Industrial Metals Monthly: Aluminium rally foiled

Our monthly report looks at the performance of iron ore, copper, aluminium and other industrial metals. In this month’s edition, we take a closer look at aluminium and discuss where we see prices heading in the second half of the year

YTD metals performance %

Aluminium rallies in May

Aluminium prices on the London Metal Exchange surged to the highest level in two years at the end of May. The increase was mostly driven by investment money moving back to commodities after a surge in copper prices.

Copper and aluminium surge to new highs in May

Surge in investment money pushes aluminium higher

After Rio Tinto declared force majeure on alumina cargoes from its Queensland refineries due to shortages of gas to power its operations, supply risks helped to push the aluminium price higher. The force majeure will only affect third-party export supply, and supply to Rio’s own smelters will remain unaffected. The cuts have raised concerns over whether they will impact aluminium supply; however, we do not believe this is the case.

Since then, the aluminium price has fallen about 9% amid concerns about elevated global inventories, profit-taking by investment funds, and weak demand from China. Meanwhile, copper is down about 10% from its all-time peak reached last month.

Despite the rally in May, we believe aluminium’s fundamentals have not changed significantly and prices are now vulnerable to further downward correction. The supply and demand outlook remains fairly balanced for 2024, while investor interest has been fading.

LME stocks jump to the highest level since October 2021

LME aluminium stocks saw their largest daily inflow in early May, driven by deliveries into Malaysian warehouses. By the end of May, total aluminium inventories rose 128% on the month.

Following these large deliveries – reported to be from Trafigura group – the wait time to take delivery of aluminium on the LME jumped to over five months from zero. The latest data from the exchange shows a wait time of 159 days for the delivery of aluminium at warehouses in Port Klang in Malaysia at the end of May. This is the longest wait queue reported in the LME system since June 2021, when there was a wait time of 168 days.

Russian share of LME aluminium falls

The Russian share of aluminium on the LME plunged last month. Russian metal accounted for less than half (42%) of the aluminium stored in LME warehouses in May. This is down from nearly 90% a month earlier, as shown by the latest data from the LME.

The volume of Russian aluminium in LME warehouses rose to 246,950 tonnes, up from 116,325 tonnes. Despite the surge, the volume as a proportion of total inventory dropped following a large inflow of metal of Indian origin. Volumes of Indian material rose to 293,325 tonnes from 12,275 tonnes, with the share of Indian metal on the LME increasing from 9% in April to 50% last month. This follows large deliveries that occurred in Port Klang last month.

The LME banned delivery of newly produced Russian metal in April following US and UK sanctions.

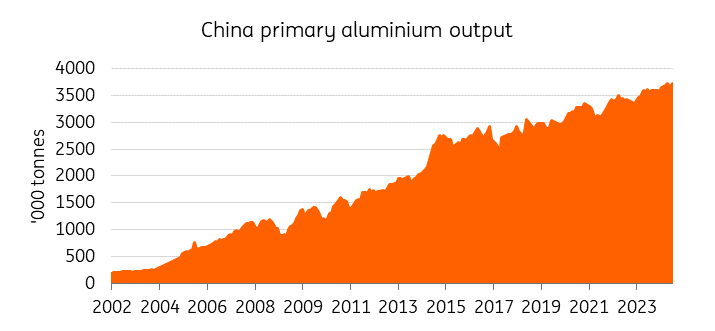

China aluminium output is increasing

Chinese production is set to increase in the coming months, mainly due to the steady recovery of power supply in Yunnan, with the remaining idled capacity continuing to slowly resume production. We expect China’s primary aluminium production to grow by around 2% in 2024 to around 42 million tonnes.

High aluminium prices, low energy costs might bring more European restarts

In Europe, smelter margins are healthy amid high aluminium prices and weaker energy costs, and might bring more announcements of restarts – which would be bearish for the aluminium price. Europe's aluminium sector was one of the worst affected industries during the energy crisis. The metal is one of the most energy-intensive to produce. More than one million tonnes per annum was taken offline during the energy crisis, but we are starting to see some announcements of restarts as power prices have retreated sharply from the highs seen during the crisis. In the first quarter, a restart began at Trimet’s St. Jean smelter in France and more announcements are likely throughout the year.

Speculators cut net bullish bets

Speculators have decreased their bullish LME aluminium bets by 3,670 net-long positions to 133,439, as shown by weekly exchange data on futures and options. The net-long position was the least bullish in more than two months.

LME net bullish bets fall to two-month low

Cautious Fed could provide a headwind

US monetary policy will also be important for the direction of aluminium prices. Elevated rates and a stronger dollar have been a drag on industrial metals over the past two years.

Our US economist believes that under the right conditions – i.e., more evidence of easing inflation pressures, labour market slack and softer consumer spending – the Fed will seek to move monetary policy from “restrictive” to “slightly less restrictive” with a 25bp rate cut at its September FOMC meeting.

However, if US rates stay higher for longer, this would lead to a stronger US dollar and weaker investor sentiment – which in turn would translate to lower aluminium prices.

Aluminium may see more downside

We have revised our LME aluminium price forecast slightly higher to reflect the investor-led increase to a new two-year high in recent weeks. We now forecast a second quarter average of $2,550/t from $2,500/t previously.

However, we then expect prices to move lower in the next few months to average $2,500/t in the third quarter, as the recent increase was mostly driven by investment money and there is now a probability of more profit taking.

Following this, we see prices rising again in the latter part of the third quarter as demand starts to improve, with the fourth quarter averaging $2,550/t. The second half of the year should also be the starting point for Fed rate cuts. There is a risk, however, for demand to weaken further if high inflation keeps interest rates high. We see prices averaging $2,460/t in 2024.

ING forecast

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article