Tariffs, costs and carbon – the triple challenge of greening aluminium

Aluminium’s shift towards sustainability presents a complex mix of challenges and opportunities. This article explores the business case for decarbonising aluminium production, with leading producers currently prioritising clean electricity and recycling initiatives

Reducing carbon emissions from aluminium production: a focus on the business case

Aluminium is integral to modern life. Its lightweight, durable, and versatile properties make it indispensable across numerous industries, from transportation to construction. The metal’s role in the transition to a low-carbon economy is equally significant. Aluminium is crucial in the manufacture of solar panels, wind turbines, battery enclosures, and hydrogen fuel cells – all essential technologies for a sustainable future. Moreover, the industry has garnered renewed interest as gallium, a byproduct of refining bauxite into alumina, is now recognised as a critical mineral for semiconductors, 5G networks, artificial intelligence, satellite systems, and defence technologies.

In 2024, global primary aluminium production totalled 73 million metric tons, with China commanding the lion’s share at 60%, while the US and Europe contributed less than 10% combined.

Despite aluminium's pivotal role in the energy transition, its production is marred by significant carbon emissions, emitting nearly 1.1 gigaton of CO2. That equals about 3% of the world’s direct industrial CO2 emissions and 0.5% of total global greenhouse gas emissions. That might not seem like much, but aluminium stands out when compared to other modern materials. Producing a ton of aluminium in Europe or the US releases about 4,800 kilograms of CO2 into the atmosphere, which is far more than a ton of cement (800 kilograms), plastic (1,300 kilograms), or steel (1,900 kilograms). The contrast is even starker in China, where coal-intensive production methods push emissions to around 15,000 kilograms of CO2 per ton, making aluminium one of the most carbon-intensive materials in the global industrial landscape.

Aluminium is one of the most carbon-intensive industrial materials in the world

Fortunately, several technologies and strategies offer promising pathways for reducing emissions in aluminium production. They are described in the tech-explainer at the bottom of this article, and we have discussed sector pathways here. This article focuses on the business case for various greening options, making it particularly relevant to corporate decision-makers who drive investment through viable business cases.

We analyse the business case of different ways to green aluminium production:

- Switching the anodes used in the production process. Anodes are often made from carbon, which reacts with CO2 in the process. Inert anodes are not made from carbon, and in turn, this source of emissions is eliminated.

- Change the heating source from fossil fuels like coal or gas to electricity or hydrogen.

- Capturing and storing the emissions from aluminium production (CCS).

- Switching from virgin production to recycled aluminium with hardly any loss in product quality.

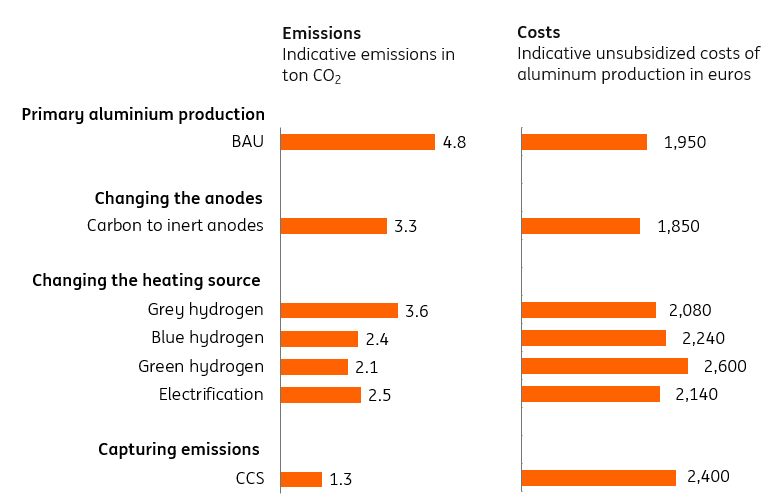

Switching to inert anodes, other heating sources or CCS can significantly reduce aluminium’s emissions, though most options come with a distinct cost

Indicative emissions and costs of primary aluminium production in Europe*

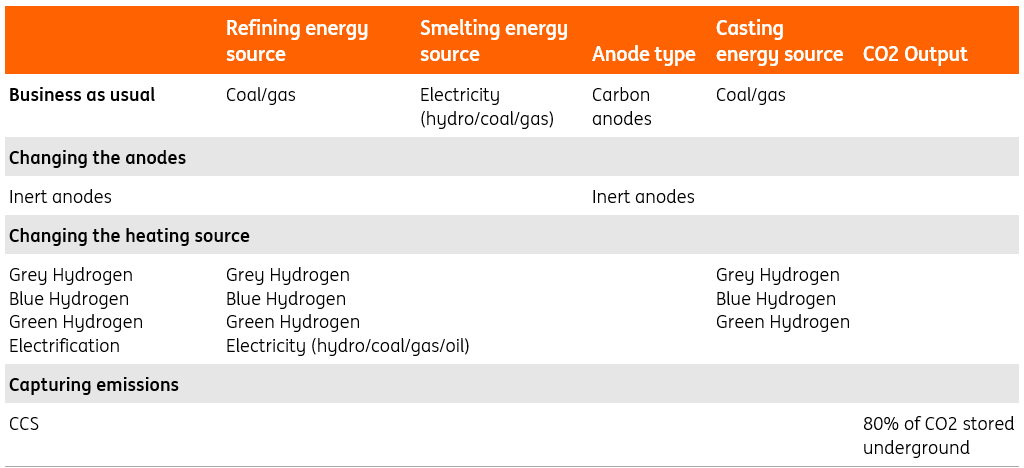

Changing the anodes

Traditionally, the smelting process relies on carbon anodes, which contribute significantly to CO2 emissions during the chemical process. Switching to inert anodes can potentially reduce emissions by approximately 1.5 tons of CO2 per ton of aluminium produced – about a third of emissions for EU and US manufacturers, and around 10% for Chinese producers, who emit nearly three times more due to their reliance on coal.

Firstly, inert anodes have a longer lifespan and require less frequent replacement, reducing maintenance and operational costs. Secondly, they consume less electricity during the smelting process, leading to significant energy savings. Additionally, these anodes do not produce CO2 emissions during the reaction, eliminating the need for costly carbon offsets or mandatory carbon credits. Furthermore, they do not emit fluorocarbons, which are potent greenhouse gases with a global warming potential 6,000 to 11,000 times greater than CO2.

Despite these potential benefits, inert anodes are not yet widely used. Companies like Alcoa, Rio Tinto and Rusal are developing it, but the technology is still in the pilot or early commercial stage. The biggest hurdle is finding a material that is truly inert in the extreme conditions of the aluminium electrolysis. While the upfront costs of adopting inert anodes are not the primary obstacle, some hesitation remains in the industry. Traditional carbon anodes have demonstrated reliability and process optimisation for more than a century, making aluminium smelters cautious about transitioning to newer, less proven technologies.

Changing the heating source

Aluminium production requires very high temperatures that are currently generated with fossil fuels, so changing the heating source can lead to significant reductions.

Aluminium smelting is already fully electrified worldwide – a key reason for its high electricity demand – yet alternative technologies such as industrial heat pumps, plasma heating, and induction heating are emerging as promising methods for generating the intense heat required for production. While these electrification technologies remain challenging to implement in the core refining process, they are increasingly used for preheating, drying, alloying, and casting.

For example, Hydro signed a €1.63 million contract with Pyrogenesis to procure plasma technology for its cast house in Sunndal, Norway. This technology will enable Hydro to use electricity instead of natural gas or other fuels to produce the high-temperature heat required in cast-houses. The company aims to start operating this facility in 2026. When powered by renewable energy, they can further reduce emissions. Our analysis suggests that electrifying the heating process with renewables could cut emissions by half, though this transition comes with a 10% increase in costs, as these technologies are still in their early stages and remain relatively expensive.

Hydrogen could, in theory, be used as a heating source. While several laboratory-scale tests have been conducted worldwide, hydrogen’s unique properties – burning hotter and faster than natural gas – pose challenges for furnace and burner design, as well as for safety and control systems. In 2023, Norwegian company Hydro achieved a milestone by producing its first batch of aluminium using hydrogen, although this process was applied to recycled rather than primary aluminium. And Novelis conducted a successful trial in the UK with support from Progressive Energy and UK government funding.

Should the technical hurdles be overcome at an industrial scale, using green hydrogen could cut emissions by up to 60%, offering a substantial environmental benefit. Yet, the current supply of blue and green hydrogen falls far short of what would be required for large-scale aluminium production. Even if it were available, relying on green hydrogen would increase aluminium production costs by roughly one third – a significant challenge in a market where producers must contend with fierce international competition. Additionally, the limited availability of low-carbon hydrogen means it may be more effective to prioritise its use as a feedstock in greener steel or plastic manufacturing, rather than dedicating it solely to aluminium heating.

Capturing and storing emissions (CCS)

Capturing and storing emissions from the production process and power generation by coal or gas plants yields the biggest climate impact in the case of virgin aluminium production. Emissions can be reduced by up to 75%, but it comes with a 25% cost increase in the absence of carbon pricing. While carbon capture and storage (CCS) technology is being developed for aluminium production, it remains in the early stages of implementation. For instance, Norwegian company Hydro is working on CCS solutions that could be retrofitted into existing aluminium smelters, aiming to launch an industrial-scale pilot by 2030.

However, capturing CO2 from smelter off-gases presents significant challenges, as the concentration of CO2 is relatively low – about 1%. This low concentration makes the process more complex compared to other industries, such as refineries, plastics, cement, hydrogen, or fertiliser production, where CO2 concentrations are typically much higher and therefore easier to capture. As a result, CCS is likely to advance more rapidly in those sectors than in aluminium production.

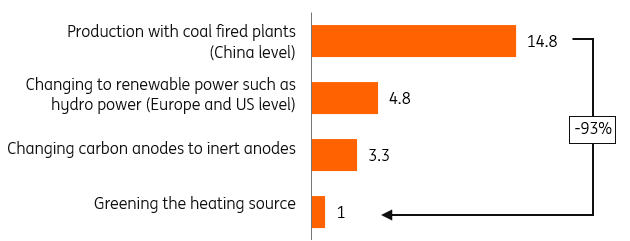

Ways to green primary production of aluminium

How can the sector set itself on a path to net zero with these novel technologies?

Switching to renewable power sources is the most significant step in reducing the carbon footprint of aluminium production. At present, China, which is responsible for 60% of global aluminium output, primarily depends on coal-fired power plants, resulting in remarkably high emissions of approximately 15 tons of CO2 for every ton of aluminium produced. By contrast, Europe and the US predominantly use hydropower, which reduces emissions to about five tons of CO2 per ton. Since the start of 2024, aluminium producers have committed to 4.9GW of renewable power purchase agreements, according to Bloomberg New Energy Finance. However, even with 100% renewable energy, emissions from primary aluminium production remain significantly higher than those from materials such as cement, plastic, or steel.

Switching to renewable power is the biggest lever for cutting aluminium’s carbon footprint

Indicative emissions for primary production in ton CO2 per ton aluminium

To further reduce emissions, the industry must adopt inert anodes to prevent CO2 emissions that inevitably arise when carbon anodes are used. Together with the use of renewable power, this could lower emissions to about 3.3 tons of CO2 per ton. Greening the fossil-based heating sources could further reduce emissions to about one ton of CO2 per ton. Carbon capture and storage (CCS) could be applied if producers continue to use fossil fuels like coal or gas, either through post-combustion CCS or pre-combustion using blue hydrogen. Electrification of heating sources could reduce the sector’s dependence on fossil fuels, either through heat pumps or electric boilers powered by renewable energy or through green hydrogen produced by electrolysers powered by renewable energy.

These measures collectively yield an impressive 93% reduction in emissions for primary aluminium production, providing the prospect of primary production in a net-zero economy. The remaining emissions (about one ton of CO2 per ton of aluminium) could be offset in other markets or avoided by substituting the demand for aluminium.

A suite of technologies could reduce emissions from primary aluminium production by over 90%, but emissions cannot be eliminated

While these innovative technologies are still in their infancy, meaningful progress will depend on three factors.

First, extensive pilot programs and significant scaling efforts need to be undertaken before the sector can truly achieve net zero. At present, such efforts are limited. Bloomberg New Energy Finance tracks developments within the industry, and notably, there have been no new projects aimed at decarbonising primary aluminium production since November 2024. The industry's main priority remains the transition from coal-fired power to cleaner electricity sources, including hydropower, wind, solar, and nuclear energy. This gradual transition is already shaping the emissions profile of the sector; despite global aluminium production increasing by 6% annually, total emissions have levelled off. Nevertheless, significant reductions in absolute emissions are still required if the industry is to make a meaningful contribution to combating global warming.

Second, aluminium buyers must be willing to pay a green premium to motivate producers to invest in environmentally friendly aluminium and help bridge the price gap. Unfortunately, enthusiasm among buyers – automobile manufacturers, for instance – for paying higher prices remains limited. This hesitancy complicates the London Metal Exchange’s efforts to introduce a green premium for sustainably produced metals. While industry advocates have called for price differentiation between clean and conventional supplies, these calls have yet to translate into higher premiums, rendering price signals largely ineffective.

Finally, this situation increases the responsibility of governments to close the price gap if they are truly committed to advancing the decarbonisation of primary aluminium production.

The strong case for aluminium recycling

There’s no way of getting around recycling when thinking about the sector’s current and future state, as it significantly reduces both costs and emissions compared to primary aluminium production. By reprocessing scrap aluminium, the industry can save up to 95% of the energy required to produce aluminium from raw materials. This energy efficiency leads to a dramatic decrease in CO2 emissions, with recycled aluminium currently generating only about 0.4 tons of CO2 per ton, compared to the 4.8 tons produced by virgin aluminium in Europe. And with elevated energy prices in Europe, it does so at a 25% to 30% cost reduction, lowering the price of aluminium to about €1,400 per ton.

Furthermore, recycling aluminium can be repeated almost indefinitely without significant degradation in quality, making it an excellent sustainable alternative. In that regard, recycled aluminium tops recycled plastic or steel, which often yield quality degradation due to impurities, limiting their application in fields such as food packaging or precision machinery.

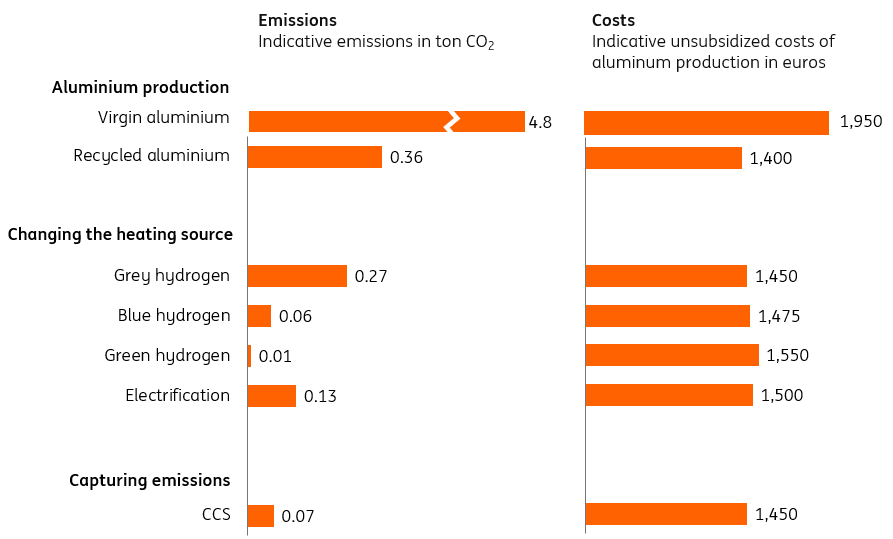

Recycling brings lower costs and emissions

Indicative emissions and costs of recycled aluminium production*

The emissions from aluminium recycling can be lowered further by applying similar principles as in primary aluminium (changing the heating source and capturing emissions, note that recycling does not involve anodes). However, from an absolute emissions reduction perspective, these technologies can be best applied to primary production. And shifting from primary production to recycling makes a far bigger impact than further greening the recycling process. The cost advantage of recycled aluminium compared to virgin aluminium and the robust quality recycling yields will be strong drivers in this direction.

It's more impactful to enhance recycling rates than to further green the recycling process

Despite these advantages, the global recycling input rate (RIR) for aluminium remains at just 32. In other words, only 320 kilograms of every ton produced comes from recycled sources. North America leads with a rate of 57, indicating that recycled aluminium now exceeds primary production there. However, there is considerable room for improvement worldwide, as currently only about half of all aluminium scrap is actually recycled.

Innovation is now largely driven by the waste collection industry, where companies are increasingly investing in advanced technologies such as laser-induced spectroscopy and digitalisation to enhance the precision of recycling sorting. By purifying the feedstock for aluminium recycling in this way, recyclers are able to achieve higher product quality and more competitive pricing.

Although global demand for aluminium continues to rise, it’s important to note that about 75% of the nearly 1.5 billion tonnes of aluminium ever produced remains in active use – and isn’t likely to become scrap in the near future. As a result, the industry will need to rely on a combination of recycled and primary aluminium for years to come. To meet sustainability goals, the sector must pursue a dual strategy: increasing the share of recycled aluminium through better recycling technologies and infrastructure, while also making primary aluminium production as environmentally friendly as possible. This article explores the business cases for both approaches, offering insights that may help to guide future decisions by corporate leaders and policymakers.

Special thanks to

The authors thank Brett Belien, master's student in Chemical Engineering at Delft University of Technology, for excellent research assistance.

Appendix: Aluminium’s tech explainer from an economist

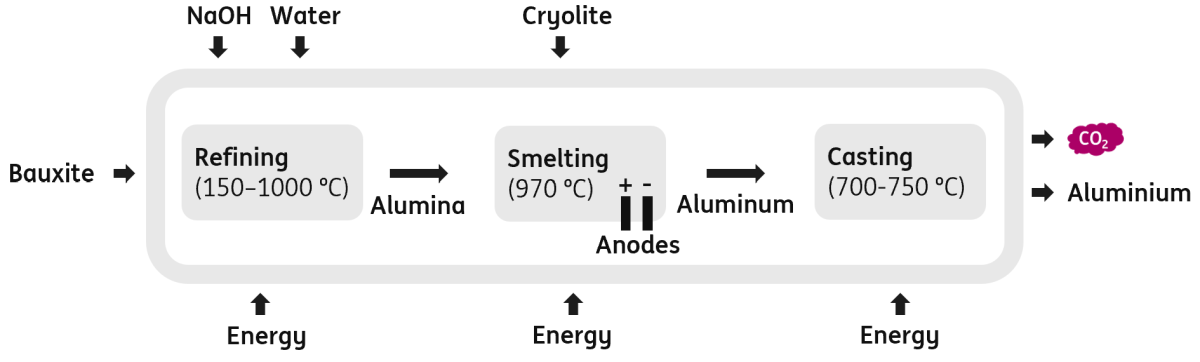

The production of virgin (primary) aluminium consists of three major steps.

- Refining. The first step begins with the mining of bauxite ore, which contains alumina (aluminium oxide) as its key component. Through the Bayer process, alumina is refined from bauxite using caustic soda (NaOH) at temperatures ranging from 150°C to 1000°C. The heat used for this process is typically generated by burning fossil fuels like coal or natural gas.

- Smelting. The purified alumina is then smelted into aluminium metal via the Hall-Héroult process, which involves dissolving alumina in molten cryolite and applying a strong electric current (around 400 kA) at approximately 950°C. This process consumes about 14 MWh of electricity per ton of aluminium, roughly equivalent to the annual electricity use of five Dutch households. A typical smelter, with an output of up to 500,000 tons per year, can use as much electricity as entire cities like San Francisco or Amsterdam. CO2 emissions arise both from the carbon anodes used in the reaction and, more significantly, from fossil-fuel-based electricity generation.

- Casting. The resulting molten aluminium is cast at around 700°C into ingots, again using heat typically sourced from fossil fuels.

Process of producing primary aluminium

Visualisation of current process (business as usual)

Process of greening primary aluminium production

Visualisation of different greening steps to the process

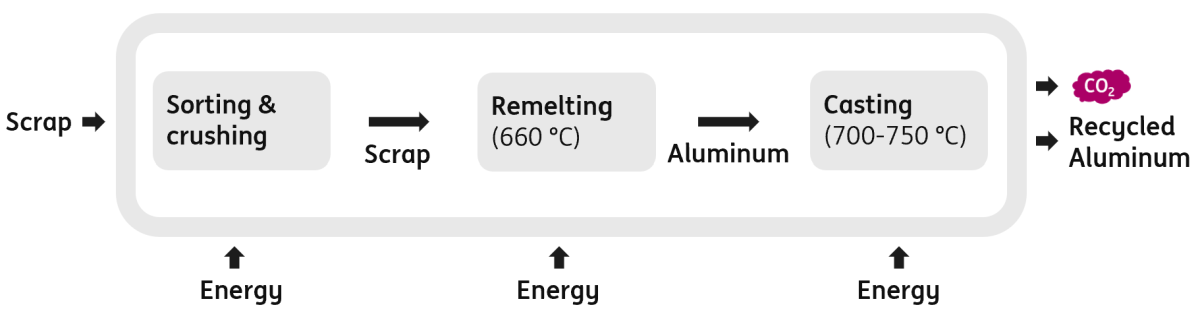

In contrast, recycled (secondary) aluminium production bypasses the energy-intensive refining and smelting steps. Scrap aluminium, sourced from used products or manufacturing waste, is simply cleaned, sorted, and remelted at around 600–700°C. This process requires only about 5% of the energy needed for primary aluminium production and results in significantly lower CO2 emissions. However, the quality and type of scrap can influence the energy use and emissions profile. Despite its lower environmental footprint, recycled aluminium still relies on fossil fuels for heat unless alternative energy sources are used.

Process of producing secondary/recycled aluminium

Visualisation of current process (business as usual)

Appendix: our economic assumptions

For aluminium production, capital expenditure (capex) assumptions vary by region. In Europe and the US, capex ranges from €5,000 to €7,000 per ton of annual aluminium capacity, while in China it ranges from €2,000 to €4,000. The lower end reflects a business-as-usual (BAU) scenario. Increases in capex are attributed to the installation of inert anodes, modifications to enable hydrogen use in the Bayer process, and the retrofitting of refining and casting facilities to replace fossil fuels with electricity. Plants are assumed to operate at a 90% capacity factor. The plant lifetime is assumed to be 35 years, with a discount rate of 8% and inflation at 3%.

Our figures are calibrated for Europe using a power price of €45/MWh (low power price region such as the Nordics), a gas price of €38/MWh, and a coal price of €95/ton. Key input prices include €70/ton for bauxite, €450/ton for carbon anodes, and €1125/ton for aluminium scrap.

Specific capex adjustments include an increase of €360*year/ton for inert anode fittings, plus an additional 10% for general retrofitting. Hydrogen-readiness adds 25% to capex, while electrification of the refining process (excluding smelting, which is already electric) applies a 250% capex multiplier on the refinery. Hydrogen is assumed to be produced on-site (so no transport costs) at prices of €1.40/kg for grey hydrogen, €2.20/kg for blue hydrogen, and €4.10/kg for green hydrogen.

For carbon capture and storage (CCS), the assumed cost (including capex) is €55/ton CO2 for emissions from coal power plants, €100/ton CO2 from gas power plants, and €225/ton CO2 for process emissions from the Hall-Héroult reaction between alumina and carbon anodes. The effective CCS capture rate was set at 82% and the EU ETS carbon price at €75/ton. When carbon prices are applied, we have assumed full carbon pricing (no free allowances, so every ton of carbon is priced).

We have used an exchange rate of 1 dollar to 0.90 euro to convert dollar values to euro.

In practice, all these input variables show considerable variation, which yields a wide range of outcomes for every technology. We have chosen to present point estimates as they often capture the main insights better than wide ranges. Treat these numbers as indicative outcomes around which real-time projects will vary.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

29 July 2025

Why Europe struggles to decarbonise aluminium, even in a world without US tariffs This bundle contains 2 Articles