move is a cut, most likely in June. After all, Fed Chair Jerome Powell recently suggested that officials are “not far” from having the confidence to “dial back” on the restrictiveness of monetary policy.

Attention will focus on the projections of FOMC members. At the December forecast update, the Fed signalled they felt three 25bp rate cuts would be the most likely path forward for 2024 with a further 100bp of cuts pencilled in for 2025. We expect a similar set of projections at the 20 March FOMC meeting with the messaging indicating that the Fed is inclined to cut rates later this year, but they need to see more evidence to justify that action. That said, given the dispersion of predictions by individual Fed members it would only take two of six FOMC members switching from a current 4.625% projection either higher or lower to move the median dot away from three rate cuts to signalling two or four rate cuts in 2024. We suspect a shift to two rate cuts from three is a higher risk than the Fed moving to signal four.

The Fed doesn’t want to cause a recession if it can avoid it and we believe they will be in a position to start moving monetary policy from a restrictive position to a more neutral stance before the summer. They are currently suggesting the neutral Fed funds rate is around 2.5% so there is room for up to 300bp of cuts just to move to “neutral”. We think they won’t want to go quite that far given the prospect of ongoing loose fiscal policy irrespective of who wins the November presidential election, but we expect 125bp of cuts this year, starting in June, with a further 100bp in 2025 as hopes rise for a soft landing for the economy.

In terms of data, we will be mainly digesting housing numbers. Affordability is woeful given high prices and high borrowing costs and we expect to see transactions remaining at very low levels.

UK: Bank of England to stay the course and await more data

It’s a busy week in the UK, and it kicks off with February inflation data due just a day before the Bank of England’s decision on Thursday. Remember that services inflation is absolutely key to the timing of the first rate cut, and we’re likely to see a jump downward as price pressures continue to gradually ease. It’s worth saying that our forecast for 6% services CPI is pretty much in line with the most recent BoE projections, so it would take a meaningful downside surprise to raise many eyebrows on the committee ahead of the March decision. As for the meeting itself, we expect the Bank to reiterate its previous forward guidance that rates need to stay sufficiently restrictive for an extended period. Watering down that language would be seen as tantamount to opening the door to an imminent rate cut, something we doubt the committee wants to do. The more interesting question is whether the two hawks who voted for a rate hike in February finally throw in the towel, though we wouldn’t be surprised if at least one of them doesn’t. At the same time, we don’t expect lone dove Swati Dhingra to be joined by other members in voting for a rate cut this month. Our view is that the first rate cut will come in August, once the inflation data for the second quarter has come through.

Key events in developed markets next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

15 March 2024

Our view on next week’s key events This bundle contains 3 Articles