CEE Issuance Outlook 2026: Diversify, pre-fund, switch, repeat

- 26 February

- FX

Sovereign issuance in 2026 is set to be driven mainly by refinancing needs and debt costs rather than fresh fiscal loosening. Governments will increasingly rely on diversified funding – retail bonds, T‑bills, EU and FX sources – to contain net local bond supply and manage curves, with Turkey the clear outlier as net issuance rises sharply

Local currency issuance: Refinancing-driven supply and disciplined debt management

Despite a strong rebound in global EM debt inflows, CEE local bond markets remain largely on the sidelines, with foreign demand highly selective and concentrated in countries offering a strong idiosyncratic story. Across most of the region, foreign bondholder shares have stabilised or edged lower, implying stagnation in relative terms. As a result, local banks, flush with liquidity, continue to dominate demand, shaping bond market technicals.

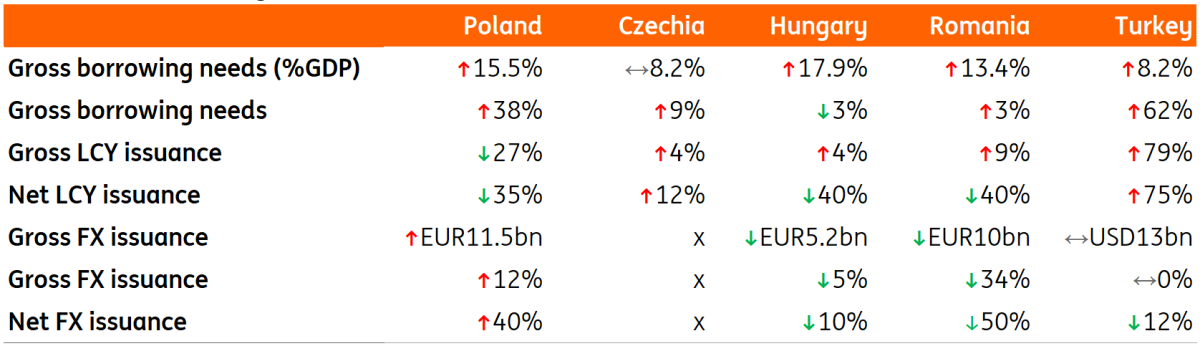

Across the CEE region, sovereign issuance dynamics are increasingly shaped by refinancing needs rather than fresh fiscal expansion. While headline borrowing requirements are rising in most countries, the primary driver is the rollover of large maturity profiles and higher debt service costs, not a new wave of discretionary deficit spending. In this sense, CEE supply in 2026 is first and foremost a redemption story, with fiscal deficits playing a secondary role.

This pattern is visible across the region. Poland faces record-high redemptions and off-budget items, Hungary enters a year of historically large bond maturities, and Turkey’s gross needs are dominated by redemptions and inflation‑driven debt costs. Romania similarly confronts elevated domestic and external maturities. Even in the Czech Republic, where proactive pre‑financing has lowered near‑term needs, the core discussion still revolves around managing the redemption profile rather than funding new deficits.

CEE issuance summary

At the same time, funding diversification has become the default strategy for sovereign debt managers. Governments are increasingly relying on non‑benchmark instruments to reduce pressure on local yield curves. Retail bonds play a growing role in Poland and Romania, T‑bill issuance has been revived or expanded in Poland and the Czech Republic, and EU funds, including Recovery and Resilience Facility (RRF) inflows, remain a critical pillar in the overall funding mix. FX issuance is also set to remain an important component for several issuers, reinforcing a shift toward more instruments and less reliance on duration supply.

From a market perspective, net supply matters more than gross figures, and here the picture is more benign. Despite higher gross issuance, net bond supply is falling sharply in Poland, Hungary and Romania, cushioning local markets. The Czech Republic should see only a moderate increase in net issuance, while Turkey stands out as the main exception with a significant rise in net supply, mainly due to high inflation.

Political constraints remain a key backdrop. Election cycles and coalition dynamics cap the scope for aggressive fiscal consolidation, even where consolidation is formally targeted. As a result, issuance policy has become more technocratic and flexible, compensating for politically constrained fiscal policy.

Finally, debt management is increasingly active. Sovereign issuers are emphasising belly‑curve issuance, anchoring the long end, and expanding the use of switches, taps and pre‑funding. Overall, CEE supply is being carefully managed, with liability management playing a central role in navigating a challenging macro‑fiscal environment.

FX issuance: Slight slowdown expected for CEE

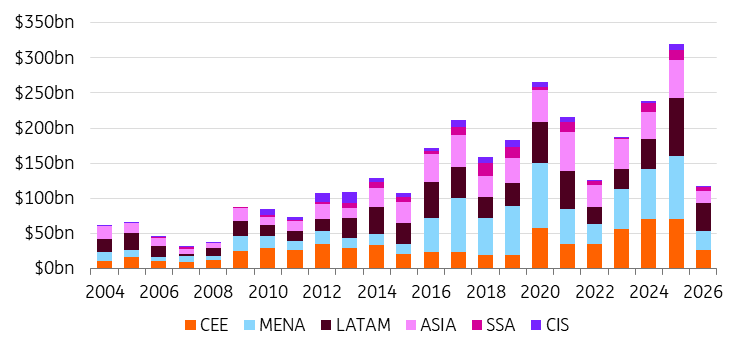

2025 saw another solid year of sovereign Eurobond issuance for CEE, with over $70bn issued in USD and EUR in total, of which almost $37bn was from Romania, Poland, and Hungary. This was down slightly on 2024 in gross terms but represented an increase in net supply given lower maturities in 2025 for Romania in particular.

In an EM context, CEE also constituted a significantly lower percentage of total issuance (22% in 2025 vs 30% in 2024 and 2023) given the acceleration in the pace of issuance from MENA and Latam that drove a record year for EM sovereigns and quasi-sovereigns in 2025. MENA saw $89bn of USD and EUR issuance in 2025, while Latam saw $81bn.

EM USD & EUR sovereign and quasi-sovereign international bond issuance

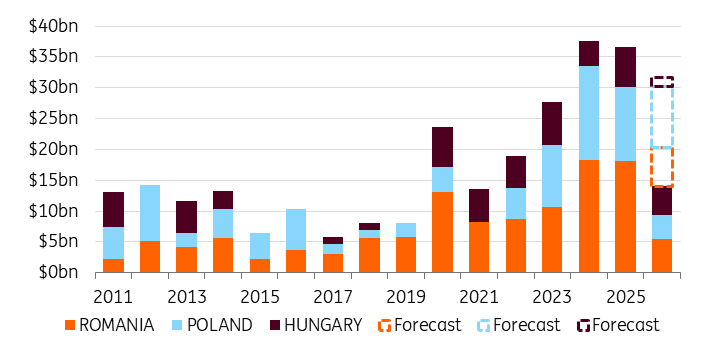

We expect the pace of issuance from CEE to slow modestly in 2026, with Romania standing out as the key driver. With limited signs of fiscal consolidation across much of the region, including in Hungary and Poland, Romania should prove something of an outlier within the CEE region in terms of fiscal improvement, despite coming from the worst position in the region.

A combination of fiscal tightening and large expected EU fund inflows make the government’s plans for lower gross and net Eurobond issuance (€10bn and €6.75bn respectively) much more credible than in previous years. Elsewhere, issuance from the rest of CEE should remain fairly stable despite a slow start to the year, while the focus for most should remain on a wide range of funding sources (EU money, green bonds, and alternative currencies, along with sukuk issuance for Turkey).

CEE-3: EUR & USD international sovereign bond issuance (USD equivalent)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

CEE Issuance Outlook 2026: Diversify, pre-fund, switch, repeat

- This bundle contains 8 Articles