ING’s outlook for central banks

Our economists look at the places where monetary policy is likely to be tightened first over the next few years

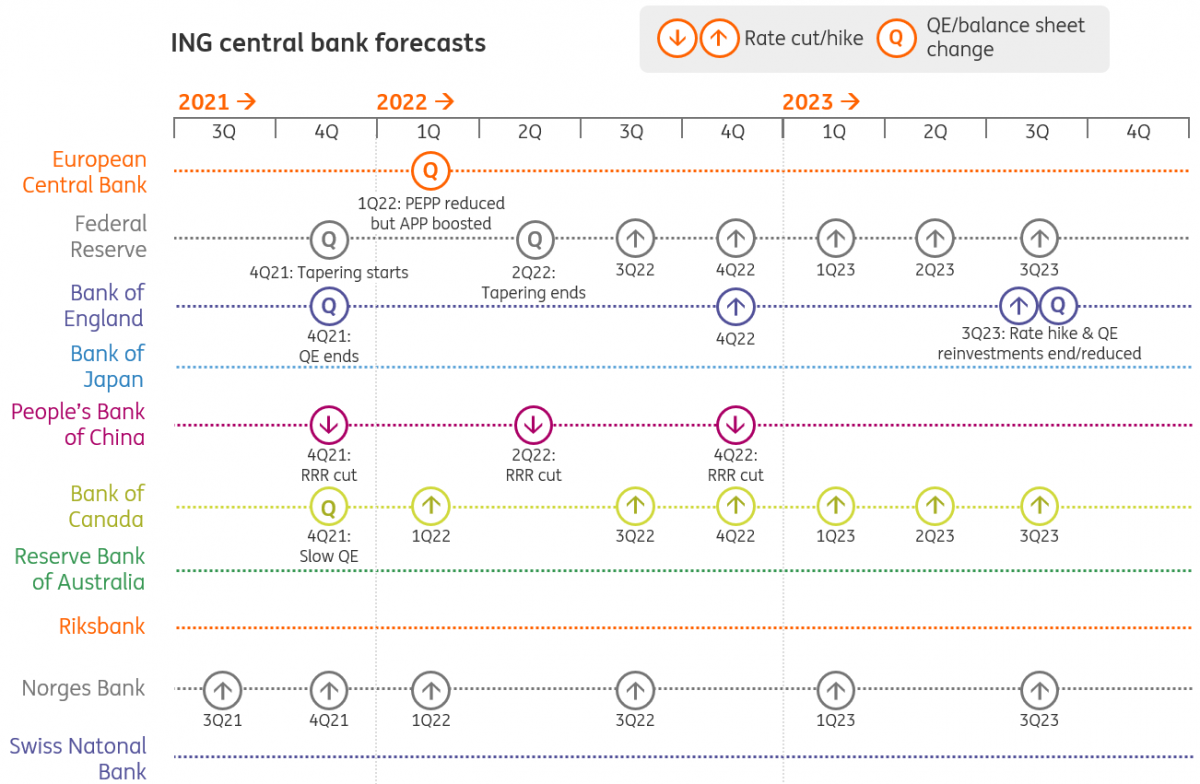

The race to hike interest rates and end QE

Federal Reserve

More and more Federal Reserve officials believe that it is time to “dial back” on the policy stimulus. Fed Chair Jerome Powell has been more cautious, but he too now recognises it “could” be appropriate to taper the $120bn per month of quantitative easing this year. His wariness stems from the resurgence of Covid and the sense that an “ill-timed policy move” could be “particularly harmful”.

Moreover, while “substantial further progress” has been made with regards to inflation, there are still 5.7mn fewer people in work than in February 2020, meaning there is still “much ground to cover to reach maximum employment,” according to Powell.

Consequently, a huge gain in August nonfarm payrolls will be needed for him and other Fed governors to support a September taper announcement. It looks as though a November agreement with a December starting point is the most likely path ahead.

In terms of rates we remain optimistic on growth, but supply chain disruptions and labour market shortages may not ease as quickly the Fed anticipates. We see inflation staying higher for longer, and with additional fiscal spending hitting the economy we expect the Fed to start hiking interest rates in the latter part of 2022.

European Central Bank

Over the summer, the ECB has clearly become more dovish with its new monetary policy strategy and the clear intention of bringing inflation expectations sustainably back to 2%. This means that the ECB will continue its benign stance on inflation and keep everything unchanged. Even an end to the front-loading of asset purchases looks unlikely as it would de facto mean earlier tapering in the eurozone than in the US.

We expect a first announcement of asset purchase reductions at the end of this year. This will mean a rotation out of the Pandemic Emergency Purchase Programme into the Asset Purchase Programme and only a very gradual reduction of total purchases. Consequently, the ECB will not be in a hurry to completely unwind QE.

With the new dovishness, a first rate hike should not be expected before 2024.

People's Bank of China

The PBoC is expected to continue cutting the reserve requirement ratio (RRR) in 4Q21, following a cut in July, to ease the rising pressure from credit costs. The economy is currently facing challenges from reforms in the real estate, technology and education sectors, as well as chip shortages that have affected production. Occasional localised Covid-19 lockdowns have also affected air and marine freight operations.

The RRR cut has been effective in lowering bank lending rates and bond yields. Further easing from monetary policies will be needed given the risks stated above are not going away for the rest of 2021. The anticipated RRR cut can help to put further downward pressure on market interest rates. It is therefore unlikely that the PBoC will need to cut policy interest rates unless economic growth were to slow excessively, which is not our base case scenario.

Bank of England

While the Bank of England doesn’t explicitly tell us when the first rate rise will come, its latest forecasts effectively endorsed market expectations from late July. At that point, investors were pricing the first (partial) rate rise in mid-2022 with another 25bp move around a year later.

In practice, that’s unlikely to be too wide of the mark, but we are a little more cautious than the BoE on a few key parts of the outlook. We think inflation is likely to fall more quickly back to target next year, and we disagree with the Bank’s prediction that there will be no rise in unemployment when the furlough scheme ends this month.

We’re now pencilling in the first rate rise in the final quarter of 2022, with another in the second half of 2023. The Bank has signalled this latter move will be accompanied by the end of reinvestments of its pool of government bonds, which were accumulated under successive rounds of QE. This 'quantitative tightening' process will be a first for the BoE which, unlike the Fed, didn’t shrink its balance sheet in the post-crisis years.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

2 September 2021

ING Monthly: Back from the beach, into the breach This bundle contains 11 Articles