Japan: A modest recovery will continue to be supported by accommodative macro policies

We expect Japan's GDP growth to slow in 2023 but to remain above its potential rate, supported by an accommodative macro policy environment. The near-term outlook is bleak due to high inflation and weak global demand conditions

Japan: At a glance

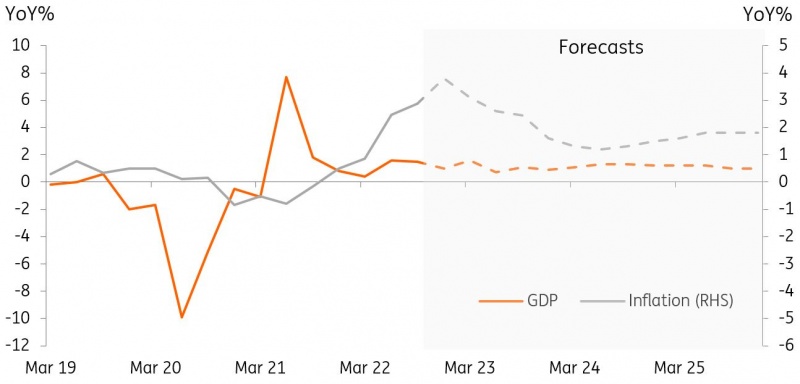

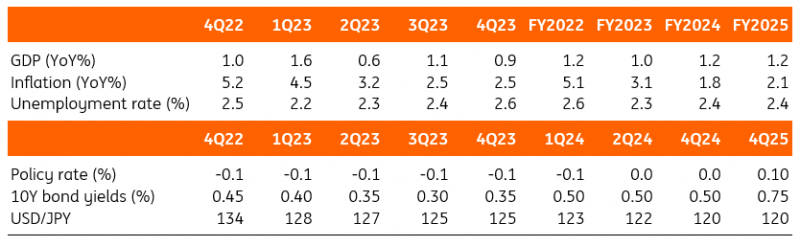

After a slight contraction (-0.2% quarter-on-quarter seasonally adjusted) in the third quarter of 2022, we expect GDP to rebound (0.6%) in the fourth quarter. A stronger yen and more relaxed border controls are likely to improve trade conditions, plus the fiscal stimulus programme will support a fourth-quarter recovery. However, the rebound should be limited as cost-push inflation puts pressure on corporate margins and household spending. We expect GDP to grow by 1.0% year-on-year in 2023, slightly lower than the 1.2% growth we expect for 2022. Weakening demand from the US, EU, and China will hurt exports and manufacturing, while limited wage growth will slow private consumption in the first quarter. Inflation hasn't peaked yet in Japan and is likely to hit 4.0% in early 2023, but it will soon decelerate back to the 2% range in the second quarter. Fiscal policy will continue to support the recovery while monetary policy will reduce the extent of accommodation, but at a slower pace than the market currently expects.

GDP and inflation outlooks

3 calls for 2023

Normalisation of Bank of Japan policy – a long and tough road ahead

The Bank of Japan's (BoJ's) unexpected decision to broaden its yield curve control band in December has paved the way for policy normalisation. But the path forward will face many challenges. A cloudy growth outlook early in the year could prevent the new central bank governor from taking immediate action, while cost-push inflation is likely to begin to subside in the second quarter. In our view, wage growth will rise more slowly than the 3% sought by the BoJ. Considering these factors, we believe the new governor will first adjust the BoJ's forward guidance in the second quarter and then call for a policy review in the third quarter. We also believe that revisiting inflation targets could be a consideration. Eventually, we expect the BoJ to lift the mid-point target for the 10Y Japanese government bond (JGB) from 0% to 0.25% in early 2024. If GDP recovers to pre-pandemic levels sooner than we expect, the timing could be moved up to the end of 2023. We also expect the BoJ to raise its short-term policy interest rate from -0.1% to 0.0% in the second quarter of 2024. That supports our view that the JGB yield curve will flatten by about 15 basis points and thus the 10Y JGB yield will come down to the 0.30-0.35% range by the year-end.

Wage growth is key to watch

We expect the job market to tighten in the short term as hospitality and tourism-related employment continues to rise, benefiting from the government's travel subsidy programme and the return of inbound travel. However, manufacturing jobs will likely decrease, mainly due to sluggish exports. Although the government offered incentives for wage increases this year, we anticipate that actual wage growth will be less than 3%. Base salaries may pick up, reflecting high inflation, but most of it is expected to be offset by a reduction in bonuses and other incentives as corporate earnings are likely to be squeezed. It is also questionable whether wage growth of 3% can be sustained in the upcoming years.

Fiscal policy is supporting growth

The second FY22 supplementary budget of 29 trillion yen (5.5% of GDP) will boost near-term growth, providing energy subsidies, maternity and childcare-related support, and vocational training support. In addition, the Cabinet approved a draft budget of 114.4 trillion yen for FY23, which is a 6.3% year-on-year rise from FY22's original budget. However, most of the positive impact of fiscal policy will be concentrated at the end of 2022 and early 2023. The budget rise in FY23 is mainly due to a large increase in defence spending (26.3% YoY), thus its policy impact on the real economy should be limited. In addition, if the government raises taxes and cuts other programmes to finance defence spending, it could hurt private consumption and result in a sudden drop in approval ratings.

Japan forecast summary table

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

9 January 2023

Asia Outlook 2023: Darkest before the dawn This bundle contains 11 Articles