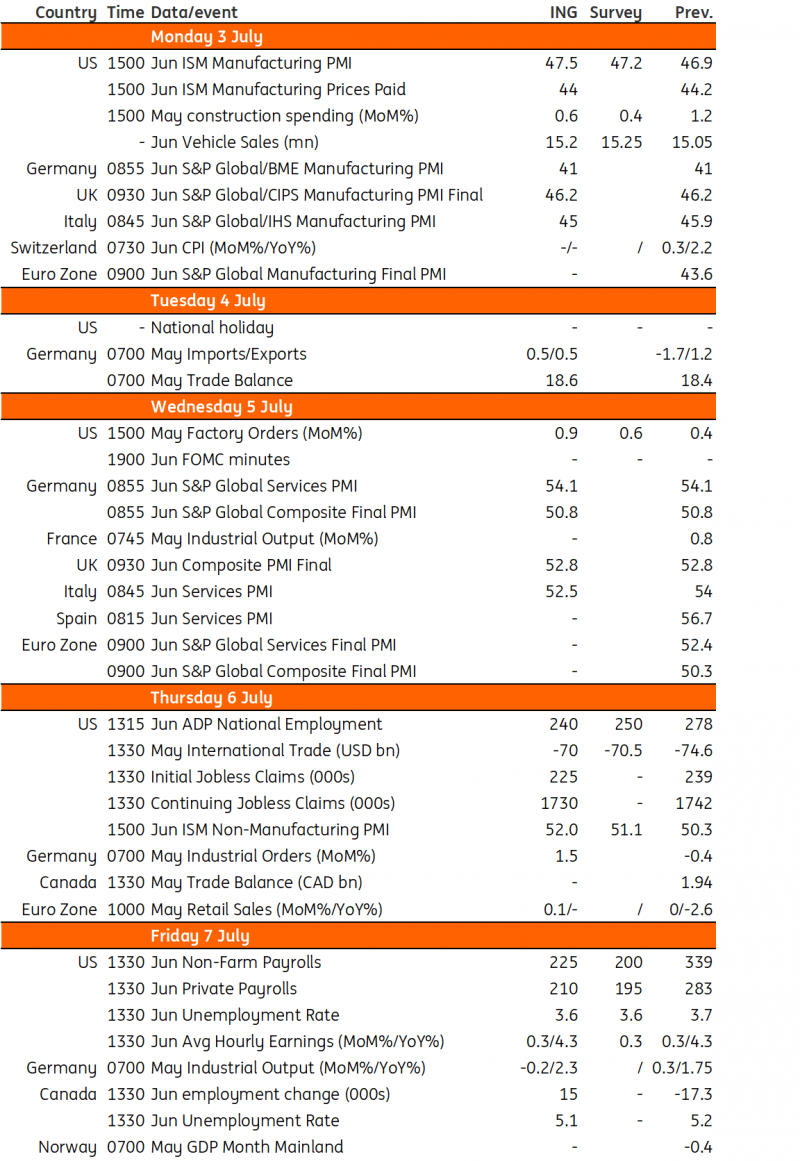

Key events in developed markets and EMEA next week

Keep an eye out for key data releases in the US next week, including the jobs report and the ISM manufacturing and service sector reports. In Poland, a continued decline in CPI could signal rate cuts sooner than expected

US: July rate hike looks like a done deal

Last week, Fed Chair Jerome Powell again reiterated the Federal Reserve base case of two further rate hikes in 2023. Markets had been sceptical, but a strong run of activity data has shifted attitudes, with a 25bp hike fully priced by September and a further 10bp or so priced by the November FOMC meeting. We had been thinking the Fed funds rate had hit a peak in May, but the central bank's robust position on the need for further tightening, sticky inflation and a tight jobs market means we have to accept that a July rate hike looks a done deal. It would take a very soft June jobs report, surprise softness in the June core CPI print and/or a financial system issue to deter the Fed from hiking.

This week’s data calendar includes the jobs report plus the ISM manufacturing and service sector reports. The ISM surveys suggest the economy is struggling, something not borne out in the official activity data. The manufacturing ISM has been in contraction (sub-50 territory) for seven months in a row and this week’s report looks set to make it eight consecutive months of contraction. The service sector ISM is still above 50, but barely. We look for a fourth consecutive month where the headline index is hovering in the 50-52 range. We will also be closely following the employment sub-indices, along with the job opening data and the ADP private payrolls series as we look to firm up our forecasts for Friday’s non-farm payrolls print.

Last month, the rise in non-farm payrolls was immensely strong at 339,000, but we do expect to see a moderation this month with something closer to the 225,000 mark. The unemployment rate jumped to 3.7% from 3.4% last month given the household survey data painted a very different picture to the payrolls data – with households reporting that employment actually fell. We see this reversing part of the jump and coming in at 3.6%. Meanwhile, average hourly earnings should soften a touch with another 0.3% month-on-month print, which would bring the annual rate of wage growth down to 4.2%.

Canada: Sticky inflation could see another rate hike in July

In Canada, the market is split as to whether the Bank of Canada will hike rates again in July after raising rates 25bp in June. Prior to that, interest rates had been on hold since the January meeting. Decent growth, a tight jobs market (set to be confirmed by next week’s data) and sticky inflation mean that we favour another BoC hike on July 12.

Poland: No policy change expected from Narodowy Bank Polski

We expect no policy changes from the National Bank of Poland (NBP) in July. However, we estimate that the chances of a rate cut after the vacation have increased to 65-70% where we previously saw 50%, given guidance provided by some MPC members, including President Adam Glapiński. We also see the possibility that the NBP will make more than one cut in 2023. Our short-term inflation forecasts are optimistic, with CPI falling to single digits in September or August – which should further strengthen the MPC’s dovish stance.

Our longer-term forecasts are pessimistic (stabilisation of core at 5% year-on-year in 2024-25). Polish inflation problems are closer to those of developed countries given strong labour markets plus an election cycle. However, the NBP should find support from emerging market central banks, which started hikes earlier than developed markets and now may be further ahead on their easing path. The market perception of rate cuts in Poland should be still positive – at least as long as headline CPI continues decreasing – despite the Fed, European Central Bank, and Bank of England continuing to hike and maintaining a hawkish stance.

Hungary: Disinflation to continue on food, durables and energy prices

The first week of July will be a busy one when it comes to the Hungarian data calendar, and our main focus will be on the May economic activity data. Dropping fuel prices in May might help retail sales a bit, though we still see a double-digit year-on-year contraction in volumes. When it comes to industry, after a bleak April a mild rebound is expected on a monthly basis, but when it comes to the yearly figure (due to the lower number of working days) we see the raw index moving further south.

The latest budgetary data will make Thursday exceptionally busy. We expect the budget to post a moderate deficit in June, with the main driver being the revenue side’s weakness in reducing domestic demand. Last but not least, Friday will bring us the June inflation prints. We expect the speedy disinflation to continue on food, durables and energy price, although services will counterbalance the impact in our view. With favourable base effects, we see the headline drop a touch below 20% YoY, while core inflation moves close to 21% YoY. We see risks tilted to the downside.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

30 June 2023

Our view on next week’s key events This bundle contains 2 Articles