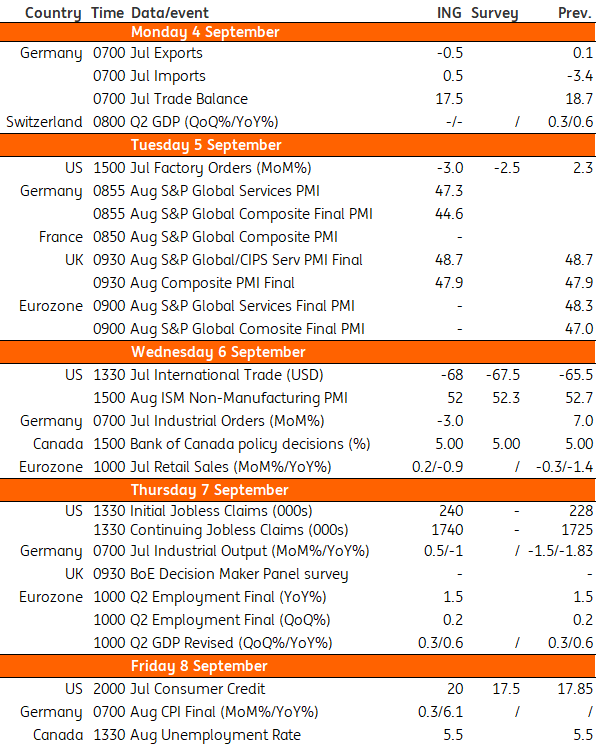

Key events in developed markets next week

Watch out for further weakness in the US service sector as rate hikes continue to feed through into the economy. The Bank of Canada is set for a pause as growth data cools

US service sector set to lose momentum as lending standards tighten

After a couple of months of US data consistently providing positive surprises, we have seen a series of misses more recently, which have helped cement expectations for an 'on hold' interest rate decision at the 20 September Federal Reserve FOMC meeting. Markets have also switched back to pricing just a 50-50 chance of any further rate hikes given growing evidence that inflation pressures are waning and that the 2% target will be in reach by early next year.

The upcoming data flow is unlikely to meaningfully alter this situation with the ISM services index on Wednesday the likely highlight. We, like the market, expect it to soften marginally and that suggests that the sector is losing a little momentum as we head towards the fourth quarter. Factory orders are likely to fall given the big drop in Boeing aircraft orders already announced, while consumer credit for July should rebound sharply given the strong retail sales and consumer spending numbers already published.

However, with banks increasingly tightening lending standards, especially for consumer credit, we expect to see less pronounced increases in the coming months with declines looking more likely for early 2024 as financial stresses mount.

Bank of Canada to keep rates on hold as growth cools

The Bank of Canada (BoC) is widely expected to leave the policy interest rate at 5% on 6 September. With growth cooling in the second quarter and the unemployment rate ticking higher, we suspect that the BoC will feel it has done enough, after implementing 425bp of interest rate increases, to bring inflation back to target in the medium term even though CPI did pick up a touch last month.

According to the latest Bloomberg survey, just three of 32 analysts questioned felt the bank would raise rates by 25bp with everyone else looking for no change. Overnight index swaps are pricing only around a 15% chance of a hike.

Bank of England survey to signal that price pressures are cooling

Bank of England Chief Economist Huw Pill reinforced the message this week that we're near the end of the tightening cycle, and that how long rates stay high is now more important than how high they ultimately settle. We wouldn't take that to mean the Bank will pause at the September meeting, and we continue to expect another 25bp hike with both services inflation and wage growth having recently come in higher than expected. But November remains more of a question mark, and mounting signs of economic weakness suggest a pause is still more likely than not at this stage.

Next week, we'll get the latest Decision Maker Panel survey from the BoE, and this asks chief financial officers a range of questions about their expectations, notably on inflation. Admittedly the BoE seems to be putting less emphasis on survey data at the moment while the actual inflation data continues to come in hot. But this survey suggests that price and wage pressures are cooling, and hiring difficulties are easing.

Key events next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

1 September 2023

Our view on next week’s key events This bundle contains 3 Articles