Industrial Metals Monthly: Iron ore tumbles below $90 as China gloom deepens

Our monthly report looks at the performance of iron ore, copper, aluminium, and other industrial metals. In this month’s edition, we take a closer look at iron ore, the worst performer in the complex, and discuss why we believe the risks are skewed to the downside for the rest of 2024

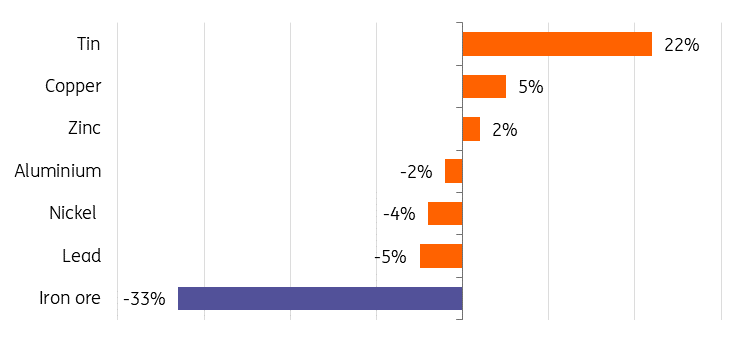

YTD metals performance %

Iron ore is one of the worst-performing commodities so far this year, with prices now down about 33% year-to-date and sinking below $90 for the first time since 2022. We believe price risks are increasingly skewed to the downside for the industrial metal as the outlook in China, the biggest buyer, continues to deteriorate.

China gloom deepens

Iron ore is among the most vulnerable to China's slowdown risks as the country's property market constitutes the bulk of steel demand. Looking ahead to the rest of the year, fundamentals are still pointing to the downside for iron ore.

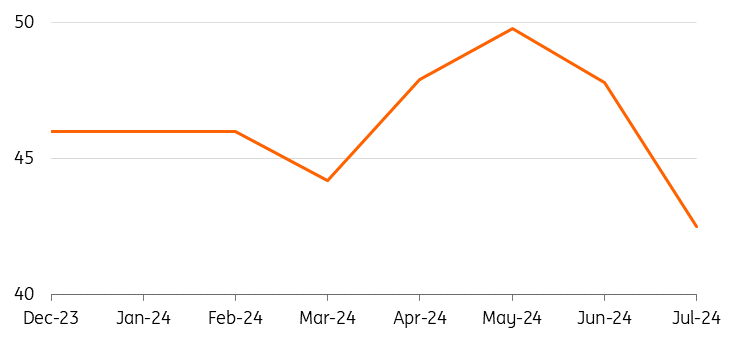

The latest data from China underwhelmed again. The official manufacturing PMI declined to 49.1 from 49.4 in July. The reading has been below the 50-mark separating growth from contraction for all but three months since April 2023. Meanwhile, China’s steel industry PMI remained in contraction, falling to 40.4 in August after a reading of 42.5 in July.

China steel industry PMI remains in contraction

China's housing data worsens

At the same time, the prolonged crisis in China’s property market doesn’t show signs of bottoming out. The latest property sales data showed a worsening residential slump. The country had 382 million square meters of unsold new homes as of July, according to the latest official data.

Meanwhile, the country’s new home starts – the biggest steel demand driver – have fallen sharply so far this year, and are down by more than 20%. This should continue to suppress steel demand this year.

Without further stimulus measures, there is little hope for a near-term recovery for the property and construction sector. We believe this continued weakness in the sector remains the main downside risk to our outlook for iron ore.

China home sales worsen in August

China’s steel industry has raised alarm about how tough conditions can become. Baowu Steel Group, the world’s largest steel maker, warned last month that the steel sector was facing a long, cold winter that could be worse than previous steel crises of 2008 and 2015.

China’s steel prices plunge to lowest since 2017

Iron ore produced by major miners

On the supply side, total iron ore production from the top four iron ore producers – Vale, Rio Tinto, BHP and Fortescue – reached 259 million tons in the first half of the year, up 1.4% from the first half of the year in 2023.

China iron ore port inventories keep piling up

High iron ore stocks pressure prices

Iron ore port holdings in China continue to rise, back above 150 million tonnes and standing at their highest ever for the time of year, a sign of abundant seaborne supplies. China’s iron ore port inventory is a key indicator that reflects the supply and demand balance, as well as the safety net and imbalance between the iron ore supply and the steel mill demand.

Iron ore imports have also been increasing, up 6% in the first half of the year compared to the first half of 2023. However, Chinese demand growth may be insufficient to absorb the extra imports.

We believe high iron ore availability in China will continue to put pressure on prices.

Risks skewed to the downside

We expect iron ore prices to fall further this year amid subdued demand and sufficient supply. Downside risks are likely to prevail in the near term amid subdued steel demand. We believe China will continue to drive iron ore prices going forward and the supply and demand balance will largely depend on China’s steel demand outlook.

With the recovery path for China still bumpy, we believe iron ore will remain sensitive to Chinese policies. Prices are therefore likely to remain volatile, at least in the short term. A further boost for China’s property sector will be crucial in supporting demand. We see prices averaging $100/t in the third quarter and $95 in the fourth quarter, with a 2024 average of $106/t.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article