Healthcare providers face challenges on path to net zero

If the global healthcare sector were a country, it would be the fifth largest emitter of greenhouse gases. Emissions have to come down over the coming years, as the world moves to net zero. In this process, the modernisation of care and healthcare facilities, the procurement of renewable energy, and value chain collaboration are vital

The healthcare sector emits more greenhouse gases than you might think

The global healthcare sector, which includes all processes that facilitate cure and care (e.g. direct care, but also pharmaceutical production, and biotech) emits roughly 5% of all greenhouse gas emissions globally. For developed countries, this percentage is higher still: between 7% and 8%. The healthcare sector in the United States, for instance, emits 8.5% of the country’s greenhouse gases while the French and the Dutch healthcare sectors emit 8% and 7%, respectively.

In the Netherlands, a little over 40% of greenhouse gases emitted by the healthcare sector are attributable to the pharmaceutical industry. These emissions mainly take place during the manufacturing process. Almost a third of emissions stem from diverse sources (named miscellaneous below) such as transport and the production of medical devices for instance. Roughly a quarter of all emissions are tied directly to healthcare providers through the food and catering they provide, electricity and heating they use and the direct impact of care. This means that healthcare providers worldwide are responsible for a little over one percent of all greenhouse gas emissions. This article takes a closer look at these emissions.

Breakdown of greenhouse gas emissions of the Dutch healthcare sector

The healthcare sector has committed itself to being net zero in 2050

As the world, under the Paris agreement, has committed itself to climate neutrality in 2050, healthcare providers and the healthcare sector at large are ramping up their climate efforts. For the European and American healthcare sectors, the European Green Deal and the Inflation Reduction Act (IRA) are particularly important. The European Green Deal dictates that healthcare providers must reduce their Scope 1 and 2 emissions to 55% in 2030, while the IRA mandates that companies reach a 50% reduction in the same year. Both regulatory packages have set 2050 as the deadline for climate neutrality.

How the healthcare sector reaches these targets differs by country as the nationally determined contributions (NDCs), agreed on in Paris, vary. In the Netherlands, for instance, the healthcare sector as a whole should achieve a 30% reduction in carbon emissions by the end of 2026 and 55% in 2030. The plans for 2050 are, as yet, not clear enough to say whether the sector will achieve these goals. However, the Dutch healthcare sector as a whole has a good chance of meeting its goal for 2030.

In the US private companies are leading the way. The two largest private hospital and health systems (Ascension and CommonSpirit Health) are on track to halve their carbon emissions in 2030. Important pharmaceutical companies such as Pfizer and AstraZeneca have also committed to being net zero in 2050.

In general, though, stark differences between countries persist. As we will see in the remainder of this article it matters how energy grids are powered, which requirements governments put in place for the sustainability reporting of healthcare providers, and whether procurement is done for each hospital individually or whether it is a joint effort.

Pathway to reducing Scope 1 and 2 emissions is clear, Scope 3 less so

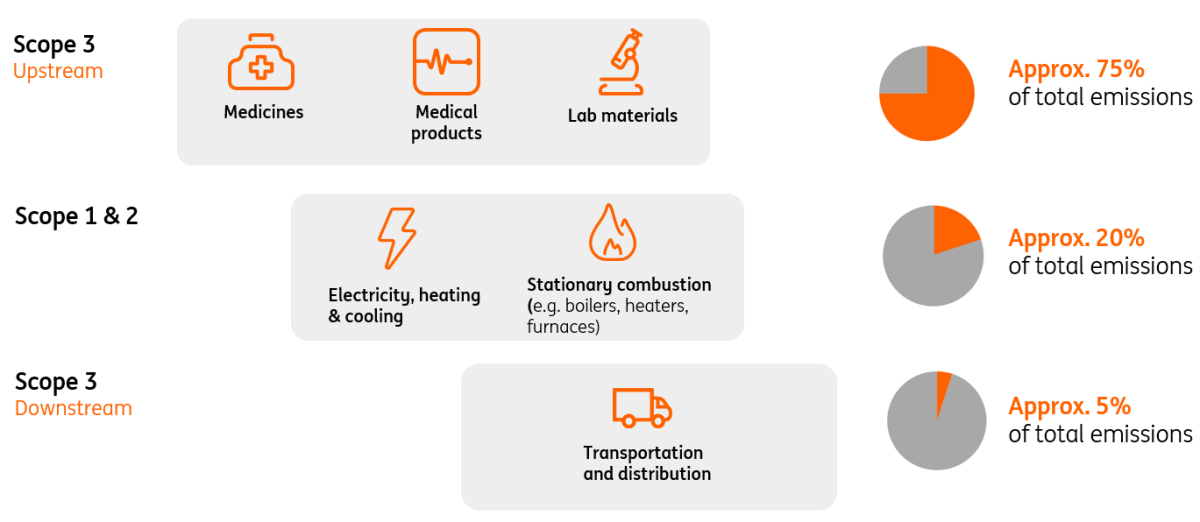

Healthcare providers face two distinct challenges in achieving climate neutrality. Firstly, they need to reduce their Scope 1 and 2 emissions, which are direct emissions (like gas-based heating) and emissions from purchased energy, but they also need to look beyond their own operations; as around 80% of the greenhouse gas emissions from healthcare providers happen either upstream or downstream in their value chain (Scope 3). Upstream emissions, for example from the production of medicines, medical devices and lab materials, are the most important factor as they cause around 70% of all emissions.

Most emissions of healthcare providers arise at the beginning of the value chain

Schematic breakdown of emissions from the perspective of a healthcare provider

Currently, the majority of healthcare providers has a plan in place to reduce Scope 1 and 2 emissions. The primary focus areas here are the purchasing/generation of renewable energy and the sustainability of real estate, but circularity, waste reduction, and the carbon footprint of food services are also important focus areas.

In contrast, not every healthcare provider has formulated a target for their Scope 3 emissions. Naturally, Scope 3 emissions are harder to bring down because of dependencies on third parties. Engagement with suppliers and setting requirements are therefore very important steps healthcare providers can take. Large healthcare providers can play a leading role in this process by setting requirements in contracts for suppliers. The British NHS is one of these organisations. Since April 2023, it mandates that every one of its suppliers (for contract values exceeding five million pounds) has a detailed carbon reduction plan in place.

Healthcare providers are well underway with their reduction of Scope 1 and 2 emissions

Healthcare providers in many countries are well underway with reducing their Scope 1 and 2 emissions. They are doing this through three primary ways: the procurement of renewable energy, the energy-efficient refurbishment of buildings, and the reduction of their energy consumption.

Increased procurement of renewable energy

This includes the installation of solar panels on rooftops but also pertains to the purchasing of renewable energy. The difficulty of purchasing renewable energy differs greatly per country. Australia’s power grid, for instance, is mostly powered by black coal. This means, aside from installing solar panels, greening energy needs are currently more difficult for Australian healthcare providers than those in countries with a large renewable energy supply, like Norway, for instance.

Energy-efficient refurbishment of buildings

Through modern construction techniques, insulation and other energy efficiency measures a lot of energy can be saved. However, not all buildings can be refurbished before 2050. Hospital buildings have an average lifespan of around 40 years. For hospitals and other in-house care providers like nursing or care homes that are not yet due for replacement before 2050, the challenges to get to an energy-efficient building can be particularly sizeable.

Reducing electricity consumption

Simple ways this can be done are through turning off air treatment when an operating theatre is not in use, or switching off medical devices that are not in use. This is forgotten, more often than you would think: a recent study by Philips and Vanderbilt on the energy use of diagnostic imaging devices, found that 44% to 75% of energy is consumed outside of patient scanning time.

Over the past years, energy consumption as a percentage of total costs for Dutch hospitals has remained remarkably stable at 2% every year, which suggests that energy use could be reduced through the training of personnel. Yet, energy costs are a small percentage of total costs, for comparison: personnel costs make up 50% of total costs on average, which reduces the incentive to offer elaborate training on these matters.

Another complication is that nurses make up the bulk of hospital staff, and they, generally speaking, cannot control the lights and switches on their wards. As hospitals run 24/7 this means that intelligent building controls and temperature settings when operating theatres are not running probably have more priority.

Energy costs of hospitals have remained very stable over the past years

Energy and labour costs as percentage of total costs of Dutch healthcare providers

Move to more compact hospitals underway

Making real estate more sustainable is all about reducing energy requirements per square metre of floor space and thus minimising the amount of space to be heated and cooled. Industry consolidation is expediting this process as the creation of larger groups and partnerships causes concentration in one place, thus requiring fewer square metres. Each metre less reduces the energy demand for heating, cooling and humidifying air. This concentration is also driven by the fact that smaller regional hospitals with real estate that is far from ready for replacement, will have trouble meeting climate goals. Hospitals with a building from before the early 2010s when the design did not take into account the replacement of installations and building parts with a shorter life cycle, such as operating theatres and intensive care units, face the greatest sustainability challenges.

More recently built or renovated hospitals often also incorporate modularity in their designs, which means that the purpose of parts of a hospital can easily be changed. This gives hospitals the opportunity to carry out the same amount of procedures, but with less floor space which benefits sustainability.

Another trend driving the move to more compact hospitals is the rise of telemedicine. Telemedicine reduces the need for patient and provider travel, which increases sustainability. Future Healthcare Journal found that telemedicine reduces the carbon footprint between 0.70–3.72 kg CO2 equivalent per consultation, which means telemedicine has enormous potential in bringing down the emissions of the healthcare sector, particularly because 60% of hospital care need not take place in the hospital (Corrigan & Mitchell, 2011). The Covid-19 pandemic accelerated the adoption of telemedicine, however shifting to more telemedicine would require major structural changes to the financial flows of healthcare systems as healthcare providers would need to be compensated for telemedicine. In addition to the investments in telemedicine, there are legacy costs of existing, but underused, real estate. Yet, healthcare providers would do well to invest in telemedicine now.

Three trends that drive move to more compact hospitals

In terms of the compactness of hospitals, stark differences between countries are present currently. Bulgaria has nearly 700 hospital beds per 100,000 inhabitants, while the Netherlands has a little over 200 beds per 100,000 inhabitants. In short, the move towards more sustainable and compact care facilities is more challenging in Eastern European countries than in other European nations, as they tend to have a less concentrated hospital sector. However, this also means that there is more potential to cut CO2 emissions in these countries. They can profit from existing telemedicine technologies and make larger steps in a shorter time span.

Number of curative care beds per 100,000 inhabitants

Value chain collaboration is an opportunity to reduce Scope 3 emissions, but process remains difficult

It is harder to bring down Scope 3 emissions than Scope 1 and 2 because of dependencies on third parties. However, healthcare providers can engage with suppliers in a meaningful way to ensure they are also on their way to climate neutrality in 2050. As mentioned at the start of this article, large healthcare providers can put stringent requirements in place in terms of the carbon reduction of their suppliers. Again, between-country differences are important here. For the NHS, this is easier to do than for countries in which private health insurers have to make this a condition in domestic healthcare procurement. It then remains to be seen whether individual parties can enforce this on their suppliers. In any case, a joint procurement policy is important if healthcare providers want to make sustainability demands on their suppliers.

For smaller healthcare providers and those that have not yet started mapping out their Scope 3 emissions, applying an 80-20 strategy is a good way to start. By creating an overview of their largest suppliers, healthcare providers can get a clear picture of where their Scope 3 emissions primarily take place. In doing so, they can monitor the science-based targets of their suppliers, and encourage responsible sourcing policy. Through the exchange of information and collaboratively building good datasets, emissions per purchased device or medicine could for instance be calculated by applying existing methods for life-cycle-analysis.

Benefits of the 80-20 Strategy

A good example of this is engagement with drug suppliers: healthcare providers could ask for data on raw material use, energy consumption, water consumption, transport distances and waste from drug production. This way suppliers could be nudged to more sustainable methods of production, agreements on reduction goals could be made and it gives healthcare providers detailed information to measure their Scope 3 emissions.

Nudging Sustainable Production

Collaboration with medical technology companies also promising

Another avenue healthcare providers can pursue is collaborating with medical technology companies. Newer models of radiological equipment, which are heavy energy users, tend to be much more energy-efficient and can be recycled by their suppliers. In addition, many newer designs incorporate modularity, which means that when a machine breaks down the entire machine does not have to go but only one part has to be replaced.

When healthcare providers can ill afford to switch to newer models, a collaboration with medical technology companies is promising. Whereas a few years ago, payments for equipment would have to be carried out in full and upfront, currently many medical technology companies offer their machines as a subscription. Monitoring as a service, for instance, means healthcare providers face less capital expenditure, but can still shift towards more energy-efficient and modular machines.

No targets for circularity in place, yet these are important going forward

In contrast to the clear targets for greenhouse gas emissions, there are no such targets for circularity and other sustainable practices of hospitals. Therefore, this is an area where the sector can make a tremendous difference without regulation forcing its hand. Naturally, with the single use of sterile gloves and other plastic equipment, surgical procedures are responsible for an enormous amount of waste.

To get an insight into this process, healthcare providers could consider introducing disaggregated carbon footprint results. This would allow decision makers to differentiate the contribution per product group and department and would give insights on which products should be used where and how.

In addition, by reducing the amount of materials and medicines that are discarded (e.g. by prescribing the exact amount of pills to patients), the need to purchase new ones can be lowered. This not only decreases the carbon footprint and emissions associated with waste treatment but also lessens the environmental impact of producing these materials. However, this requires a behaviour change that needs to be effectively managed. Doctors order the materials that they require, shifting to new supplies therefore requires education and time for adoption.

Medicines prescribed and gases used during procedures also have a big climate impact

Another sustainability aspect few people are aware of is that the same medicines can have very different climate impacts. The way paracetamol is administered, for example, has a widely varying environmental impact: intravenous has the largest impact but is most commonly used in hospitals. Thinking whether intravenous administration is necessary could have a major impact on CO2 emissions.

Carbon footprint of different types of paracetamol

The same goes for anaesthetic gases. Complete anaesthesia during surgery emits twice the CO2 of partial anaesthesia, and replacement by injections decreases greenhouse gas emissions even more. Again, this requires a behaviour change of doctors, who are key in this regard.

In addition, these might seem like small changes, but the hospital sector is so big, that little things add up to a huge amount of waste and CO2 reduction. In short, incremental changes can make a big macro impact.

Conclusion

Healthcare providers are on their way to bringing down their Scope 1 and 2 emissions, however, stark differences between countries remain. The modernisation of care through telemedicine and the energy-efficient refurbishment of healthcare facilities are important in this regard, as is the procurement of renewable energy. However, significant investment in the measurement of Scope 3 emissions and value chain collaboration is required to achieve climate neutrality in 2050.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article