Greening aluminium: The urgent need to reduce emissions

Producing aluminium from raw materials requires more energy than any other industrial manufacturing method. While emissions are decreasing slightly, they need to fall much faster if we are to reach net zero by 2050, and greener methods of production are urgently needed

Aluminium is a key material for industries aiming to reduce their carbon footprints - and demand is soaring. However, its production is highly energy-intensive; it emits around 3% of the world’s direct industrial CO2 emissions. Producers are under mounting pressure to slash those emissions. True, they are decreasing, but they need to fall much faster if we're to reach net zero by 2050 and greener methods of production are increasingly needed.

Aluminium is used just about everywhere, from transport to buildings, aerospace to defence. It also plays a key role in energy generation, transmission, and storage technologies, notably those delivering the energy transition, such as wind and solar power, alternative fuel cells, hydrogen production, high-voltage cables, and batteries.

What causes aluminium’s emissions?

The world consumes around 70 million tonnes of aluminium each year, and due to its role in decarbonisation, that number is expected to increase by almost 40% by 2030.

In addition to direct emissions resulting from the aluminium smelting (Scope 1 emissions), aluminium production also results in indirect emissions from the electricity or heat purchased for the aluminium production process (Scope 2 emissions).

Aluminium production from raw materials – primary aluminium production – requires more energy than any other industrial manufacturing method and releases large amounts of carbon dioxide into the atmosphere. Recycled, or secondary aluminium, produces around 5% of emissions compared to primary aluminium.

In primary aluminium production, the energy-intensive series of processes that turn raw bauxite ore into a pure metal emit, on average, 15 tonnes of CO2 for every metric tonne of primary aluminium produced on a cradle-to-gate basis. This includes both direct and indirect emissions for the production process and inputs from raw material extraction until the product leaves the factory, according to data from the International Aluminium Institute (IAI).

Smelting is the most energy and carbon-intensive step in aluminium production

To achieve the goal of limiting global warming to within the threshold of 1.5° by 2030, as envisioned by the Paris Agreement, the aluminium industry needs to reduce its emissions to less than 0.5 tonnes of CO2 per tonne of aluminium by 2050. That's according to data from the International Aluminium Institute.

Aluminium production involves three main stages: the mining of bauxite, refining into alumina and smelting into aluminium.

Mining bauxite is not particularly carbon-intensive – bauxite mining contributes just 0.04 tonnes of CO2e/tonne of primary aluminium. Refining is a more carbon-intensive process, contributing 2.6 tonnes of CO2 per tonne of aluminium. Those emissions are largely from the burning of fuels to produce heat.

The most energy- and carbon-intensive step in aluminium production is the smelting of alumina into aluminium.

Smelting is the most significant source of aluminium’s emissions

Aluminium emissions vary hugely depending on the power source used in the smelting process. This varies by geography. In North America, Europe and Russia, aluminium is typically made using hydro power, which has a relatively low emission intensity. In China and India, aluminium is made predominantly using coal power, resulting in high carbon intensity.

Greenhouse gas emissions intensity in primary aluminium

Cradle to grate (tonnes of CO2e per tonne of primary aluminium)

The latest data from the IAI showed that, for the first time, total greenhouse gas emissions from the global aluminium sector were stable in 2022, even though aluminium production grew.

Production vs GHG emissions (million tonnes)

In 2022, aluminium production grew by 3.9%, from 104.1 million tonnes to 108.2 million. However, greenhouse gas emissions from the industry showed a slight decline from 1.13 giga-tonnes CO2e to 1.11 giga-tonnes CO2e, and the GHG emissions intensity of primary aluminium production (the average quantity of emissions from the production of a tonne of primary aluminium) has been declining since 2019. In 2022, intensity declined by 4.4% from 15.8 tonnes CO2e per tonne to 15.1 tonnes CO2e per tonne.

A shift towards more hydropower in China

The last time we saw a similar picture in the aluminium industry's GHG emissions was in 2009. The IAI data shows there was a production decline coinciding with the global financial crisis.

So, what's going on with this decoupling of production and the emissions trend? It is largely due to a shift towards more hydropower in China, the world’s largest aluminium producer. The increasing use of renewable electricity in other producing regions, including the Middle East and Australia, as well as investments in other emission reduction technologies, including fuel switching in alumina refining and increased aluminium recycling rates and efficiency, are also playing important parts.

How is China decarbonising its aluminium production?

China is the world’s largest producer of primary aluminium, accounting for nearly 60% of the global market. Like many others, its government is accelerating its efforts to decarbonise.

China's aluminium industry contributes significantly to the country’s carbon footprint, making up around 5% of its total emissions. Its primary aluminium production comes directly from mined ore rather than using recycled or alloy materials.

Primary aluminium production in China is overwhelmingly reliant on coal-fired electricity, over 70% of all energy used in 2022 (according to IAI data), which is why decarbonising the power supply for Chinese primary aluminium production is critical.

Due to the high proportion of coal-fired energy used, 12.7 tonnes of carbon is emitted per tonne of aluminium produced in China compared to a global average of 10.3 tonnes (according to IAI data covering the 2005 to 2019 period).

In 2018, China set a national capacity cap of 45 million tonnes for aluminium as part of its efforts to control power consumption in the sector.

Also, a trend that has become very clear in China is the moving of smelters from coal-fired electricity-dependent regions to hydropower-rich provinces, like Yunnan, as Beijing has set a goal of achieving carbon neutrality by 2060.

By 2027, 29% of China’s aluminium output is expected to be powered by green energy. If this trend continues, the average carbon intensity for Chinese aluminium producers will reduce significantly.

Primary aluminium smelting power consumption (2023)

The challenges in China's energy transition path

In 2023, China's share of coal-fired aluminium capacity was 72%, and that of hydro was about 19%. In Asia, excluding China, coal-fired capacity accounted for 86%, with only 2% using hydropower. In comparison, North America’s hydro share was 96% and Europe’s 94%.

China Hongqiao, the world’s largest private operator, has been increasingly relying on hydropower and solar energy. Its goal is to achieve peak emissions by 2025 and net zero by 2055. The producer is looking to move four million tonnes of capacity from the northern province of Shandong to China’s southwestern Yunnan province by the end of 2025 to take advantage of low-carbon energy. The company has an annual production capacity of more than 6 million tonnes per year.

However, China’s energy transition path is not without its challenges. Droughts over the past few summers forced cities in southwest China to curb power supply to heavy industries, disrupting aluminium production in the country. As China continues to decarbonise its aluminium industry, and as more smelters move from coal-dominated Shandong to hydropower-dominated Yunnan province, it's left more vulnerable to further disruptions, with green energy being heavily reliant on weather conditions and patterns.

Chinese producers will soon face extra costs for emitting carbon

Meanwhile, China plans to expand its national carbon trading market by including steel, aluminium and cement producers next year. A carbon tax is also being contemplated.

China’s current carbon trading system, launched in 2021, only covers the coal-fired power generation sector. The inclusion of these additional industries would extend the market’s coverage to about 60% of China’s total carbon emissions. Beijing aims to cover 70% of its total emissions by 2030.

The move means Chinese aluminium producers will soon face extra costs for emitting carbon, which could incentivise significant emissions reductions.

Chinese authorities hope lower emissions will help soften the blow to domestic producers from a new carbon tariff – CBAM (Carbon Border Adjustment Mechanism) – to be imposed by the EU from 2026.

What does CBAM mean for aluminium flows?

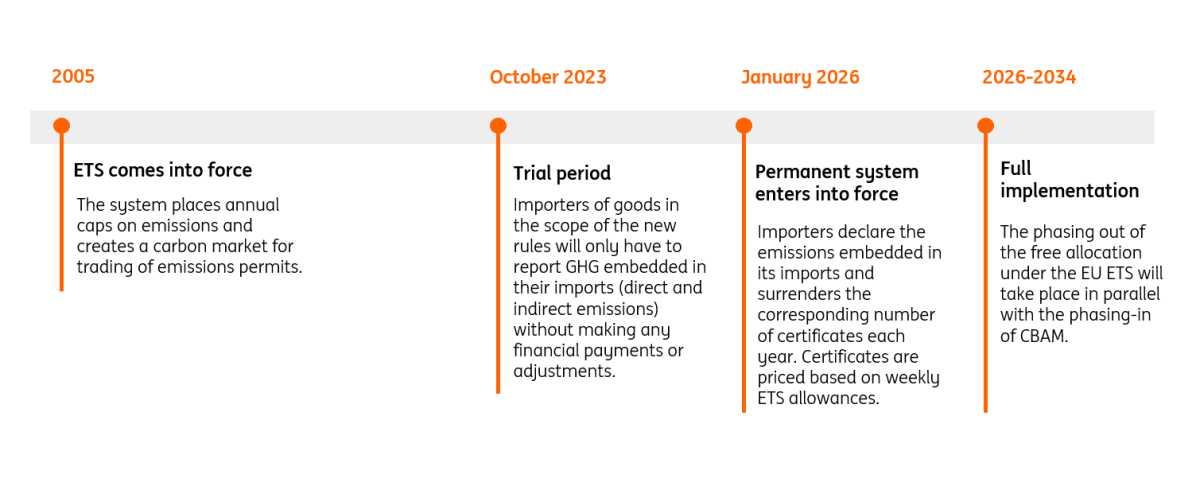

Under the Carbon Border Adjustment Mechanism agreement – the first of its kind globally – goods imported into the EU will face a levy at the border based on their emissions footprint. This will be phased in from 2026 until 2034.

The CBAM will initially apply to six carbon-intensive industries: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. These industries are at higher risk of carbon leakage. Eventually, the aim is for the carbon tax to cover all imports.

The CBAM entered its transitional phase on 1 October 2023, with the first reporting period for importers ending 31 January 2024.

During the trial period, importers of goods only have to report greenhouse gas emissions (GHG) embedded in their imports (direct and indirect emissions) without making any financial payments or adjustments. After the transitional period, indirect emissions will be in scope for some sectors, notably cement and fertilisers.

CBAM will come into force on 1 January 2026, and importers will need to declare each year the quantity of goods brought into the EU in the preceding year and their embedded GHG. They will then surrender the corresponding number of CBAM certificates. The price of the certificates will be calculated depending on the weekly average auction price of EU ETS allowances expressed in EUR per tonne of CO2 emitted. The phasing out of free allocation under the EU ETS will take place in parallel with the phasing in of CBAM in the period 2026-34.

CBAM timeline

CBAM will not apply to Iceland, Liechtenstein, Norway and Switzerland, given they already participate in the EU ETS or their domestic ETS is linked to it, as is the case for Switzerland. Additionally, goods imported from countries that have a carbon price can offset the amount paid under CBAM by an amount equivalent to their domestic carbon price.

The first and most obvious impact of the implementation of CBAM is that European consumers will face higher prices. This is not only because imports will be more expensive but also because the allocation of free allowances to a number of these domestic sectors will be gradually reduced as the CBAM is phased in, which will drive costs higher for EU producers. However, given the phase-out period for free allowances will run from 2026 to 2034, the impact will be felt gradually. Reporting obligations related to CBAM will also push up costs, which will likely also be passed on to consumers.

Trade flows will also likely be affected. This will be felt both with imports and exports. For exports, the eventual removal of free allowances will impact the export competitiveness of European downstream sectors.

For imports, there will also be large shifts. However, the degree of impact will really depend on how carbon-intensive some of these third-country producers are and whether these countries have a meaningful carbon price already in place to drive the decarbonisation of domestic industries in the coming years. Suppliers who have a carbon intensity similar to that of EU suppliers will likely not be significantly impacted in terms of competitiveness. Low-emission producers are likely to increase their share of exports to the EU, given the lower CBAM burden they would face, while higher carbon emitters will likely look for markets where their high emission intensity will not be penalised.

CBAM process

To meet global climate targets, the aluminium industry must accelerate its transition to greener production methods. By increasing recycling, adopting renewable energy and deploying emerging technologies such as hydrogen, carbon capture and inert anodes, the sector can significantly reduce its carbon footprint.

And we'll be discussing the different ways we can decarbonise aluminium production in our next article in this special Greening Aluminium series.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

14 November 2024

Greening aluminium: Its less than shiny net-zero reputation This bundle contains 3 Articles