Why Hungary’s brighter labour market data should be taken with a pinch of salt

From a data perspective, recent labour market indicators have generally remained strong in Hungary. However, there are some nuances that warrant caution before we get too excited about the strength of the country's labour statistics

Recent data releases on the Hungarian labour market paint an encouraging but mixed picture. The trend in employment and unemployment over the past year shows a cooling of the Hungarian labour market, which still provides a positive overall picture. But the trend itself could be exploited by companies in their wage decisions. At the beginning of 2025, companies could be faced with a still sluggish economic environment and a sense of a softening labour market. As a result, they may be reluctant to grant strong wage increases – so what we saw in 2024 may not be repeated in 2025, and wage dynamics will not be as strong.

| 4.4% |

Unemployment rate (Oct-Dec)ING Forecast 4.8% / Previous 4.6% |

| Lower than expected | |

Positive surprise on the Hungarian labour market

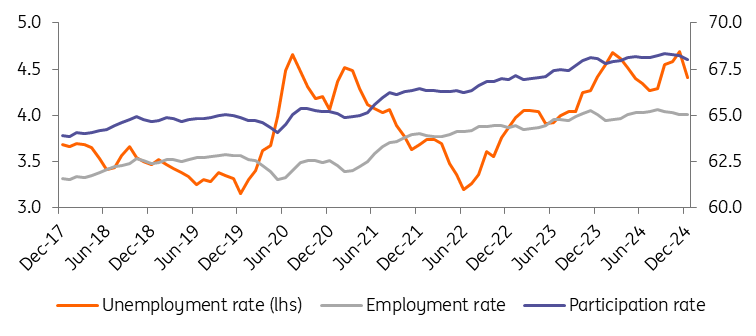

The latest labour market statistics from the Hungarian Central Statistical Office (HCSO) came as a big positive surprise, with the model estimate for December 2024 showing a decline in the unemployment rate to 4.3%. Meanwhile, the official data (the survey-based three-month moving average) also moved in a positive direction, with the indicator standing at 4.4% for the fourth quarter.

In terms of the unemployment numbers, the two statistics put the size of the group at around 210-216,000. The detailed data shows that in December, with a slight decrease in the population, the number of inactive persons increased more significantly (by 9,000 persons). Overall, the number of people participating in the labour market fell by almost 12,000. At the same time, the number of those unemployed fell significantly and the number of those employed fell slightly. All this paints a picture of a greater shift towards inactivity than towards employment. In this case, while the main labour market indicators show a positive change, this is essentially due to a fall in labour supply rather than a real positive development, i.e., an increase in labour demand.

Historical trends in the Hungarian labour market (%, 3-m moving average)

Of course, no serious structural conclusions should be drawn from one month's estimated data. However, if we look at the four quarters of 2024 and the official survey data, we can say that the last quarter of 2024 was the weakest in terms of employment and participation. In other words, if we look at the year as a whole, we see a worsening trend, as labour supply has fallen – partly for natural reasons and partly for those that were deliberate – while labour demand has also fallen. But the same could be seen in the labour hoarding statistics, which showed a declining hoarding rate at the end of the year, mainly due to redundancies and not as a result of an actual improvement in labour demand.

The decline in the labour market slack is keeping the labour market tight. This process could be exacerbated by the introduction of new production capacities in the manufacturing sector, which could represent a significant absorber of labour market slack. It will be interesting to see how the stricter legal requirements for the employment of third-country nationals in Hungary will evolve in the light of the tight domestic labour market and the expected pick-up in labour demand.

In 2025, however, the positive effects mentioned above may be tempered by the recent decline in consumer and business confidence, suggesting that the economy may again prove weaker than expected. Against this backdrop, firms that are still holding on to their workforces may make further cutbacks. In addition, the supply of labour may be further reduced by demographic factors. All in all, we see an improving positive change in the level of the unemployment rate, but less so in the "real" trends. In numerical terms, this could mean an average unemployment rate of around 4% for 2025 as a whole.

| 11.9% |

Average wage growth (November)ING Forecast 12.0% / Previous 12.5% |

| Lower than expected | |

Wage growth remains strong, but lack of consumer confidence limits its impact

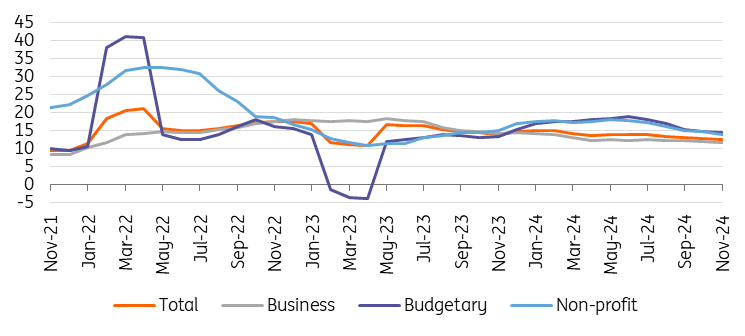

According to the latest data from the Hungarian Central Statistical Office (HCSO), the pace of wage growth slowed further in November 2024 as expected. Average gross wages rose by 11.9% year-on-year. While this was below market consensus, the data does not paint a bad picture. Indeed, today's data point is in line with the longer-term trend of a slow but steady moderation in the pace of wage growth since the beginning of the year. November's wage growth has been the lowest in 2024, and the first time since 2021 that we have seen a rate below 12%. Nevertheless, average wage growth in the first 11 months of last year was 13.5%, well above expectations.

Wage dynamics (3-month moving average, % YoY)

Looking at the November data in more detail, the slowdown in average wage growth is not sector specific. In fact, the pace of growth slowed in all three main areas. Moreover, in November all sectors recorded their lowest level of dynamism in recent years.

In the case of agriculture, the change in wage growth could be due to the completion of seasonal work. The slowdown in the energy sector was also more pronounced. By contrast, the slowdown in industry, construction and market services was not necessarily strong. In the public sector, average wage growth was still very high at almost 14%. This was due to the continuing impact of wage settlements in various areas.

Nominal and real wage growth (% YoY)

Regular earnings have grown at the same rate as the average wage itself, which means that the slowdown in the pace of wage outflows is not due to the development of bonuses, but can be seen as an underlying process. The growth rate of real earnings is around 8%, which is still quite high. However, the positive effects of this are not yet being felt in the economy, given the high propensity of households to save and the fact that caution remains strong. In addition, the current negative trend in consumer confidence may further limit the transmission of positive real wage developments into economic growth.

Looking ahead to this year, the key question is whether we will see a repeat of what we saw in 2024. In other words, despite companies' desire for lower wage increases, the final agreement was closer to what workers wanted. According to a recent Randstad survey, 88% of companies are considering a maximum wage increase of 10% in 2025. In contrast, 86% of workers said they wanted wage increases above 11% (and to be more specific, 45% of workers want an increase above 20%). So the gap between employers and employees is significant once again. However, given the softness in labour demand and the generally weak economic environment at the end of last year and the beginning of 2025, we expect employers' will to prevail this year.

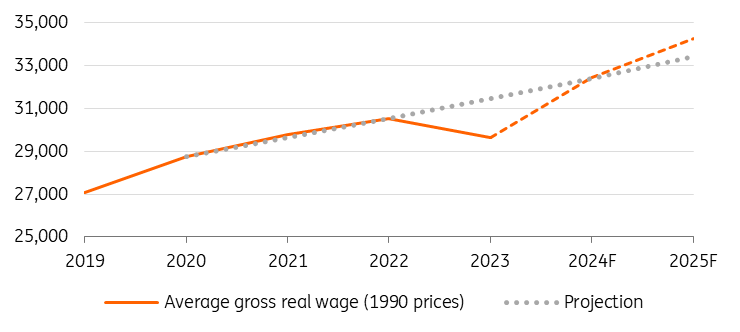

The level of average gross real wage (1990 CPI adjusted HUF)

This means that we see average wages rising by around 10% this year. Besides this, we expect average inflation to be between 4.2% and 4.4% in 2025, which means that real wage growth could be 5.5% for the year as a whole. While this is still almost double the historical average, it is nowhere near as strong as it was last year. A more important question, therefore, is whether or not the accumulated savings will show up in the real economy in the form of consumption. Consumer confidence will be the key to this, and positive real wage growth alone is not enough to encourage spending.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article