Greening aluminium: How to cut emissions

Making aluminium more sustainable is becoming a top priority. The metal is used in countless processes, and it accounts for some 3% of global emissions. Switching to clean power offers the highest potential for decarbonisation. As for other technologies, we’re going to examine the potential options, but they come at a cost

The aluminium industry contributes around 3% of global emissions, and with the demand for the metal set to soar, it's now crucial to decarbonise the production processes.

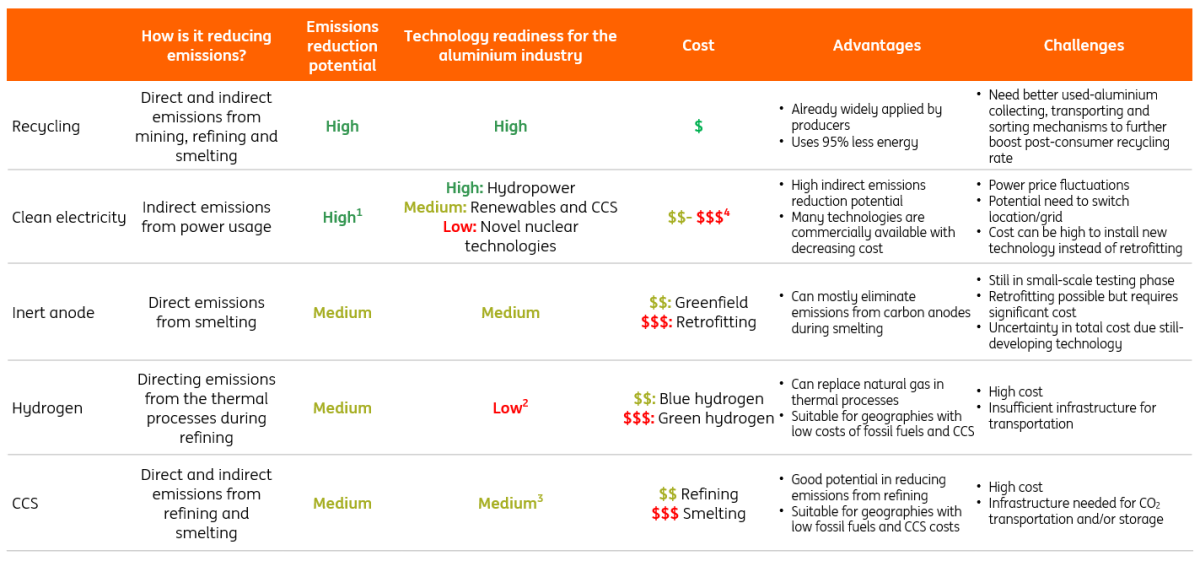

Several decarbonisation pathways have emerged, and this is what we're going to focus on here:

- recycling

- clean electricity

- inert anodes, hydrogen, and

- carbon capture and storage (CCS)

While recycling is a highly cost-effective approach, supplying aluminium production with clean electricity paints a more mixed picture depending on sources of generation and location. Meanwhile, inert anodes, hydrogen, and CCS are emerging technologies for a greener aluminium industry, but they differ in application outlook, cost, the timeline of application, and so on.

Your cheat sheet to aluminium decarbonisation pathways

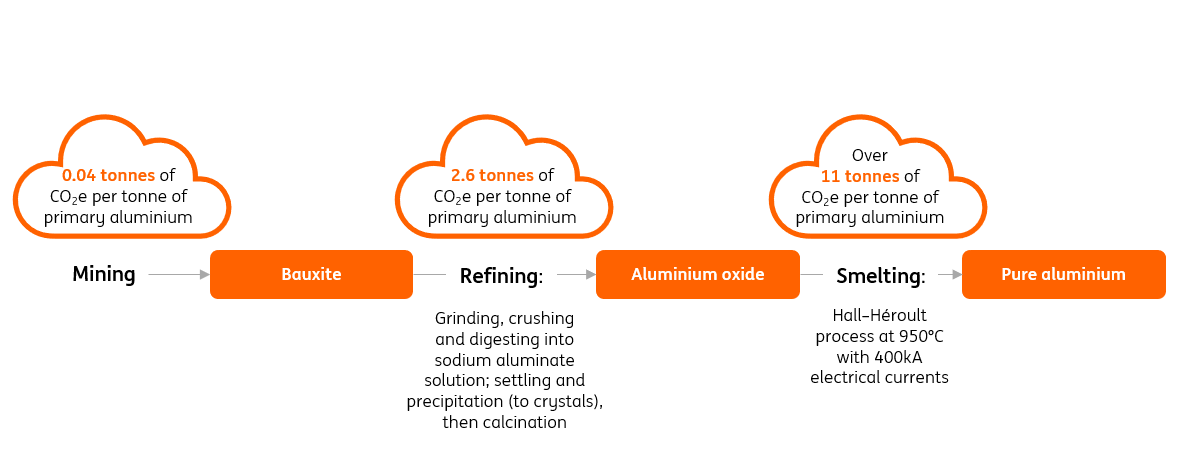

How is aluminium produced?

As we discussed in our previous article, aluminium production can be divided into three main steps: mining and filtering out the bauxite, refining it into aluminium oxide, and smelting it into aluminium.

Recycling

One of the most effective ways to reduce emissions from the aluminium industry is recycling. Recycling consumes up to 95% less energy than producing it, making the cost largely manageable when energy savings are taken into account. The characteristics of the metal allow it to be recycled again and again without losing quality. Because of this, aluminium cans are the most recycled container on earth, and 75% of all aluminium ever produced is still being used today.

Yet, despite significant environmental benefits, only about 34% of the aluminium produced in 2018 came from recycled materials. According to forecasts by Rocky Mountain Institute (RMI), that figure needs to increase to 54% for the industry to reach net-zero emissions by 2050. The share of aluminium production from primary (i.e. new) materials would drop from 67% to 46%.

Forecast of aluminium production inputs in the 'net-zero by 2050' scenario

Million metric tons

More attention needs to be paid to post-consumer recycling than to pre-consumer recycling. Pre-consumer recycling refers to reusing the leftover materials from aluminium production, whereas post-consumer recycling means collecting finished aluminium products (e.g., beverage cans), processing them, and reusing them as input for production.

It is increasingly acknowledged that although both processes recycle aluminium, post-consumer recycling is the desired method because the aluminium produced will have already completed its life cycle and can register emissions reductions if it is used again. In contrast, pre-consumer recycled aluminium will not have ‘served its purpose’ and still needs to book the carbon emissions from the original production process.

Tackling the impurity challenge

Admittedly, recycling aluminium from used products means producers need to tackle the impurity challenge, as the used aluminium is often mixed with plastic labels, dirt, and so on. But impurity is not a deal-breaking problem, and solutions are being developed and improved. Meanwhile, the environmental benefits of emissions reduction and waste management can more than offset the efforts needed to purify used aluminium.

As such, under RMI’s net zero by 2050 scenario, the share of post-consumer recycling in aluminium production will increase from the current 20% to 46% by the middle of the century, and the share of pre-consumer recycling will drop from 14% to 9%.

Now, with a higher corporate focus on circularity, more aluminium producers are ramping up production from post-consumer recycling. Hydro, an aluminium and renewable energy company, is offering a product called Hydro CIRCAL that has at least 75% of post-consumer scrap. Alcoa, another aluminium producer, is advancing its ASTRAEATM recycling process to convert low-quality post-consumer aluminium scrap to high-purity aluminium.

From a societal perspective, increasing the supply of post-consumer scrap can boost the rate of post-consumer recycling. This can be done not only by having more defined recycling signs and trash cans but also by enhancing a city/municipality’s trash sorting facilities (many consumers believe that whatever gets separated at trash cans gets mixed again at processing facilities).

Clean electricity

Greening the mix of electricity an aluminium producer uses can also substantially change its emissions profile (reduce Scope 2 emissions). Aluminium production is a highly electricity-consuming process because the smelting process alone requires electric currents constantly running at 400 thousand amperes (A). In 2021, half of the electricity used to power the smelting process came from coal, and that is largely because China is the world’s largest aluminium producer, and the country’s aluminium production is predominantly coal-powered.

To reach net zero emissions by 2050, about half of the electricity used to power the smelting process needs to come from renewable energy, nuclear, and hydropower, according to an analysis by the Mission Possible Partnership (MPP), an alliance focused on facilitating the decarbonisation of high-emitting sectors. The remaining half will need to be powered by fossil fuel-based captive power equipped with CCS technologies.

Power mix of primary smelting processes

Reducing Scope 2 emissions from power usage involves being connected to a cleaner grid, developing standalone clean power to be directly used for aluminium production, or buying renewable power purchase agreements (PPAs). The best solution depends on both a company’s general strategy and the location of production. As we've previously mentioned, China has been transitioning a lot of its aluminium production from coal-rich areas to hydro-rich areas.

Many companies are also relying on Power Purchasing Agreements or PPAs. Rio Tinto, for instance, signed a renewable PPA for its aluminium operations in Australia, a region where coal accounts for 45% of the aluminium smelter electricity usage. Alcoa is selling EcoLum aluminium, which is produced predominantly at hydro-produced smelters. Reducing Scope 2 emissions from hydro and renewable sources can be a cost-effective means of green production for these actions that do not involve moving production locations or building completely new plants.

Nuclear is expected to account for more than 20% of the smelting electricity source by the MPP, and we agree that nuclear plays a role in decarbonising the grid and especially energy-intensive activities in the long term. The novel nuclear technology, Small Modular Reactors (SMRs), can be a powerful standalone electricity source capable of powering one or more aluminium sites without having to be connected to the grid. However, SMRs are still in the Research & Development phase. So, in the short to medium term, because of caution on traditional nuclear plants and the nascent stage of SMR technologies, nuclear’s contribution to decarbonising the grid will be limited.

Inert anodes

Since smelting accounts for most of the emissions from aluminium production, emerging technologies are being developed to decarbonise that process. One that is gaining popularity is inert anodes, which replace carbon anodes in smelters. Traditionally, aluminium oxide runs through a smelter with carbon anodes, where oxygen is removed from the oxide and reacted with the carbon anodes.

As a result, high-purity aluminium is produced, but so is carbon dioxide (CO2). An inert anode, however, does not contain the carbon element and is instead made of cermet, metal alloys, or other suitable materials. With inert anodes, the products of the smelting process are high-purity aluminium and oxygen.

Aluminium smelting process - traditional vs. inert anodes

This means that inert anodes have the potential to eliminate almost all the direct emissions (non-electricity and heating related) from the smelting process, bringing huge environmental benefits. The technology is still under development and not commercially available, but the outlook looks promising. In 2019, Elysis, a joint venture between Alcoa and Rio Tinto, succeeded in producing aluminium using inert anodes and started constructing the first commercial-scale prototype cells of the inert anode technology at a Rio Tinto smelter in Quebec, Canada.

Inert anodes are not yet commercially available, but because of the successful pilots mentioned above, the technology has the potential to be applied more widely in a shorter timeframe. The fact that inert anodes remain in the testing and development phase also makes it hard to estimate the cost, especially when it comes to the broader market. Now, some research groups believe that the cost of installing greenfield inert anodes would likely be ‘medium’ compared to green hydrogen and CCS for aluminium smelting (‘high’). A report published by MPP suggests that retrofitting smelters to include inert anodes is possible but would require significant costs, which can make retrofitted inert anodes a less attractive option than CCS in smelters.

Hydrogen

Hydrogen has been explored as an alternative to natural gas to be combusted during the industrial heating processes for producing steel, petrochemicals, and so on. The same technique is also being developed in aluminium production. Natural gas or coal is typically burned during the refining process to provide a heated environment of roughly 300 degrees Celsius for digestion and 950 degrees Celsius for calcination. With hydrogen as an alternative, only water, instead of CO2, would be produced from the combustion. Such a method can substantially reduce the indirect emissions associated with refining.

Yet, the cost is hindering a faster application of hydrogen in the aluminium industry. Today, both green hydrogen (produced from electrolysing water using renewable power) and blue hydrogen (produced from fossil fuel sources with CCS) are still visibly more expensive than grey hydrogen (produced from fossil fuels without abatement). For blue hydrogen, CCS technologies are expensive to adopt; for green hydrogen, not only are electrolysers pricey to install but the availability and cost of renewable power are also a challenge.

In 2023, green hydrogen was more expensive than natural gas in all the countries listed below, according to Bloomberg New Energy Finance. And the gap is considerable in areas with low natural gas prices and/or high renewable power and electrolyser costs.

Levelised green hydrogen costs compared to natural gas prices in selected countries

2023, $/MMBtu

The cost outlook of green hydrogen may significantly improve in the medium to long term, with the lowest possible cost of green hydrogen maybe trending below the lowest cost of grey hydrogen by around 2030. Policy incentives, which are being rolled out by many governments, can also boost cost competitiveness.

Levelised cost of different shades of hydrogen compared with natural gas prices

$/MMBtu, based on data from over 20 countries

For hydrogen to take off even faster, its transportation infrastructure—pipelines, suitable trucks, ships, or a combination of all of them—needs to be significantly strengthened.

Today, the use of hydrogen to decarbonise production is seen less often in aluminium than in other energy-intensive industries. Hydro produced the world’s first batch of aluminium in a test with renewable hydrogen in 2023, and since the aluminium was produced from post-consumer scrap, the production process was essentially carbon-free. One can hope that such applications will become more widespread as the hydrogen industry matures.

Alternatives to hydrogen: biofuels and electrification

It is worth mentioning that competing technologies can potentially replace hydrogen as an alternative to natural gas. These include biofuels, which can be used for combustion, and electrification, which essentially eliminates the combustion process.

Among biofuels, renewable natural gas (RNG or biomethane) can be used to replace fossil natural gas. And because RNG has the same chemical composition as natural gas, it can serve as a ‘drop-in’ fuel that involves minimal infrastructure retrofitting. But just like many other clean energy options, RNG prices are visibly higher than natural gas, especially in areas where natural gas prices are low. RNG adoption in the aluminium industry is, therefore, low and will rely on policy support to scale up.

As for electrification, some research shows that replacing traditional furnaces with electrical ones can be more cost-effective than burning hydrogen in the low to medium-heat processes of refining in aluminium production. For the high-heat processes during refining, clean fuels like hydrogen would be a more suitable option, given the level of temperature and energy needed.

Carbon Capture and Storage

Finally, CCS is an emerging technology that can help the aluminium industry decarbonise. CCS can reduce carbon emissions from two parts of aluminium production:

- CO2 generated from industrial heating and processing

- CO2 generated during the smelting process when aluminium oxide reacts with carbon anodes

Although CCS technologies have existed for a long time and have reached commercial viability, their application in the aluminium industry is a lot more nascent with sector-specific challenges. In 2022, Aluminum Bahrain (Alba) and Mitsubishi Heavy Industries signed a memorandum of understanding to evaluate how to use CCS technologies to reduce emissions from Alba’s plants, but no concrete result has been communicated since then. More recently, Fives, an industrial engineering group, set up a consortium with Aluminum Dunkerque, Trimet, and Rio Tinto to develop CCS solutions. Hydro also announced it's set to explore CCS in aluminium production but expects to develop an industrial-scale pilot only by 2030.

The high cost of applying the technology to smelting

The biggest challenge to adopting CCS in aluminium production is the high cost of applying the technology to smelting. To begin with, for any industry, deploying CCS already requires high upfront costs that can be hard to recover without policy incentives or other revenue streams, such as selling captured carbon. For aluminium smelting, specifically, capturing costs can be even higher. A main factor determining the cost of capturing is the CO2 partial pressure of a flue gas stream at the point source of emissions, which is directly related to CO2 concentration: the higher the CO2 concentration is, the higher its partial pressure is, and the lower the per-ton capturing cost is.

Aluminium smelters have one of the lowest carbon partial pressures among most sectors. This makes the cost of capture in aluminium smelters high, likely two to four times the cost of CCS in iron and steel production and approximately 25 times the cost in natural gas processing, fertiliser, and bioethanol production. Such a high cost of capturing CO2 from smelters makes inert anodes a promising alternative, as it aims to achieve the same effect.

Cost of CCS in various types of power and industrial processes

Excluding downstream CO2 compression

2020 dollars per tonne of CO2

However, the high per-unit cost of CCS only applies to capturing CO2 from smelters. The cost for refining and heating in the rest of the production process is much lower, at a level comparable to applications in many other industries. This suggests that CCS can still have good potential in decarbonising aluminium production, just not for the smelting part in the short to medium term.

The challenges ahead

Reducing emissions is challenging for an energy-intensive industry such as aluminium, but efforts are underway. It is worth emphasising that simply switching to clean electricity sources such as hydro, solar, wind, and nuclear power can already lead to a roughly 75% reduction in emissions from the industry globally.

Reducing direct emissions from the production process is also important, though many possible technologies, such as hydrogen and CCS, remain costly to deploy. Although aluminium consumers are now keener to manage Scope 3 emissions, the high price tag for green aluminium is hindering faster demand growth. This means that significant investment is needed to fuel the R&D and infrastructure improvement.

Government policy is crucial to making this happen, be it financial incentives for clean aluminium production, carbon pricing, initiatives for clean aluminium production hubs, or other means. In future articles, we will explore the business case of these technologies and policies.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

14 November 2024

Greening aluminium: Its less than shiny net-zero reputation This bundle contains 3 Articles