Taxonomy Disclosures: A slow start, but a start nonetheless

For the first time, banks disclosed their Taxonomy alignment and Green Asset Ratio alongside their Taxonomy eligibility. The GAR average lies just over 3%, far below the expected 10%, while the eligibility rate increased by 5pp since last year to reach 35%. Several factors explain these very low results including data gaps and calculation differences

What you need to know about the latest EU Taxonomy disclosures

For the first time ever, the first quarter of 2024 ends with financial institutions’ EU Taxonomy (EUT) reports including both eligibility and alignment to the Taxonomy. Banks’ annual reports and Pillar III disclosures now include the new and widely discussed Green Asset Ratio (GAR), designed to become a snapshot of banks’ environmental sustainability.

While some expected this first year’s GAR average to be lower than 10%, banks reported, on average, only 3% GAR. However, when looking at the EUT eligibility rate, financial institutions still reported around 35% Taxonomy eligible assets, a 5-percentage point (pp) increase since 2022. These results are derived from our sample of 33 European banks from 13 jurisdictions, and while we note some national variations, results are still strikingly low.

One could stress that these very low results show the overall lack of green activities in the European economy or the financial sector’s inaction against climate change. However, we believe there are other factors at play that influence both the Taxonomy and GAR results. In this piece, we start by looking into variables considered in the EUT and Green Asset Ratio calculations. We also dive into the different methodologies used by banks and their effect on the reported results. The third section summarises this year’s disclosures. Finally, we discuss the three main points that could negatively affect the final results.

What's new this year?

The European Commission introduced its sustainable finance framework back in June 2023. It aims to complete the Union’s sustainable agenda while supporting corporates and financial institutions’ transition to a carbon-neutral and sustainable economy. Part of that action is to reduce implementation costs and enhance the EUT’s usability.

The Taxonomy is a cornerstone of the European Union’s action against climate change, as it defines environmentally sustainable activities. The classification system aims to enhance transparency and comparability of ESG performance metrics.

EU Taxonomy in a nutshell

The European Taxonomy uses six environmental objectives to define sustainable activities:

- Climate change mitigation

- Climate change adaptation

- Sustainable use of water and marine resources

- Transition to circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

The Environmental Delegated Act for the last four points was published only last year. Therefore, the current reporting focuses on the first two criteria.

Taxonomy eligible: Activities identified in the Climate Delegated Act and Environmental Delegated Act as eligible for the purpose of financing the EU Taxonomy six environmental objectives.

Taxonomy aligned: Taxonomy-eligible activities that fully comply with the EU Taxonomy’s technical screening criteria for substantial contribution, do no significant harm and have the minimum safeguards.

Large corporates, financial institutions and insurers must report under the Taxonomy annually. For the first time this year, banks were required to report both eligibility and alignment ratios. Corporates covered by the Non-Financial Reporting Directive (NFRD) already did so last year.

Enforced in 2014, the NFRD aims to improve social and environmental information transparency. Large, listed companies but also banks and insurance companies with more than 500 employees are falling under the NFRD scope and are therefore required to publish annual reports on their sustainable policies. This directive only covers the largest European financial and non-financial entities. However, the number of included corporates will significantly increase with the enforcement of another directive, the Corporate Sustainability Reporting Directive (CSRD).

The CSRD completes the current NFRD by gradually increasing its scope to incorporate smaller entities and third-country corporates. Entities gradually falling under the CSRD scope will automatically also have to disclose their eligibility and alignment ratio under the European Taxonomy.

The EU Taxonomy should be fully implemented in 2029

The Green Asset Ratio

While the two previous policies are focused on corporates, yet another indicator was developed specifically aimed at banks, the Green Asset Ratio (GAR). This seeks to give a glance at financial institutions’ sustainability and is enforced for the first time this year. Banks reported in 2024, for the first time, both their GAR asset stock and some also added their GAR for their investment flow.

The GAR measures the share of the credit institution’s Taxonomy-aligned balance sheet exposures over the total eligible exposures. This gives a short and comparable overview of the credit institution’s alignment with the Taxonomy.

GAR equation

Exposure to central governments, central banks and supranational issuers are excluded from the calculation. While exposure to undertakings not (yet) falling under the NFRD (or CSRD) are excluded from the numerator of the GAR but included in the denominator. We’ll get back to the calculation and effect on the results in the last part of this piece.

The methodology to derive Taxonomy-aligned assets in a bank's portfolio involves three steps

To summarise this overflow of European regulation, this year’s disclosures matter as it’s the first time banks share their EUT alignment and Green Asset Ratio. Thus, they give a feel for the ratio that could become the main sustainable indicator for financial institutions.

First GAR disclosures are disapointingly but not surprisingly low

Banks’ two previous Taxonomy-eligibility disclosures revealed major methodology discrepancies. These stemmed from different calculations used by corporates on which banks rely for their own Taxonomy-eligibility reporting. Indeed, corporates can calculate their sustainability ratio over three variables: their turnover, capital expenditure (CapEx) or operational expenditure (OpEx).

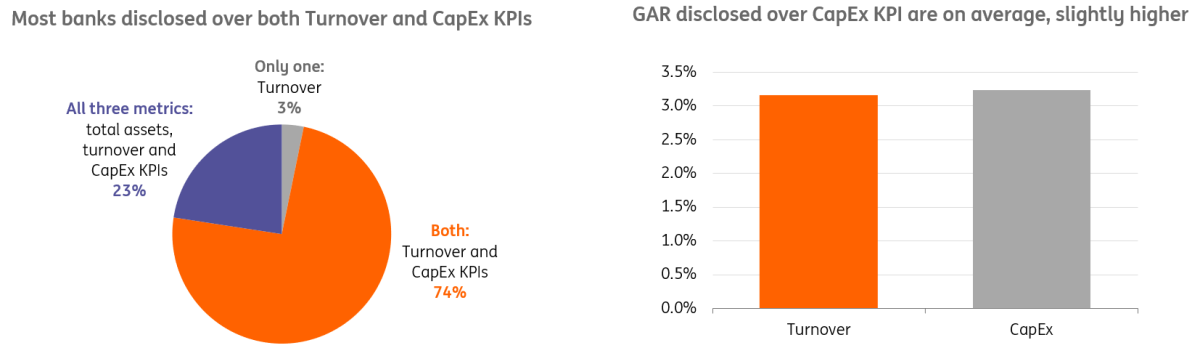

As a consequence, banks disclosed their eligibility ratio using different methodologies. In short, they disclosed a share of green activities with three separate KPIs: either their total assets, turnover or CapEx. With time, we have seen financial institutions’ disclosures shift to focus mainly on turnover and CapEx ratios. Thankfully, as this year marks the third anniversary of Taxonomy disclosures, we also note more consistency in banks’ reporting. Most of our 33 European bank samples made use of a uniform template, allowing for a better cross-institution and country comparison.

Before having a look at the results, it’s important to explore the consequences of these calculation differences. While most banks disclosed two ratios, one using the turnover KPI and the other the CapEx KPI, we also see a decent share of institutions reporting on their GAR over total assets. On average, the Green Asset Ratio over CapEx is slightly higher than the one over turnover, but the difference is minimal.

Banks disclosed their GAR using different methodologies

As discussed in our previous publication, we expected a drop of about 20pp between eligibility and alignment results. Based on our sample, this drop was even worse. The average eligibility rate lies at 35%, 5pp ahead of last year. However, while some estimated this year’s average GAR to be below 10%, in reality, the average reaches just over 3%.

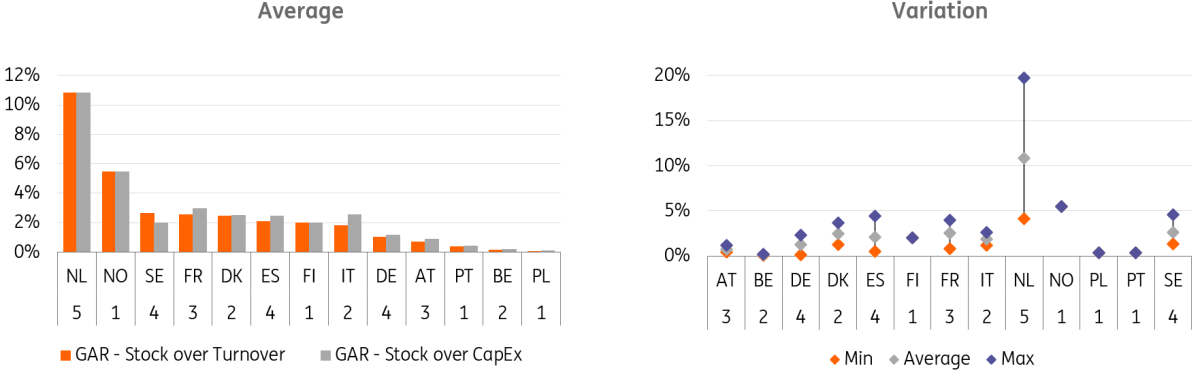

Whilst 3% of banks’ eligible assets qualifying as green is very low, we believe it’s not worth raising the alarm yet. The first reason to keep calm is the large variation between disclosed results. Indeed, our sample includes 33 banks from 13 jurisdictions and within that selection, we see significant gaps in disclosed GAR both between banks and countries. The graph below illustrates the national average GAR, which clearly shows major differences.

Dutch financial institutions disclosed, on average, the highest share of green assets with results reaching nearly 11% on average. Belgian banks are last with an average below 1% (0.14%). Zooming in on variations between banks from the same jurisdiction, the graph below also highlights important differences. Once again, the Netherlands is the outlier with a 15pp gap between the highest and lowest GAR. Overall, national variation is around 5pp. In the next section, we dive into the different reasons for these variations and how to interpret these results.

Green Asset Ratio averaged per country

While the GAR is an interesting metric to look at, the Taxonomy eligibility and alignment ratios give insights into the share of a bank's portfolio that could become green by improving eligible assets into aligned assets. Over 2021 and 2022, the eligibility rate stabilised around 30% of banks’ total assets. Last year’s results slightly improved as the 2023 average lies at 35%.

On average, we see a reduction of 30pp between the national average for eligibility versus alignment with the Taxonomy. However, a higher eligibility rate doesn’t imply a higher alignment rate as countries like Norway, Sweden and Finland (with some of the highest eligibility) show a drop of over 40pp between their Taxonomy eligibility and alignment. This can suggest that domestic banks were very cautious in calculating their green assets and left out significant parts of their books. Thus lowering their EUT alignment and, ultimately, their GAR. Dutch banks were the outliers with the highest alignment ratio despite showing around a 45% eligibility rate.

Averaged national correlation between EUT eligibility rate and alignment rate

One last interesting metric to look at is the share of non-financial counterparties not subject to the NFRD. This ratio shows the share of corporates not yet subject to the European Taxonomy disclosures in the bank’s book. It’s an interesting metric to keep an eye on as the EUT scope will be gradually increased through the CSRD. This implies that SMEs and third-country companies’ activities will ultimately be included in the ratio.

In other words, a high share of non-financial counterparties not subject to the NFRD can be interpreted as potentially higher eligibility and alignment rates in the future strictly resulting from a calculation change. The graph below points out the largest average share is for Spanish and German banks, followed by Belgian ones.

National variation in share of non-financial counterparties not subject to the NFRD

Results to take with a pinch of salt

In summary, from our sample the average green asset ratio (over Turnover) for the year 2023 equals 3.1%. The Netherlands and Sweden are leading with average GARs at 11% and 5.5% respectively. We also still note important disclosure variations between banks within the same jurisdiction. Additionally, results point to a stagnation of the EUT eligibility rate at 35%, only a slight 5pp increase compared to 2022.

Financial institutions, as well as the corporates they rely on, are still in the implementation-learning phase as this year was banks’ first ever GAR disclosures. We believe this exercise is going in the right direction as this year’s disclosures were showing much less methodology discrepancies than previously. This adds to the improved accessibility of banks’ disclosures as they are now included in their annual and Pillar III reports.

Despite these improvements, the reality remains that the average GAR doesn’t even reach 3% of banks’ eligible assets. Nonetheless, we would like to remain hopeful and stress the importance to take those results with a pinch of salt. This section unfolds three reasons why one should remain cautious when looking at Taxonomy and GAR results.

Large data gaps

The EU Taxonomy is an extensive piece of regulation requiring corporates to collect substantial information on their activities. This can be a challenge to put in place. Besides the struggle to gather the necessary data, not all corporates have the data storage or methodology in place to process the information and share it with both regulators and banks.

Banks struggle to gather the necessary data from their clients, which adds to data gaps. For instance, banks must collect Energy Performance Certificates (EPC) for their building portfolio. However, in many countries, only a small share of the building stock holds an EPC. In countries like Belgium, a remote amount of real estate has an EPC. Therefore, financial institutions are not able to gather and include those assets in their disclosures.

This will most probably evolve over the next few years as the Energy Performance of Buildings Directive (EPBD) will standardise the use of EPCs and such certificates will become more commonplace. Read more on this Directive in our other publication here.

Additionally, the European Union is currently developing the EU single access point. This platform will centralise all corporate sustainable disclosures and will allow banks to retrieve the necessary data for their own reporting.

Banks are still in a learning phase

The second point to consider when looking at these reports is the “application uncertainty”. Indeed, as this year was the first year of the EU Taxonomy alignment and GAR reporting, banks often had widely different approaches to selecting their green assets.

This is partly due to gaps in the regulation but also stems from inconsistent enforcement from auditors. Indeed, banks’ sustainable reporting must be audited by an external party each of which appears to take a somewhat different direction.

The most significant variation concerns the treatment of the mortgage portfolio. The first reason for that is the EPC classification of buildings, which differs significantly across Europe (both in terms of scaling and methodology). Countries with a more lenient EPC classification system (like the Netherlands) accounted for nearly all their taxonomy-eligible buildings, increasing their GAR.

As discussed previously, in cases where countries hold only a very small share of EPC labels relative to the building stock, banks must exclude a large part of their portfolio from the calculation, which lowers their alignment ratio and GAR.

Alongside this challenge, sometimes, bank assets must comply with very difficult and technical Do No Significant Harm (DNSH) criteria to be considered as Taxonomy aligned. This is the case for certain electric vehicle criteria, making it virtually impossible for banks to comply with.

Finally, some banks simply opted for a conservative approach to reporting, most probably to avoid greenwashing accusations as public scrutiny is at an all-time high. This translated into a large difference between the share of eligible and aligned assets and consequently a very low GAR.

Imperfect methodology

Last but not least, one should be cautious when interpreting these results as the formula by which they are derived is not giving a full view of banks’ assets and sustainability. There are three reasons for that:

- The Taxonomy scope currently only includes corporates large enough to fall under the NFRD, insurers and financial institutions. Therefore, SMEs and third-country companies are simply not required to disclose their sustainable activities. Ultimately, banks with a large share of their books dedicated to these entities will report a lower alignment rate and GAR, regardless of how green their activities truly are. This will be tackled by the new CSRD regulation discussed earlier in this piece but several years will be necessary before its full implementation.

- SMEs and non-EU companies’ exclusion has a specific impact on the GAR as it creates an asymmetry in the ratio. These entities are accounted for and included in the denominator of the equation but excluded in the nominator. From this strictly mathematical effect, the GAR is artificially brought down. The degree of this effect depends on the bank and the share of its portfolio allocated to SMEs and third-country companies. However, we can affirm that it has and will have a negative impact on banks' disclosed Green Asset Ratio until these entities are included in the scope of the Taxonomy.

- The last point we’ll address here concerns project finance. Financial institutions often finance large projects, including sustainable ones such as wind or solar panel farms, through special-purpose vehicles (SPVs). By doing so, the financed assets may not technically end up on the bank’s balance sheet and, therefore, are neither included in the Taxonomy nor GAR. Furthermore, while the gradual implementation of the CSRD should mitigate the two previous points, the size of such SPVs will still be too small to fall under the CSRD. Therefore, there is no prospect in the European legislation to include such investments in the mapping of sustainable assets yet. Once again, the impact of the exclusion varies depending on banks’ balance sheet composition.

Despite showing that the European economy is, in fact, not that green, we should keep in mind these three points when discussing and assessing this year’s bank disclosures.

A sinuous start to a long regulatory road

The Taxonomy’s ultimate objective is to develop a financial system and economy as a whole, rewarding sustainable activities and supporting every sector to transition to more sustainability. This year’s disclosures are a great improvement as they allow some degree of cross-bank and country comparison. This comes from banks’ use of a common template and the inclusion of the disclosure in their publicly accessible sustainable or annual reports.

Nonetheless, the road ahead is still long before either the EUT or GAR allows us to truly assess how green the European economy is. To become a more meaningful measure of sustainability, the EU will have to address several challenges. First comes the data accessibility to ensure an unbiased picture of the economy. Second is the enforcement of the CSRD and consequent increase in EUT scope. And finally, the improvement of the current calculation ensures all green activities can be included and disclosed.

To conclude, both the alignment ratio and the GAR are showing disappointingly low results this year. The first argument that comes to mind is that the European economy is simply not that green, and much more effort must be put into the transition. However, rather than panic, we’d like to remain positive as these were banks’ first-ever green asset disclosures. It is thus natural to see some room for improvement. Furthermore, the EU is setting global standards in sustainable disclosures and that should be celebrated as a step in the right direction.

One should also remain hopeful as the current ratios don’t represent the whole economy and will change significantly over the next five years.

Last but not least, these are indicative ratios, and despite giving a good idea of how far EU banks still must go to become green, it’s difficult to summarise banks’ green activity to a single two-digit ratio. It’s, therefore, always advisable to dig deeper. That being said, one can hope that these low results will work as a wake-up call for the economy and financial institutions to further invest in sustainable activities.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article