Hungary’s record just got even better

Hungary's 4Q18 growth has just been revised up to 5.1%, which means the country has just posted its highest growth rate since 2004. The structure of the economic activity is imbalanced, but we see some improvements going forward

| 5.1% |

4Q18 GDP growthConsensus (5.0%) / Previous (5.1%) |

| Better than expected | |

Growth looks balanced on the production side

The detailed 4Q18 GDP release surprised us yet again as the Hungarian Central Statistical Office (HCSO) changed the advance reading by 0.1 percentage points to 5.1% year on year. This means that Hungary has posted its highest growth rate since 2004. But adjusting for working days and seasonal factors, the growth rate mildly declined to 4.9% in comparison to the previous quarter.

GDP growth revised up to 5.1% YoY in 4Q18

On the production side, the value added of services increased at a slower pace (3.9% YoY) in the fourth quarter. In line with the deceleration, services contributed slightly less to GDP growth in Q4 (2.3ppt). Value added in industry rebounded with a strong end to the year, posting an expansion of 4.1% YoY - the best figure in 2018. So the slowdown seen in services was more than counterbalanced by industry.

Services sector provides the majority of economic activity

Construction also decelerated to 20.4% YoY in 4Q18 due to the high base, and is still driven mainly by the pre-financed EU projects and the housing boom. The contribution of the construction sector came in at 0.9ppt - the second highest among the main sectors. Agriculture also provided a positive surprise with its 0.3ppt contribution. The effect of net taxes on products was strong again at 0.8ppt, and as this is basically the income of the government, we see this as a sign of strong economic performance and a retreating shadow economy.

Contributions to GDP growth – production side (% YoY)

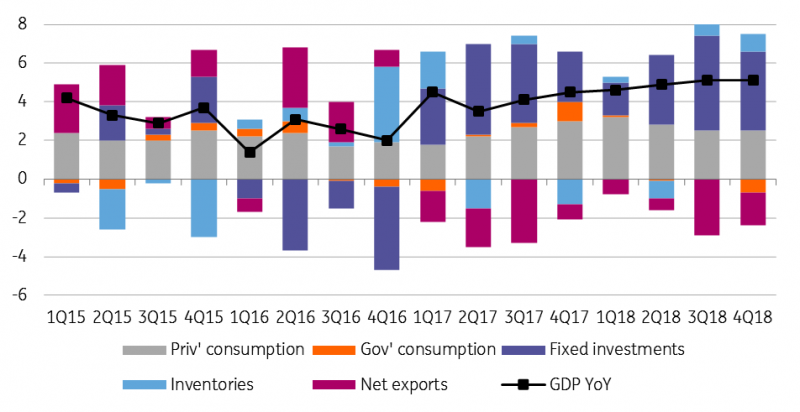

The expenditure side shows major imbalance

Taking into consideration the expenditure side, the main drivers behind GDP growth have remained the domestic factors.

The domestic use (actual final consumption and gross capital formation) added 6.8ppt to the economic activity, which means that the net export had a negative contribution reaching 1.7ppt. In absolute terms, the difference diminished somewhat from the 10-year high level reached in 3Q18, but still shows a significant imbalance between the internal and external drivers.

These developments also impact the current account balance which dropped to 1.2% of GDP. Going forward, if the Hungarian economy wants to stay away from a twin deficit (which is an explicit goal of the government), external drivers need to pick up, or domestic demand has to slow down. Otherwise, the economy will hit an unsustainable growth path (from a government point of view) going forward.

The difference between the domestic and external factors diminished somewhat

Within the domestic use, actual final consumption of households rose by 4.3% YoY, while the actual final consumption of government dropped by 7% YoY. The latter was coming from the base effect of a significant government spending ahead of the general election in April 2018. Overall, actual final consumption in total marked a 2.6ppt contribution to economic activity in 4Q18, 1.1ppt less than in the third quarter.

This 'loss' was way counterbalanced by the investment activity: the 17.2% YoY increase in gross fixed capital formation translated into a 4.1ppt contribution. Inventories also helped to spur growth by 0.9ppt as a lot of investments are on the pipeline which increases the inventories in the national accounts.

On the external side of the economic activity, we see the import growth outpacing the export’s, mainly on the back of the still strong domestic demand, affecting the import side. This difference translated into the 1.7ppt negative net export contribution.

Contributions to GDP growth – expenditure side (% YoY)

Growth will decelerate despite fiscal stimulus

The latest dataset contains some clues about the future as we saw the services sector decelerate along with the fading impetus of consumption. Investment activity is also likely to decelerate, albeit from a high point.

Our LeadING HUBE indicators also support our call for a loss of economic momentum in 2019. Real wage growth will decelerate on the back of a lower nominal wage growth combined with elevated inflation. Investment activity will decelerate as the EU projects end, and we also need to consider the expected global slowdown affecting external demand. However, the need for fewer imports will also help to improve net exports, and new export capacities can help to bridge the external issues at least temporarily.

For the time being, we see GDP growth slowing down to 4.0% in 2019 from 4.9% in 2018 and 3.0% in 2020.

Moreover, even the government is openly talking about the need for fiscal stimulus to maintain Hungarian growth around 4%, but at least 2ppt higher than the EU average. The recently announced ‘family support action plan’ might provide a minor boost to the economy, and we are also waiting for the soon-to-be-announced ‘economic protection action plan’.

But for the time being, we see GDP growth slowing down to 4.0% in 2019 from 4.9% in 2018 and 3.0% in 2020.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more