ING’s outlook for central banks

Our economists look at the places where monetary policy is likely to be tightened first over the next few years

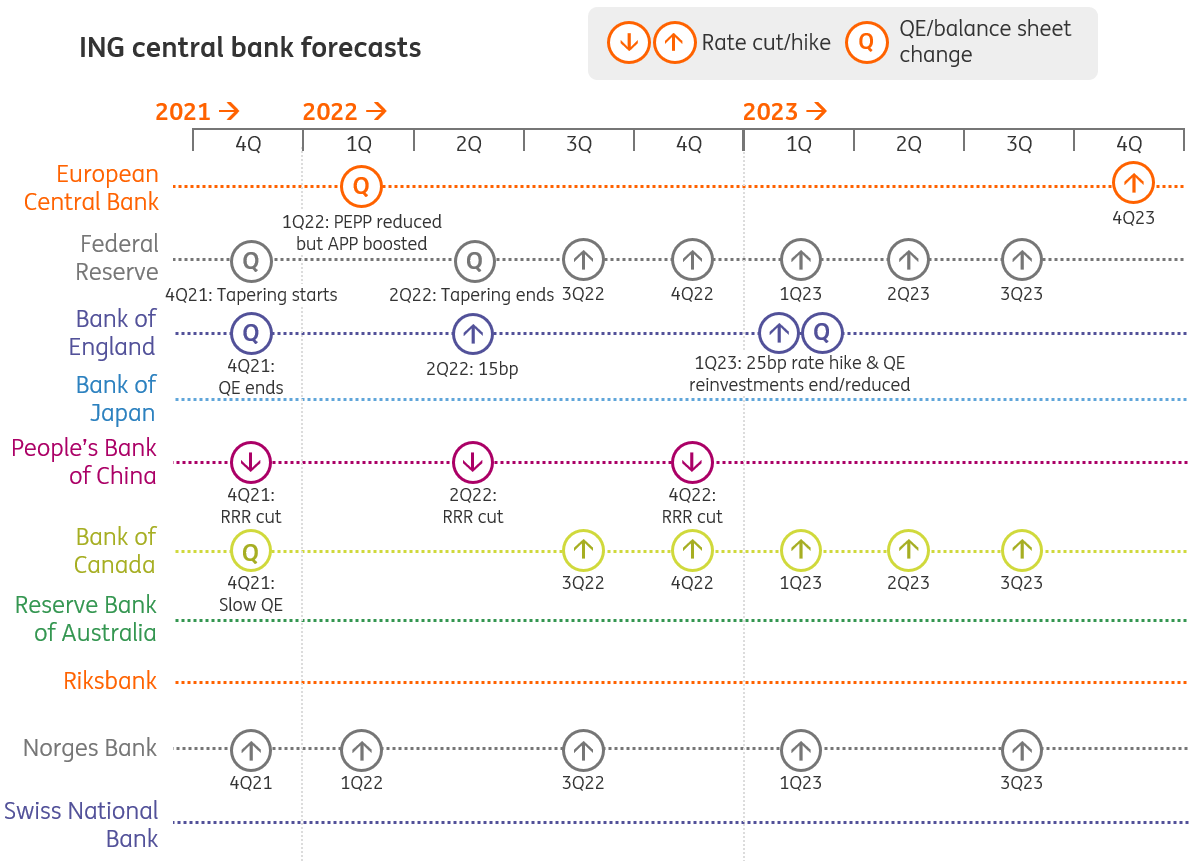

The central bank tightening timeline

Federal Reserve

After a soft patch in the third quarter, the early signs are that the fourth quarter should see a renewed acceleration in US growth and job creation now that the number of Covid cases is on a steep decline. At the same time, inflation pressures remain elevated as supply chain issues, production bottlenecks and labour market shortages mean that the supply-side capacity of the economy struggles to keep pace with demand.

The combination of cost-push and demand-pull inflation is unlikely to ease anytime soon and with the labour market improving again, the latest Fed commentary and forecasts suggest a consensus is building behind a 3 November quantitative easing taper announcement. This will lead to monthly QE asset purchases slowing from their current $120b rate down to zero by early summer 2022.

The Fed has been at pains to emphasise that the decision on QE is completely separate to the decision on interest rates. However, we forecast that the strong growth story will continue, with the risk being supply-side constraints don’t ease as quickly as hoped. Our suspicion is that inflation stays higher for longer with the Federal Reserve responding with interest rate hikes in September and December next year.

European Central Bank

The ECB’s new dovishness of the summer has gradually been replaced by a more balanced inflation assessment in recent weeks. While the ECB’s base case scenario, with an inflation forecast clearly below 2% in 2023, would argue for even more policy accommodation, the rise in headline inflation and the increasing risk of second-round effects materialising argues for more caution. And, indeed, since the ECB’s September meeting, the Bank's tone on inflation has become somewhat more cautious and balanced.

The December meeting, with a fresh set of macro-economic projections, will be a very intense one with heated debates between the doves and hawks. The focus of the discussion should not be about whether the Pandemic Emergency Purchase Programme is stopped in March but rather what size of asset purchases will be needed going into the second half of 2022.

We expect a first announcement on asset purchase reductions at the end of this year. This will mean a rotation out of PEPP into the Asset Purchase Programme and initially only a very gradual reduction of total purchases. However, the ECB’s new stance on inflation could lead to a faster and more significant reduction of monthly asset purchases in the second half of 2022.

Bank of England

We now expect the first Bank of England 15bp rate hike in May 2022, earlier than we'd previously pencilled in, followed by another 25bp move in 1Q23. At that point, the BoE will also likely begin passively shrinking its balance sheet. This involves ending reinvestments linked to the bonds accumulated under successive rounds of QE.

All of this follows some hawkish comments from policymakers over recent weeks, which suggests they aren't going to hang around longer than a year before tightening policy. Still, markets are probably getting ahead of themselves by pricing almost three rate hikes by the end of 2022.

Investors are inferring that the rise in electricity prices - and the resulting spike in inflation - will pressure the Bank to raise rates, concerned perhaps about the feed through to longer-term inflation expectations. But we think if anything rising energy prices, which coincide with tighter fiscal policy, is a dovish factor. The pace of rate hikes instead relies on the increased rates of wage growth we're seeing for the likes of lorry drivers and food workers becoming more widespread. This isn't a given, seeing as jobs market slack is also rising now the furlough scheme has ended.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

7 October 2021

ING Monthly: Starting the great rotation This bundle contains 11 Articles