ING’s latest economic views and forecasts

- 16 March 2020

- United States

Following some big market and central bank moves, we have updated our forecasts for growth and policy rates. Find our what our economists are looking for in the major economies over the next few months as the globe deals with the coronavirus threat

Exceptional times require exceptional measures.

It’s not only policymakers who are trying to get a grip on this fast-moving environment, so are we. Since our last regular monthly update earlier this month, the Federal Reserve has cut interest rates by 150 basis points, the European Central Bank introduced several liquidity measures and increased quantitative easing, and the Bank of England cut rates by 50bp.

At the same time, Covid-19 is quickly spreading across Europe and the US. Not only are governments taking unprecedented steps to slow down the spread of the virus, they have also started to announce fiscal support measures such as short-time work schemes, liquidity support and loans. In the US, President Trump declared a national emergency and invoked the Stafford Act, which gives access to additional funding.

Our gut feeling is that this will not be the last update

The situation in many European countries is increasingly looking like a national emergency and the number of European countries announcing lockdowns is increasing by the day. The economic impact of all these events and measures is still uncertain. A lot will depend on how long the lockdown situations last. Changing consumer behaviour, companies suffering from supply chain disruptions and the sudden drying up of demand will leave deep marks on economies. The survival of small and medium-sized enterprises and the service sector - just think of hotels, restaurants, event organisers, artists, freelancers and many others - will be at risk. While it is completely different in nature, the current crisis could have a similar economic impact as the 2008/09 crisis. It will, in any event, have a stronger impact than we had pencilled in two weeks ago.

We've therefore updated our forecasts for the major economies. Our gut feeling is that this will not be the last update.

Global picture by Carsten Brzeski

United States

- Growth: The supply crunch in manufacturing, the panic in the financial sector and the collapse in airline travel, hotel stays and leisure activities mean we could see a quarterly GDP contraction of the scale reached during the height of the financial crisis, particularly given the prospect of some city lockdowns. We are pencilling in an 8.0% annualised 2Q20 GDP decline with full-year growth down to -0.4%. That still assumes things get better over the summer.

- Inflation: The oil price plunge is already resulting in sharply lower gasoline prices and means negative headline inflation looks certain over the summer months. Expect core inflation to fall too, given weaker demand and wage growth.

- Federal Reserve: The Fed has slashed its policy rate to 0-0.25% and has announced a formal restart of quantitative easing to the tune of US$700 billion. They could easily do more QE.

- 10-year yields: We’ve lowered our quarter-end forecast to 0.5%, but a trading range of 0.2-0.5% is our favoured scenario.

United States by James Knightley

Eurozone

- Growth: With some countries going into full or partial lockdown, the hit to eurozone growth is likely to be more significant than we previously thought. With recreation, hotels & restaurants and transport taking a big hit, it will be hard to avoid a contraction in consumption in the first quarter. Durable goods sales are also likely to suffer, while investments will be put on hold. Despite the rather good Jan/Feb figures, we are now pencilling in a 6.5% annualised quarter-on-quarter contraction in the first quarter. On top of that, April is not going to see an immediate return to normal, with negative carry-over also impacting the second quarter, leading to -1.2% annualised growth. As the ECB has taken measures to avoid a credit crunch and an increasing number of governments are announcing fiscal measures to soften the blow, we think a decent upturn in the second half is still feasible. We now anticipate -1.2% GDP growth this year, although this is shrouded in uncertainty.

- Inflation: On the back of the fall in energy prices and weaker growth, inflation is revised down to 0.9% for 2020.

- ECB: In the wake of financial market turmoil and negative economic figures likely, we suspect that the ECB might ultimately be pressed to do something more, although we are very sceptical that a deposit rate cut is the right thing to do. We've pencilled in a 10bp cut, but at the same time, a big change in the tiering system for excess liquidity to mitigate the negative impact on banks. Another €100bn QE would also be part of an additional package.

- 10-year yields: Bund yields will likely continue to hover around -0.7% in the coming weeks, but could temporarily fall once the actual impact from the crisis on the economy materialises. With risk aversion softening over the course of 2Q, we should see some curve steepening.

Eurozone by Peter Vanden Houte

China

- Growth: The breakdown in global supply chains and the increasing decline in demand presents a double hit to China. Fiscal stimulus will help, which includes tax cuts to ease cash flow constraints, and new investments, so far amounting to about 6-6.5% of nominal GDP in 2020. Even so, we are downgrading first-quarter GDP growth to 3.6% from our early-March forecast of 4.4%. For 2020 as a whole, we’ve lowered growth to 4.8% from 5.2%.

- People’s Bank of China: The cut in the reserve requirement ratio (RRR), which has also been expanded to include more banks, should help small businesses. However, the degree of help really depends on how the banks assess credit risks associated with those companies, compared to the interest savings generated by participating in the inclusive finance scheme. The chance of another rate cut this month has fallen, given the targeted RRR cut should put enough downward pressure on the level of interest rates.

China by Iris Pang

United Kingdom

- Growth: A sizable hit to consumer activity - particularly concentrated in travel and hospitality (incl restaurants), and mostly hitting during the second quarter - means the UK is likely to enter a technical recession. We're expecting full-year GDP to contract by 0.6%. All of this remains pretty uncertain - the UK government's outbreak response so far signals a slightly less restrictive approach to day-to-day activity, which could prompt some near-term differences in UK growth rates relative to other European countries.

- Bank of England: Policymakers have already cut interest rates by 50bp, but more is possible. We think an additional 15bp rate cut is likely, taking rates to the lower bound. Given negative rates aren’t viewed as an attractive option by the BoE, the next step would be to increase the stock of government and corporate bond purchases. Given the swift response being taken by other central banks, this could come at (or even before) the 26 March meeting.

United Kingdom by James Smith

Asia ex-China

- Growth: The global pandemic has hit the Japanese economy at a particularly vulnerable time, following last year’s consumption tax hike. Olympics-related construction will soon end, and with the event itself under question, there could be further implications for growth. We expect Japanese GDP to contract by 1.3% in 2020. Outside China, South Korea is Asia’s worst affected economy, though the measures taken to contain the spread of the virus seem to be working. The Government has announced a further stimulus package, although we still expect just 0.6% growth in 2020.

- Central banks: The Bank of Japan has reiterated it stands ready, but there’s little it can do, other than providing liquidity as it has done over recent days. The Bank of Korea has cut the 7-day repo by 50bp, a bigger and faster move than expected, taking the rate to 0.75%. Normally one would argue that this uses up their available easing power, with rates now lower than inflation. But in these times of massive economic stress, those metrics probably no longer apply. In other parts of the region where rate constraints still exist, such as Indonesia, other measures, such as reserve rate requirements will be cut. For some in the region, namely Australia, this could end up with the adoption of some unconventional policy measures.

Asia ex-China by Robert Carnell

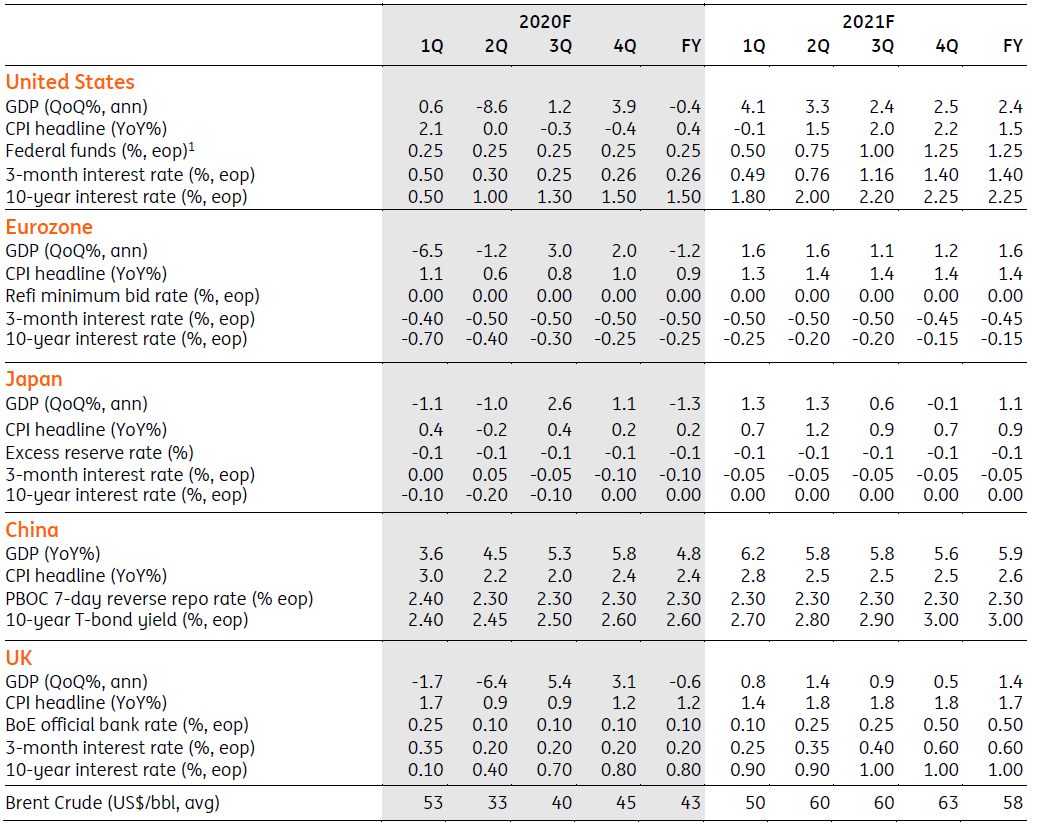

Our latest economic forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more