Oil prices to remain well supported

The oil market saw significant strength over the third quarter, with the market set to remain in a deep deficit until the end of the year. This tightness suggests we could see more upside, but we believe any move above $100/bbl will be short-lived

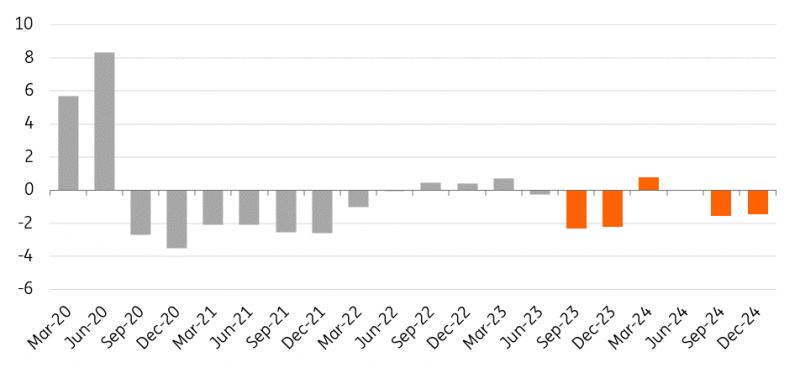

Deep deficit for the remainder of the year

ICE Brent has had its best quarterly performance since the first quarter of 2022, up more than 31% over the third quarter of this year. This is on the back of a deficit environment, which is expected to remain until the end of this year. Following Saudi Arabia and Russia extending voluntary supply cuts through year-end, our balance shows that the oil market will see a deficit of more than 2MMbbls/d in the final quarter of 2023.

A tight market for the rest of the year suggests that prices should remain well-supported for the remainder of 2023. Our forecast for Brent remains unchanged and we expect it to average US$92/bbl over the fourth quarter of the year.

We do expect some of this tightness to ease in in the early part of next year, with the market returning to a small surplus over the first quarter of 2024. This is driven by Saudi Arabia’s voluntary additional cuts coming to an end, along with the seasonally weaker demand that we usually see over the first quarter. The looser balance early next year suggests we could see a pullback in prices towards the end of 2023 and moving into 2024. However, we believe any pullback will be relatively short-lived as the market starts to tighten once again from the second quarter, and with growing deficits over the second half of next year. Our 2024 Brent forecast remains unchanged at US$90/bbl.

Global oil balance remains tight (MMbbls/d)

$100 oil likely not sustainable

In addition, OPEC+ will likely come under increased political pressure to bring more supply back into the market if prices move much higher. There are elections in two key oil-consuming nations next year – the US and India – and these governments will likely want to minimise any potential inflationary pressures. However, there is no guarantee that OPEC+ or the Saudis will listen to any calls to increase supply. It will become increasingly difficult for OPEC+ to state that they aim for stability in markets when there is a large deficit, prices are moving towards $100/bbl, and the group is holding a sizeable amount of supply from the market.

OPEC+ has a strong grip on the market

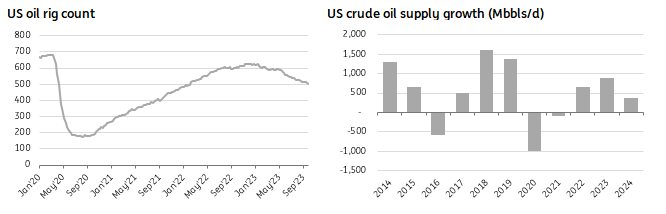

It has become very apparent that OPEC+ has full control over the oil market. It has taken a while, but the group has managed to push prices higher. Limited non-OPEC+ supply growth – specifically from the US – has given OPEC+ the confidence to cut supply and push prices higher without the risk of losing a significant amount of market share.

In order for OPEC+’s grip to loosen, we would likely have to see a resurgence in US oil supply growth. This is unlikely to be anytime soon, with US drilling activity having slowed significantly this year. The number of active oil rigs has fallen by 119 so far this year to 502, the lowest level since February last year. While US crude supply is set to hit record levels in 2024, the growth rates are expected to be very modest. If oil prices remain elevated, there is always the potential that US industry will start to relax the capital discipline it has shown in recent years – which would eventually translate into increased activity. However, up until now, we've seen few signs of this.

Modest US supply growth gives OPEC+ growing control of the market

Download

Download article

5 October 2023

ING Monthly: An inconvenient truth for central banks This bundle contains 14 ArticlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more