Is the increase in Reverse Yankee issuance a tailwind for EUR/USD?

Following April’s widening of USD spreads relative to EUR corporate borrowing costs, and the still narrow spreads in the cross-currency basis swap, it is no surprise that Reverse Yankee issuance – US corporates borrowing in EUR – has picked up sharply. Occasionally, this activity gets linked to demand for EUR/USD. We take a look at this relationship

A cost-saving advantage for US issuers going to EUR market

We expect an increase in Reverse Yankee issuance in 2025, as market conditions have aligned to offer cost-saving opportunities for US issuers. This trend is already evident, particularly in recent weeks, with a notable uptick in EUR-denominated bond issuance by US corporates. Year-to-date, corporate Reverse Yankee supply has reached €42bn, the highest YTD level on record. Issuers like McDonald's, AT&T, Alphabet, Pfizer, Visa and Morgan Stanley have already brought dual-tranche transactions in the past month.

USD credit has been the underperformer during recent market volatility as risks on the US side are perceived to be higher for now. Of course, USD credit is coming from a much more expensive place and has more room to swing wider. Thus, the cross-currency basis swap equation will continue to offer a cost-saving advantage for US issuers to come to the EUR market and swap back. This is in addition to US issuers also financing their European operations at a lower yield level.

The increased differential between EUR and USD spreads creates a lower cost of issuance in euro, particularly as the cross-currency basis swap remains at historically very low levels. We expect this basis to stay anchored at these very low levels of between 0-5bp.

USD credit will likely remain on the wider end of the range and continue to come under more pressure than EUR credit. This has already been reflected in mutual fund and ETF flows, whereby the outflows in USD were much more drastic during the April volatility, matched with the general slowdown of inflows since late last year. On a YTD basis, USD IG fund inflows only amount to around 1% of assets under management, versus EUR IG inflows of nearly 3%.

Cross-currency basis swap & USD-EUR Spread differential - 5yr

Reverse Yankee supply booms

We forecast corporate Reverse Yankee supply to reach up to €85bn in 2025, from the current YTD figure of €42bn. This will mark the second-highest year for Reverse Yankee supply on record, after the €98bn of 2019. Opportunistic funding will be the large driver for the increase in supply. Additionally, redemptions for Reverse Yankee bonds rise in 2025 up to €47bn, an increase from €39bn maturing in 2024.

Corporate Reverse Yankee supply (€bn)

Normally, financial Reverse Yankee supply is relatively stable year-on-year, much of which is for European operations. However, with the attractive cost-saving advantage, supply has jumped up to €30bn YTD, matching the full year figure of 2024. As such, we will likely see record-breaking supply at €55bn, pencilling in above the €42bn in 2021.

Financial Reverse Yankee supply (€bn)

Reverse Yankee deals usually come with a marginally higher new issue premium to attract the investor; in any case, this supply will still be met with very strong demand. Higher reverse Yankee supply does drive EUR corporate supply higher and adds additional supply to the technical equation. Whilst there is still plenty of cash ready to be put to work in credit, and new issues continue to catch strong demand, the technicals are not as strong as they were several months ago, thus it becomes slightly less supportive for secondary spread developments.

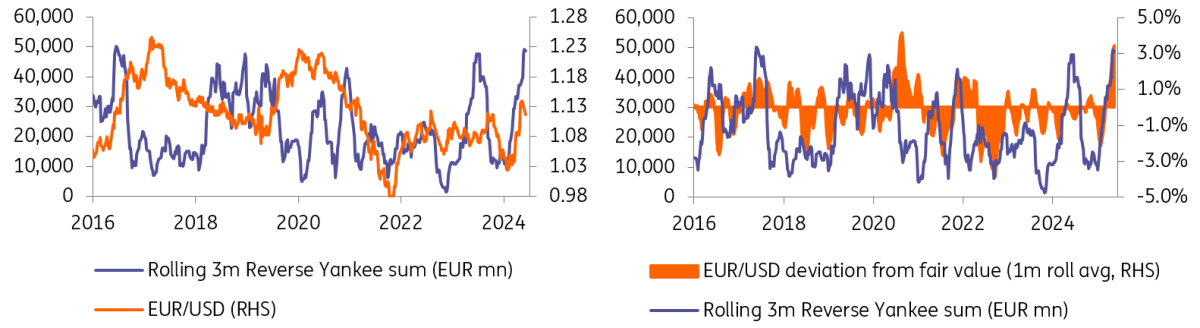

Could Reverse Yankee issuance create EUR/USD demand?

Periods of heavy RY issuance have occasionally been linked with a stronger EUR/USD. It’s not exactly clear why. From what we understand, RY issuance is normally targeted at investor groups who already manage a EUR portfolio – e.g. the European investment industry. And in the mechanics of the RY deal itself, there is no natural demand for the euro given that the issuer would be receiving the euros from a community that already owned them and would then undertake an FX swap to cover exchange rate risk over the life of the bond.

Where there could be euro demand is from cross-over or Absolute Return funds – making a choice to take on more euro risk relative to the dollar. We highlighted this in our Unipolar Disorder report, where we said we’re looking for any signs – perhaps in the fund flow data – that investors were starting to increase the preference for euro over dollar credit assets.

Additionally, one can argue that the sizes we’re talking about here – e.g. EUR25bn is a very good month for RY issuance – are still pretty small relative to the $420bn that changes hands each day in spot EUR/USD.

Looking at the data, it’s hard to pick out periods – apart from now – when RY issuance has had a meaningful impact on EUR/USD. Below we show both: EUR/USD spot versus RY issuance trends and EUR/USD spot versus the EUR/USD deviation from ING’s short-term Financial Fair Value model. The latter measure might be more relevant in that it shows where EUR/USD is trading relative to conventional drivers like rate spreads, global equity performance and yield curves.

We’d probably conclude here by saying that a pick-up in RY issuance certainly won’t hurt EUR/USD. And if marginal new buyers are coming in from the credit space, then at the margin that will help. But this all certainly plays into the current narrative of buy-side interest in products outside of the dollar domain.

Reverse Yankee Issuance trends versus EUR/USD

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article