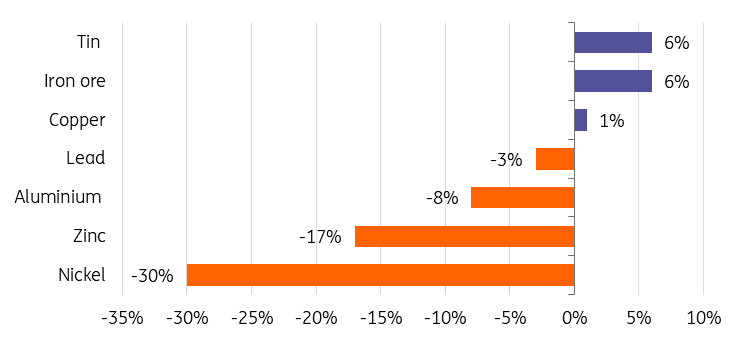

Industrial Metals Monthly: China’s stimulus in focus

- 7 September 2023

- Commodities, Food & Agri

Our monthly report looks at the performance of iron ore, copper, aluminium and other industrial metals, as well as their outlook for the rest of the year. In this month's edition, we take a closer look at the recent impact of new stimulus measures introduced in China

Metals markets assess China policy

China ramping up economic support

A mixed picture of China's economy has been painted by the latest releases of official PMI data. While the manufacturing index increased slightly to 49.7 – its third consecutive rise since the lows of 48.8 seen in May – it's still falling short of the 50-level mark associated with expansion.

The non-manufacturing series, which had reflected the bulk of the post-reopening recovery, fell further in August. At 51.0, the index was a little lower than the forecast figures of 51.2 but at least remains slightly above contraction territory.

The introduction of China's latest stimulus measures emerged after home sales plummeted to the lowest point seen in over a year

Meanwhile, the Chinese government has moved forward with a series of stimulus measures designed to turn around the flagging economy and its ailing property sector, which accounts for more than a quarter of China’s economic activity. Included in these measures was the decision to cut down payments and lower rates on existing mortgages. The nationwide minimum down payment will be set at 20% for first-time buyers and 30% for second home buyers. Mortgage rate cuts will be negotiated between banks and customers, and both policies will go into effect on 25 September.

The introduction of these measures came after China’s home sales slumped in August. Sales by the country’s largest developers fell 34% from the previous year, according to China Real Estate Information Corp. It was the deepest drop seen in over a year. Further stimulus packages could also be introduced, which could boost the need for industrial metals. So far, Beijing has remained reluctant to back major stimulus that might be necessary to put a floor under falling home sales.

News of a surge in home sales in two of China’s biggest cities has offered an early sign that government efforts to cushion a record housing slowdown are helping. Existing home sales for Beijing and Shanghai doubled over the last weekend (2-4 September) from the previous one. Reports of property developer Country Garden avoiding default with last-minute interest payments also restored some additional confidence in China’s property sector.

Until the market sees signs of a sustainable recovery and economic growth in China, we will struggle to see a long-term move higher for industrial metals

The metals markets will now be watching how sustainable this pickup in interest is and how long it will last. China’s recovery is still uncertain, and metals are likely to see some continued volatility for a while – at least in the near term. For the remainder of this year, the key factor for the direction of metals prices will be whether China will be able to stabilise its property market. Until the market sees signs of a sustainable recovery and economic growth in China, we will struggle to see a long-term move higher for industrial metals.

Fed pause bets bolster sentiment

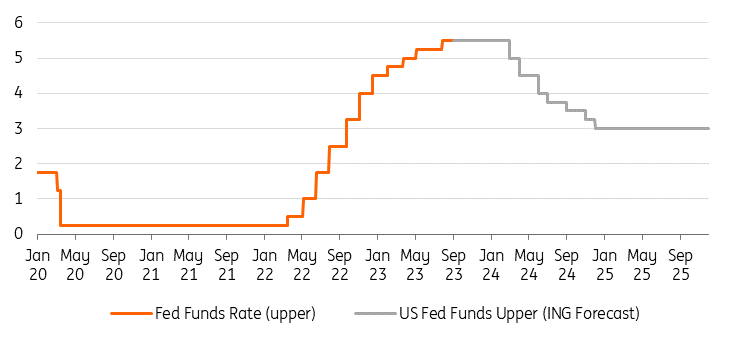

Sentiment in metals markets also received a boost after last week’s US jobs report that showed a steadily cooling labour market, offering the Federal Reserve room to pause rate hikes this month. Nonfarm payrolls increased 187,000 in August, while hourly earnings rose slightly less than the median economist forecast.

The central bank hiked rates by 25 basis points at its July meeting following the recent strength seen in economic data. At the Jackson Hole conference last month, Fed Chair Jerome Powell announced plans to keep policy restrictive until confidence that inflation is steadily moving down toward its target has been fully restored. Over the next few weeks, we'll be keeping a close eye on US data releases which could shed more light on what the Fed may do next.

Higher-for-longer interest rates will ultimately lead to a drop in metals prices

September appears set for a pause given recent encouraging signals on inflation and labour costs, but robust activity data means the door remains open for a further potential increase. Markets see a 50% chance of a final hike, while our US economist believes that rates have most likely peaked. US interest rates remaining higher for longer would lead to a stronger US dollar and weakening investor confidence, which in turn would translate to lower metals prices.

US rate cuts to start by the spring

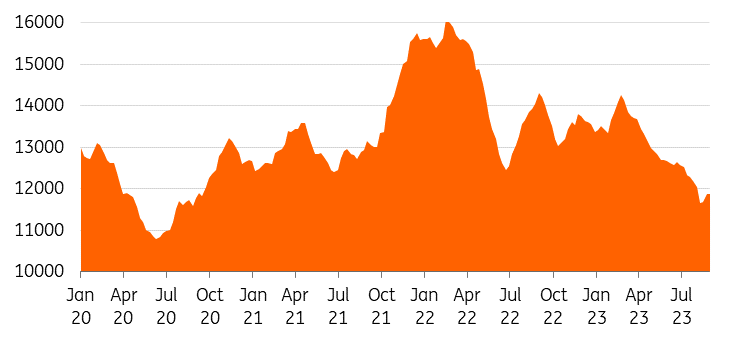

Iron ore rises on China property aid

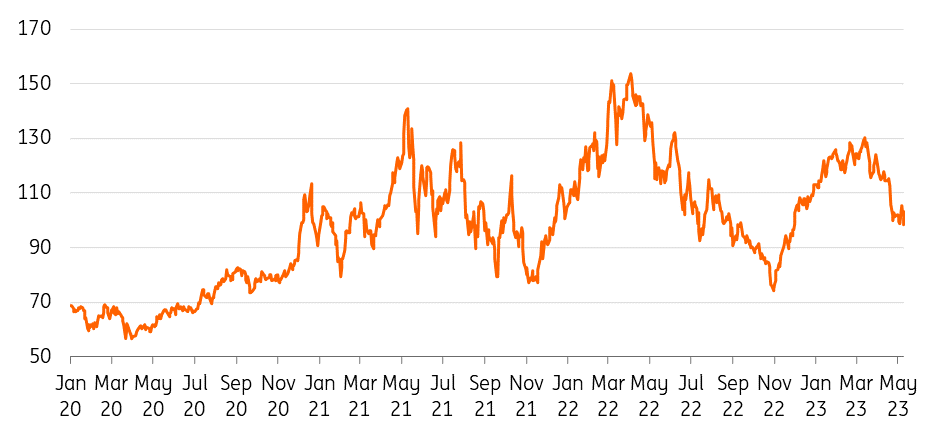

Iron ore prices held above the $100/t mark in August despite China’s worsening property crisis, which in typical years makes up about 40% of demand.

Iron ore has managed to stay above $100/t for most of 2023

Iron ore prices surged more than 15% over the past three weeks as China has continued its efforts to boost the steel-intensive property sector. Steel mills are also expected to ramp up as the building season begins again this month. However, the uncertainty around mandatory curbs will weigh on the outlook.

After China’s steel output climbed to a record of more than one billion tonnes in 2020, the government responded by ordering production cuts in each of the next two years to cut back on emissions and match supply with demand. The intensity and the timeline of production cuts this year are still unknown, but any steel output cut would add to bearish risks for the iron ore market.

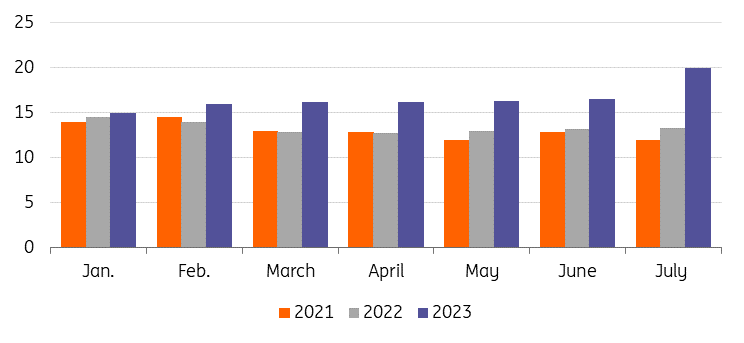

CISA daily average crude steel output at member companies

| 16% |

Drop in China's iron ore inventoriesJuly to August 2023 |

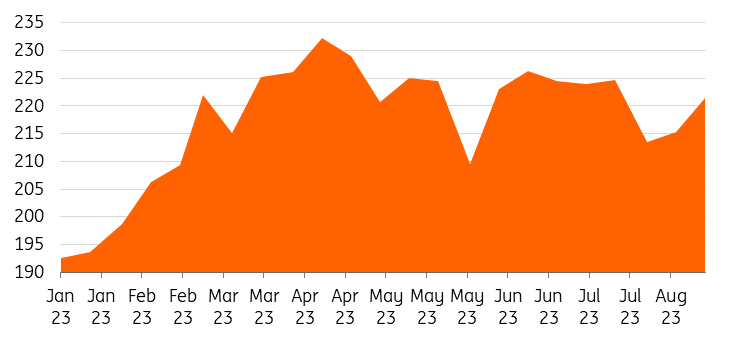

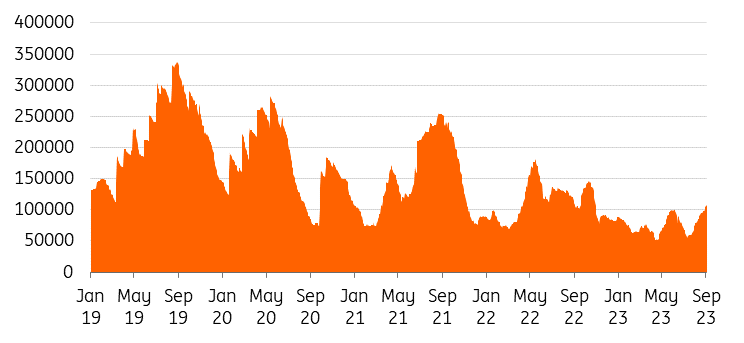

Meanwhile, China’s iron ore stockpiles are hovering around the lowest level since August 2020 as mills have been cautious about restocking amid property woes. From July to August, total iron ore inventories in China across major ports fell 16% to less than 120 million metric tonnes. However, the arrival of the construction season might encourage domestic mills to start restocking. China's iron ore imports in August were at their strongest in almost three years at 106.415 metric tonnes. Low inventories should also support iron ore’s price at elevated levels.

China iron ore total ports inventory

With the supply side largely stable, it will be demand in China that will continue to drive iron prices moving forward

The supply side has been largely stable, with total iron ore production from the top four miners (Vale, Rio Tinto, BHP and Fortescue) ticking up to 539 million metric tonnes in the first half of the year – 4% higher than a year earlier. We believe that with the supply side largely stable, it will be demand in China that will continue to be the main driver for iron prices moving forward. We believe prices will remain volatile as the market continues to respond to any policy change from Beijing.

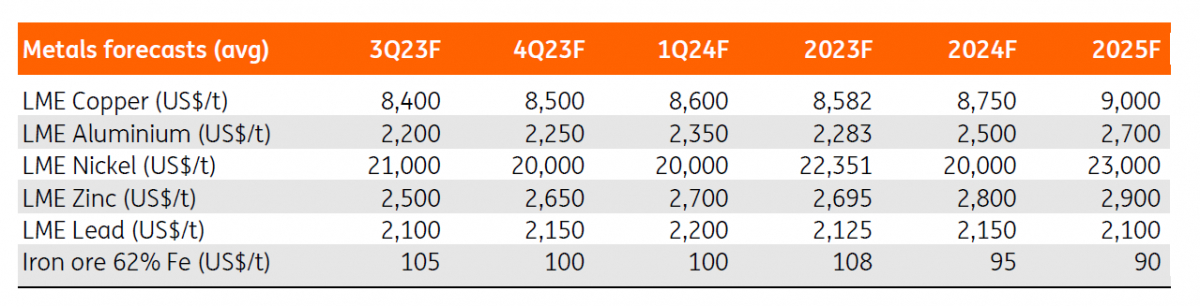

We expect prices to average $105/t in the third quarter, with seasonal demand supporting. We're expecting $100/t in the fourth quarter and we see the 2023 average at $108/t. Risks will remain to the downside heading into year-end amid China steel output cuts, an uncertain outlook for the property sector and healthy supply.

Copper struggles for direction

Against the backdrop of an uncertain path of US rate hikes and China’s lacklustre economic recovery, copper has been struggling for direction lately. Beijing’s latest measures to support the housing market helped copper make a recovery from a low in mid-August, but it has failed to hold above the $8,500/t mark.

After two weeks of rising prices, copper is falling again as the market assesses the effects of China’s measures to support its property market and how they might translate into demand for industrial metals.

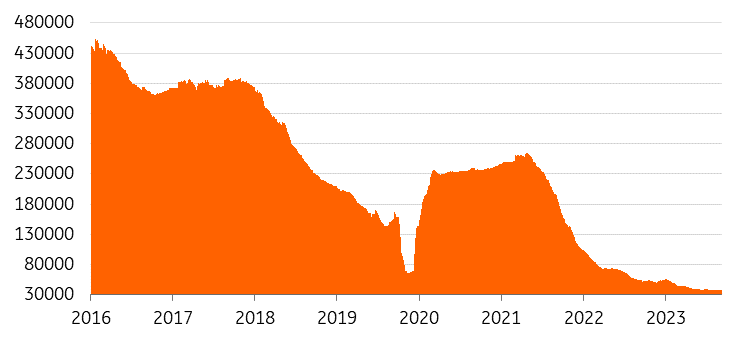

LME copper warehouse stocks have been rising

Copper’s inventory levels in LME warehouses have been growing, up more than 40% in August after doubling in July. This shows clear signals of weakening demand. They do, however, remain at historical lows. We believe low inventories fuel the possibility for spot prices to rise rapidly if consumption picks up sooner than expected.

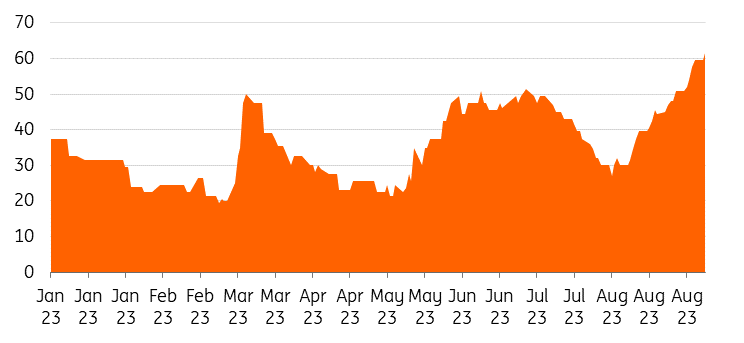

China’s imported copper demand is showing signs of improvement

The Chinese market has just entered a peak demand season, which should be supportive for copper prices in the near term. China copper ore and concentrate imports are up 9% year-to-date to 18.104m tonnes, while imports in August climbed to all-time highs at 2.697m tonnes ahead of a seasonal pick-up in demand.

A boost for China's property sector will be crucial in supporting demand going forward.

Signs of improvement are also emerging for China’s imported copper demand. The Yangshan copper cathode premium – which usually serves as an indicator of China’s import needs – has steadily been moving up over August to stand at $58/mt compared to a year-to-date low of $19.50/mt in March. Still, it remains even below the post-pandemic average of around $65/mt. A boost for China's property sector will be crucial in supporting demand going forward.

We remain wary about the short-term outlook for copper, and China remains a key source of caution. We believe commodity-intensive stimulus is needed to support short to medium-term demand growth. In the longer term, we believe copper’s supportive decarbonisation trend should support prices.

We maintain our price forecast at $8,400/t in the third quarter and $8,500/t in the fourth quarter, taking the 2023 average to $8,582/t.

Nickel underperforms

Nickel has been the worst-performing metal on the LME so far this year, with year-to-date prices down more than 30%. One of the key drivers of the price decline has been the disappointing recovery in Chinese demand, with nickel prices dropping to a one-year low in August. We believe this underperformance is likely to continue amid a weak macro picture and sustained market surplus, with supply from Indonesia continuing to surge to meet the growing demand from the battery sector. In the past, market surpluses have been due to Class 1 nickel – but in 2023, the surplus will be on account of Class 2 nickel.

| 34.5% |

Rise in Class 1 nickel outputIn China from 2022 |

LME nickel stocks are critically low

The LME’s Class 1 nickel stocks are critically low. However, we believe that LME’s new initiative – which has reduced waiting times for approving new brands that can be delivered against its contract – could potentially increase inventories.

China's refined Class 1 nickel output has been increasing in 2023

China’s refined Class 1 output has seen a solid increase in 2023 in response to historically elevated LME prices, and we believe Chinese producers will continue to submit fast-track LME nickel brand applications. This will allow them to deliver their Class 1 material to LME warehouses. The LME has already approved nickel produced by Quzhou Huayou Cobalt New Material Co, a subsidiary of China's Zhejiang Huayou Cobalt Co, as a listed brand in July. GEM Co. Ltd., a subsidiary of Jingmen Gem Co. Ltd. also applied last month to become an LME-deliverable brand.

China’s refined Class 1 nickel output jumped 34.5% year-on-year to 129,400 metric tonnes in the first seven months of the year. This was faster than the 33.9% year-on-year increase in the country’s total output of battery-grade nickel sulphate over the same period, according to data from Shanghai Metals Market. Shanghai Metals Market estimates that 145,300 t/y of new refined class 1 nickel production capacity will be added in China this year.

We forecast nickel prices to remain under pressure in the short term as a surplus in the global market builds and a slowing global economy mutes stainless steel demand. We see prices averaging $21,000/t in the third quarter and $20,000/t in the fourth quarter. However, the downside will be limited due to tightness in the LME deliverable market.

Prices should, however, remain at elevated levels compared to average prices seen before the historic LME nickel short squeeze in March last year due to nickel’s role in the global energy transition. The metal’s appeal to investors as a key green metal will support higher prices in the longer term. We believe that demand for use in electric vehicle batteries remains a key factor for the longer-term narrative for nickel.

ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more