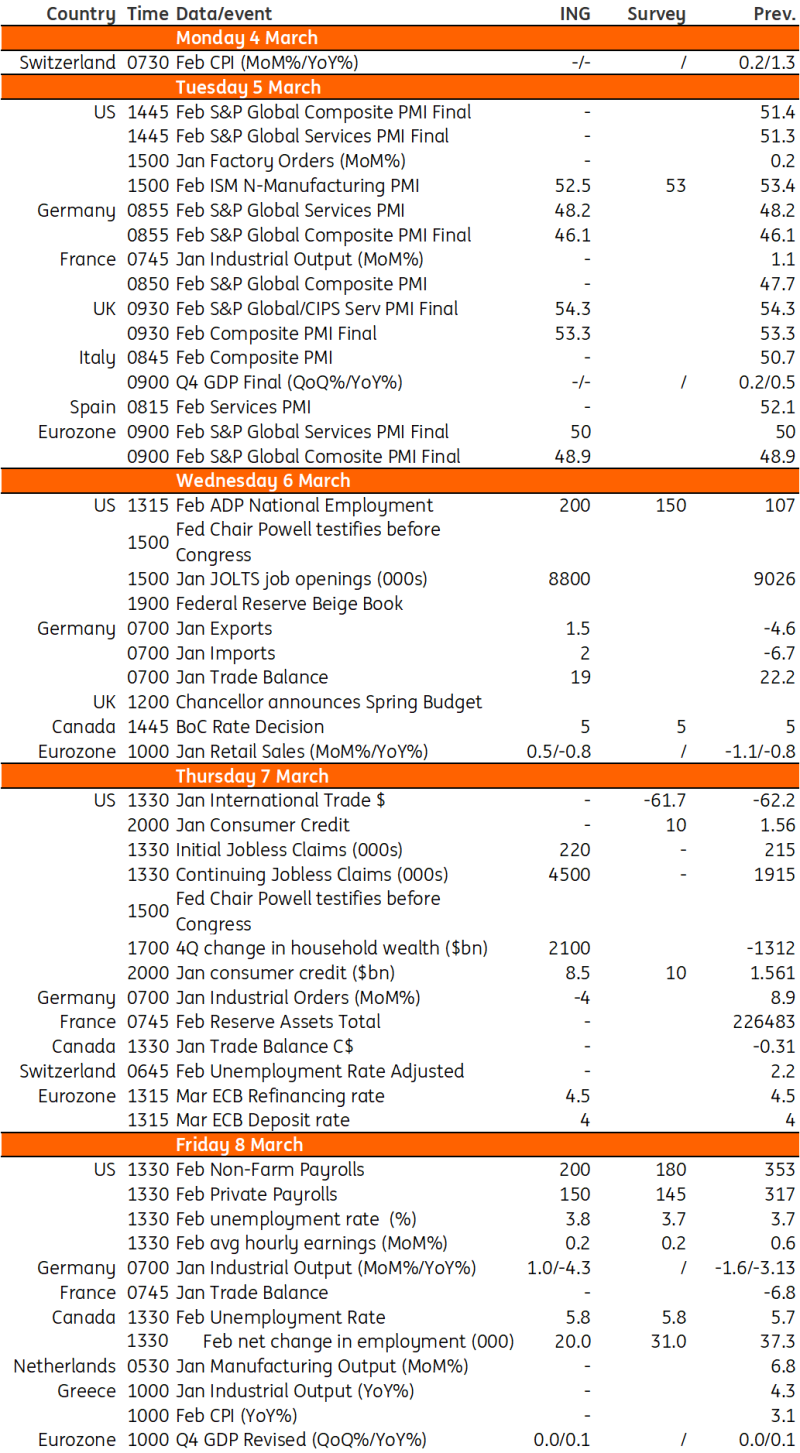

Key events in developed markets next week

An important week in the US will see Fed Chair Jerome Powell testifying before Congress, as well as the release of February's jobs report following a blowout in January. In the eurozone, we expect a small uptick in February retail sales, while the scope for UK tax cuts looks limited ahead of the Spring Budget. The Bank of Canada is expected to hold rates at 5%

US: Fed Chair Jerome Powell testifying before Congress

It's a big week for markets, with Federal Reserve Chair Jerome Powell testifying before Congress on the state of the economy and the situation regarding monetary policy. As with his recent commentary, he will likely indicate a willingness to eventually start moving monetary policy away from restrictive territory towards a more neutral footing, but officials need to see data to justify such action. With GDP growth coming in hot, the jobs market remaining tight and inflation running too fast there is little prospect of an imminent interest rate cut.

In terms of economic data, the focus will be Friday’s February jobs report after January’s blow out 353,000 increase and upward revisions to November and December. We will be able to firm up our forecasts as we go through the week and see what the ISM and NFIB business organisations say about what their members are experiencing, but for now we are provisionally penciling in something around the 200k mark. This is despite anecdotal evidence of rising job lay-offs at major employers, which we think will dampen the data in coming months. Average hourly earnings will correct lower after a big jump related to fewer hours worked for salaried professionals in January – relating to bad weather limiting some employees’ ability to get into work. We also expect the unemployment rate to rise a tenth of a percentage point to 3.8%.

Eurozone: Small uptick in February retail sales expected

Not many interesting eurozone deta points will be out next week to accompany the European Central Bank meeting, but retail sales data for January on Wednesday will give a sense of how the economy started the year. A big December decline in sales showed that Europeans were thrifty for the holiday season this year, but this fits a broader trend of weak spending on goods since late 2021. We expect a small uptick in January but nothing that can be seen as the start of a recovery.

UK: Scope for UK tax cuts looks limited ahead of Spring Budget

UK Chancellor Jeremy Hunt has made it abundantly clear that he intends to cut taxes in the Spring Budget on 6 March. But with markets more cautious about the extent of Bank of England rate cuts, the chancellor will have less money to play with than he’d hoped just a few weeks ago. We think Hunt's “headroom” will still have increased from £13bn to £18bn, on account of slightly lower market rates compared to at the time of November’s Autumn Statement. That headroom is money that could in theory be given away, while still meeting the main fiscal rule of debt falling as a share of GDP in five years’ time.

The situation is tight. Reports suggest the chancellor will scale back his planned pre-election tax cuts and the package of support will be less substantial than back in November. The alternative is to bake in even tighter spending plans for future years to try and eek out further room for tax cuts, but this looks highly challenging.

Canada: Policy rate to remain at 5%

We expect the Bank of Canada to leave the policy rate at 5% at the upcoming meeting on 6 January The BoC is sounding a little less hawkish, but with officials not expecting inflation to return to the 2% target until next year, it's unlikely to signal that it is relaxed enough to ease monetary policy soon.. As with the Fed, we are looking at June as the likely starting point for interest rate cuts.

Key events in developed markets

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

1 March 2024

Our view on next week’s key events This bundle contains 3 Articles