Industrial Metals Monthly: US copper tariff risks pull more metal to the US

Our monthly report looks at the performance of iron ore, copper, aluminium, and other industrial metals. In this month’s edition, we take a closer look at copper and what Trump’s potential tariffs could mean for the metal’s trade flows and prices

US President Donald Trump has signed an executive action plan directing the Commerce Department to start an investigation into the threat that copper imports pose to national security and recommend ways to mitigate any such threat. Mitigation efforts may include “potential tariffs, export controls, or incentives to increase domestic production,” the order says.

The department has up to 270 days to report back to Trump. Many uncertainties remain, including which products will face tariffs and the rates on those imports.

Copper from Canada and Mexico has been exempt in all forms from tariffs under the United States-Mexico-Canada trade agreement (USMCA) for now. Tariff concerns are already shaking up global markets, leading to price dislocations from New York to Shanghai.

Tariff concerns deepen price dislocation

The likelihood of tariffs has triggered a sharp rally in Comex prices, widening the gap with equivalent prices in London, with Comex futures trading near a record premium to those in London.

Prices in the US are up more than 25% so far this year, while the benchmark LME price is around 13% higher year-to-date as copper continues to benefit from the front-running of tariffs.

There is a further upside risk for copper prices in New York if tariffs are applied; however, the spread risks a pullback if any potential tariffs fall short of expectations.

Comex copper trades near record premium to LME

CME copper stocks keep rising

The threat of tariffs has led to traders shifting metal from the global LME warehouses to the US to take advantage of the arbitrage. CME copper stocks have been rising steadily since Trump's presidential election win. The bulk of the shipments coming into the US have been from South America, but some have been also arriving from Asia. At the same time, LME stockpiles saw modest declines.

The investigation may take months, allowing more metal to be shipped to the US before tariffs are imposed. The US copper rush could leave the rest of the world tight on copper if demand picks up more quickly than expected.

Movements in copper have been reflecting trends in other metals. Aluminium and steel prices, for instance, have surged in the US compared to international prices as Trump imposed 25% tariffs on all US imports of both metals

Copper inventories at major exchanges

Meanwhile, the cancellation of copper warrants in the LME has soared since late February, with the largest drawdowns seen in Asia’s inventories, followed by those in Europe. Orders to withdraw metal out of LME warehouses in Asia have surged to the highest level seen since August 2017.

LME cancelled warrants surge

US import reliance

The US is reliant on copper imports for its domestic consumption. Chile is the country’s biggest supplier at 41%, followed by Canada at 27%. The US imported around 850,000 tonnes of copper (excluding scrap) in 2024, accounting for around 50% of its domestic consumption. It might be challenging to fill that gap with domestic production. These flows of imported metal are likely to continue.

US copper imports by country (2024)

US copper imports by type (2024)

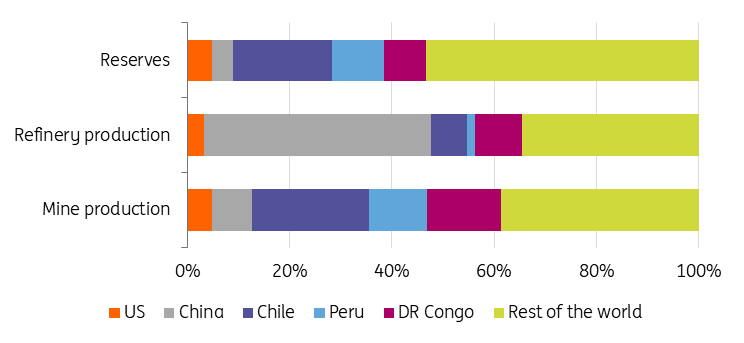

The US produces around 5% of global copper mining output. Its reserves are also at around 5% of the total, according to the US Geological Survey (USGS). The country’s production has been on a downtrend, dropping about 20% over the last decade. Last year, US copper production fell 3% following an 11% drop in 2023.

The US produces around 5% of global copper mining output

Tariff risks offer short-term support

In the long term, tariffs could be bearish for copper and other industrial metals in the context of slowing growth and keeping inflation higher for longer. If US inflation remains persistent or rebounds, it could prompt the Federal Reserve to delay or increase interest rate cuts. With growth in the US likely to slow on the back of tariffs and China already struggling to revive its economy, demand for copper and other industrial metals is likely to weaken looking ahead.

In the near term, however – as the US investigation into copper imports continues – copper prices are likely to remain supported by the front-running of tariffs and tightening of the ex-US physical market as more metal makes its way to the US ahead of any potential levies.

Until the result of the investigation becomes clear, US import demand triggered by potential tariffs will continue to offset headwinds from slowing global growth and higher inflation as the trade war ramps up.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article