Hungarian GDP falls in the third quarter, confirming the deteriorating outlook

- 1 December 2022

- Hungary

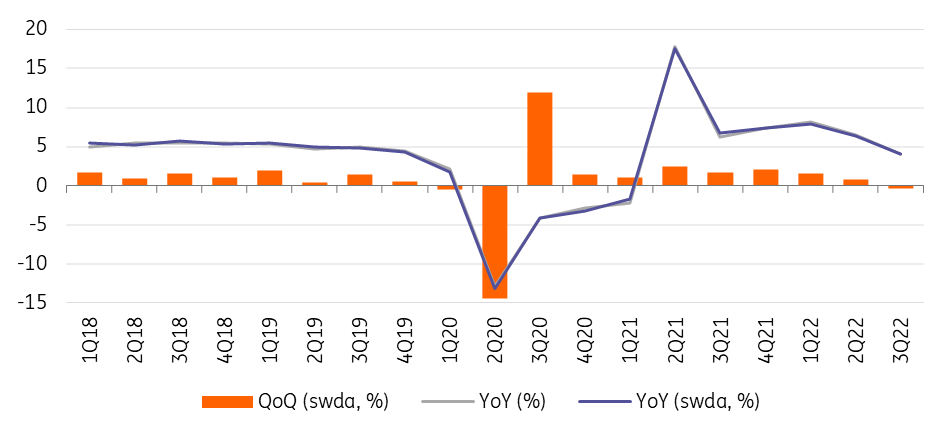

The Statistical Office has confirmed a 0.4% quarterly drop in Hungarian GDP in the third quarter. Knowing what is driving the economic downturn has bolstered our view about the incoming technical recession

| -0.4% |

GDP growth (QoQ, swda)3Q22 |

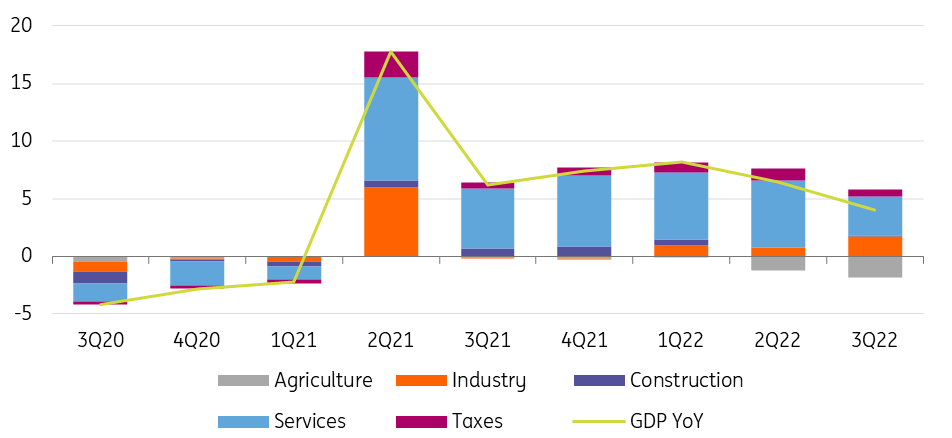

Hungary’s real GDP drops on agriculture and services

When the Hungarian Central Statistical Office released its estimate of the country’s third-quarter performance on 15 November, it was worse than the market consensus. Looking at the actual data today, it is clear to see why there has been a decline.

Hungary's real GDP growth

Let’s start with the production side, where we find the main culprit of the downturn: agriculture. After the extremely negative performance in the second quarter (-32.4% quarter-on-quarter) the volume of value-added in agriculture shrank in the third quarter as well by around 5% on a quarterly basis.

It is also a major blow to economic activity that the volume of value-added in the services sector decreased on a quarterly basis in the third quarter. This is the first time since the height of the Covid-19 pandemic that there has been such a drop. The 0.7% quarter-on-quarter fall is a good indication that the combination of rising inflation, which is crippling the purchasing power of households, and supply-side price shocks for service providers has already started to reduce interest in services. This will only get worst in the fourth quarter.

The stagnation of the construction industry on a quarterly basis was a minor positive based on the monthly output of the sector. But in general, this didn't create a significant contribution to the yearly GDP growth. In contrast with construction, industry delivered a good performance, being the silver lining in economic activity in the period of July-September.

Contributions to GDP growth – production side (% YoY)

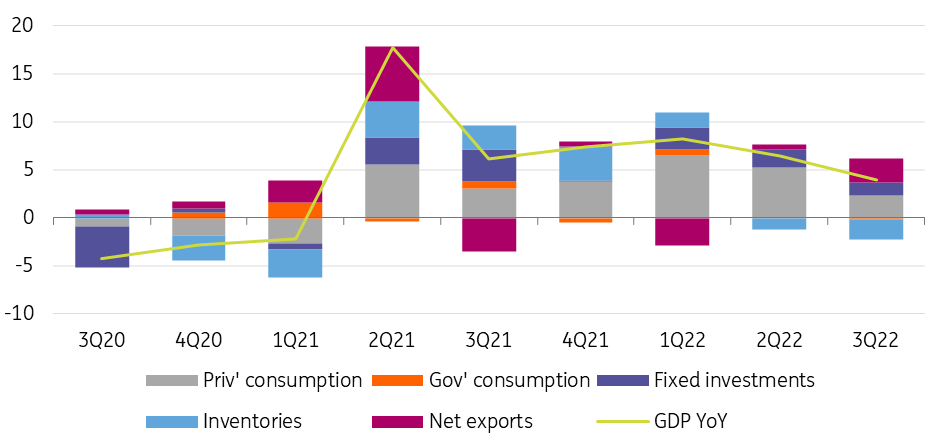

Looking at the expenditure side of GDP, the consumption of households shrank by 0.1% on a quarterly basis in 3Q22. Except for the two Covid-19 lockdown periods, the last time such a drop in consumption took place was in 2012-13. That was the last time Hungary went through a technical recession. Another sign that a technical recession is coming is that the negative real wage shock is likely to fully hit consumption in the fourth quarter.

Investment performance has also weakened, and although expansion is still visible on a quarterly basis, the 0.6% increase indicates that positive momentum is fading here as well. This is due to the uncertain economic outlook, the rising interest rate environment, and the depleted options of subsidised lending.

Unsurprisingly, the contraction of the economy on a quarterly basis and the slowdown of growth on an annual basis in the third quarter were caused by the reduction in domestic demand. The good performance of industry, on the other hand, significantly helped net exports. That explains why 2.5 percentage points of the 4% year-on-year growth comes from net exports, while 1.5 percentage points came from domestic drivers. The last time net exports were a bigger contributor to GDP growth than domestic demand was around 2015-16 (not including the Covid-19 bottom and recovery period). At that time, the economy went through a significant slowdown.

Contributions to GDP growth – expenditure side (% YoY)

The looming technical recession will be evident in the 2023 GDP figure

The detailed data, therefore, confirms our view that the domestic developments will translate into a technical recession in Hungary, as we see a continued drop in real GDP on a quarterly basis in the fourth quarter. At the same time, the combination of the good first half of the year, and the bad second half – which was marked by a technical recession – will keep the average GDP growth around 4.8% in 2022. As for 2023, the picture is much gloomier. This year's expected ugly end creates a negative carry-over effect for next year, and Hungary is probably facing another quarter of GDP contraction in the early stages of 2023. Against this backdrop, we expect economic performance to be close to stagnation, perhaps posting a marginal growth of 0.1% year-on-year in 2023 as a whole.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more