The Covid-19 liquidity problem for eurozone businesses

Business funding needs and the ways these are met differ substantially across the eurozone. This further complicates monetary policy measures meant to provide liquidity to the real economy

How are eurozone businesses funding themselves amidst the Covid-19 pandemic? We've got some answers from the European Central Bank. It's just released bond issuance figures for the first three quarters of 2020. And that's also giving us some ideas on how this may develop in the months ahead.

Borrowing for liquidity, instead of for investment

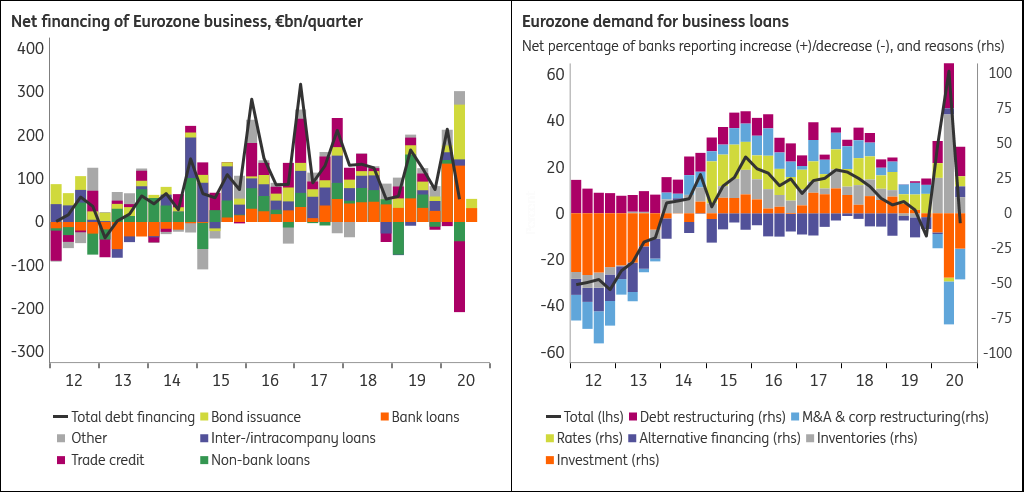

It’s no news that eurozone businesses strongly relied on government liquidity and bank borrowing during the spring lockdown. In addition, bond issuance picked up in the second quarter. But there are more sources and drains of liquidity. For that, we need to turn to the quarterly macroeconomic sector accounts, which are currently available until the second quarter. The chart below shows that in the eurozone as a whole, trade credit (which includes cross-border trade advances but more importantly also domestic supplier credit) dropped substantially in the second quarter. This is simply the result of lower economic activity in the lockdown months, resulting in fewer transactions and turnover. In addition, it may reflect suppliers imposing shorter payment terms on their business clients.

Any 'tax credit' has to be repaid at some point

Once trade credit is taken into account, the increase in business debt in the second quarter looks quite unremarkable. It is important to note however that several governments in Europe allowed businesses to defer their tax payments (e.g. VAT). This amounts to a “tax credit” that will have to be repaid at some point in the future, and hence adds to business debt, but is not counted in the sector accounts depicted below. Moreover, the Bank Lending Survey shows that the second quarter spike in bank loan demand was driven primarily by inventory and working capital needs, as opposed to investment plans or taking advantage of favourable rates, which were the main drivers for demand in the quarters preceding Covid-19.

As liquidity needs subsided in the third quarter, so did demand for bank loans. Meanwhile, investment plans are put on ice, and further contribute to weak bank loan demand. The survey confirms the strongest fall in demand in France and Spain in the third quarter, with demand holding up in e.g. Italy and Germany.

Eurozone business funding mix and demand for bank loans

For the third quarter, we don’t have the full funding picture yet. Bank loans and bond issuance are now in and show a sharp drop to more “normal” amounts. As economic activity recovered in the third quarter, we may expect trade credit to have increased again.

Funding mix differences across countries magnified in crisis times

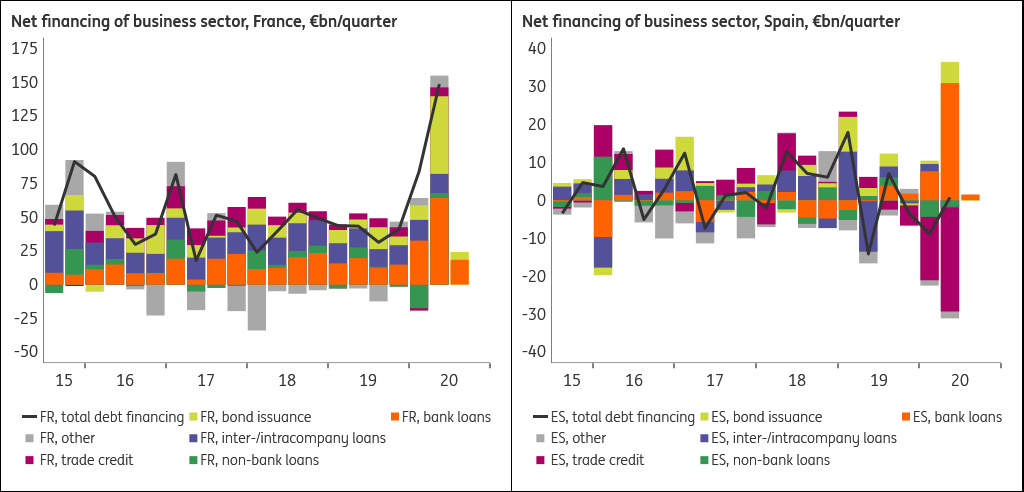

Looking at aggregated eurozone data misleadingly suggests that funding patterns are similar across its member states. Yet business funding shows some sizeable country differences. First, France stands out. In the second quarter, both bank borrowing and bond issuance increased strongly, while there was no trade credit contraction – a stark contrast to the rest of the eurozone, and one we struggle to explain.

All this resulted in additional French business financing surpassing €150bn in the 2nd quarter, triple the “normal” quarterly amount. If it weren’t for France, net eurozone-wide business financing (clocking in at €52bn) would have been negative. And again, this does not include government liquidity support (neither credit nor grants).

Net financing of the business sector in France and Spain, € bn per quarter

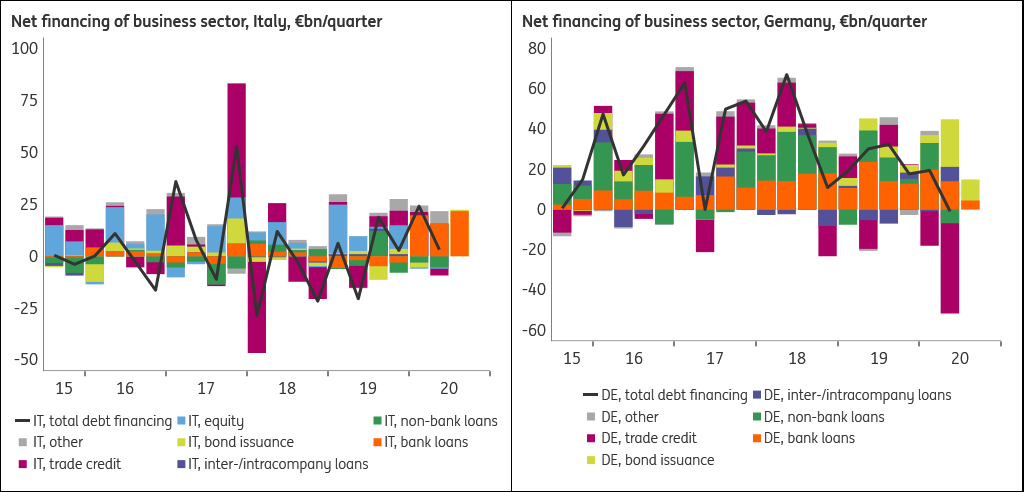

Spanish businesses did see a strong contraction in trade credit, and relied mostly on bank borrowing in the second quarter, with relatively little bond issuance. Net demand for bank loans dropped to zero in the third quarter. Note that Spain experienced a relatively deep recession, with GDP now back to about 90% of pre-Covid-output, compared to about 95% for the other major eurozone countries. Italian businesses, in contrast, faced only a very small trade-credit contraction. Reliance on bank borrowing was strong too, but much more evenly spread in time, with strong demand continuing into September. Net bond issuance was virtually zero throughout 2020.

Net financing of the business sector in Italy and Germany, € bn per quarter

Net financing of German businesses fell to zero in the second quarter, with negative trade-credit balancing out bank borrowing and bond issuance. Demand for bank loans eased in the third quarter, even turning net negative in September. Similar patterns can be observed in the Netherlands and Belgium. Stronger bond issuance by "northern" corporates suggests that they have access to bond markets on better terms than their southern counterparts, a pattern all too familiar in the eurozone. All this makes clear that in crisis times, even more than normal ones, the demand for funding - and the way this demand is met - differ substantially across the eurozone.

This is old news… what about funding in the months ahead?

In a way, the data above provides a glimpse into the distant past, as by now we have moved into a new lockdown phase. Based on the patterns we saw earlier this year, we may expect a new drop in trade and supplier credit, though given that governments try to minimise the economic impact, and businesses have adapted too, that drop will be less severe.

We expect any increase in demand for bank loans and bond issuance to be much more muted than in Spring. Businesses are likely to have been better prepared this time, not least in financial terms. Some businesses may no longer be in a position to run up any more debt. Looking towards 2021, the recessionary environment will continue to weigh on funding demand, while borrowing rates have little room to fall further, as we wrote earlier.

Despite the establishment of a Banking Union and continuing efforts to build a Capital Markets Union, business demand for funding, and the way this demand is met, differs substantially across the Eurozone. This is nothing new, but differences get magnified in crisis circumstances. This complicates the use of eurozone-wide policies, such as monetary policy: their transmission to the real economy will diverge between countries.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article