Goldilocks GDP feeds the US soft landing narrative

GDP growth was a little stronger than expected in 2Q 2023, but inflation pressures continue to moderate, supporting the soft landing narrative. The Fed will leave the door open to further rate hikes, but the legacy of past rate hikes and tighter lending conditions will restrain activity and dampen price pressures, negating the need for further action

| 2.4% |

2Q annualised GDP growth |

Not too hot inflation, not too cold growth

We’ve got a nice combination on the US data front this morning for risk assets. Second-quarter GDP growth is stronger than expected (2.4% vs 1.8% consensus), led by consumer spending and investment with inventories not being as important a growth driver as thought likely. Meanwhile, the core PCE price deflator slowed to 3.8% annualised from 4.9% (consensus 4%). So we’ve got decent growth with slowing inflation while jobless claims fell to 221k from 228k and continuing claims dropping to 1,690k from 1,749k, which have further helped to boost the soft landing narrative. At the same time June durable goods orders jumped 4.7% month-on-month thanks to strong Boeing orders boosting civilian aircraft orders by 69.4%. Non-defense capital goods orders ex aircraft remain subdued though at 0.2% MoM – a little better than expected, but there were downward revisions.

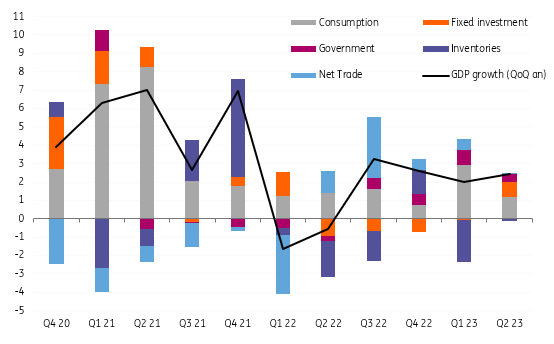

Contributions to US quarterly annualised GDP growth (%)

Focusing on GDP, the 1.6% gain in consumer spending was slower than the warm-weather-boosted 4.2% surge in the first quarter, but it was better than the 1% figure we expected to see and points to some upward revision to the monthly profile in tomorrow’s personal income and spending report. Fixed investment was also better than predicted, rising 4.9%, led by a 10.8% jump in equipment and software investment after a couple of negative quarters. Government expenditure was also robust, rising 2.6%. The main drags were inventories, which weren’t rebuilt as much as expected while net trade was disappointing, subtracting 0.12 percentage points from headline growth with exports plunging 10.8% and imports falling 7.8%.

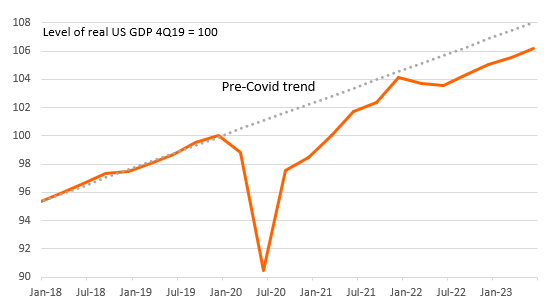

GDP continues to run below pre-Covid trend

GDP below pre-Covid trend, suggesting inflation still largely a supply side story

If we look at the levels of GDP we see that while today’s growth number was better than expected, output is still around 2 percentage points below where we would have been had the economy remained on its pre-pandemic track. This suggests that supply side constraints continue to have an important legacy impact on inflation and additional rate hikes to dampen growth and get inflation sustainably back to target are not necessary. This view gets some support from that lower-than-expected core PCE deflator which at 3.8% annualised is the slowest rate of price increase since the first quarter of 2021. The headline PCE deflator slowed to 2.6% annualised.

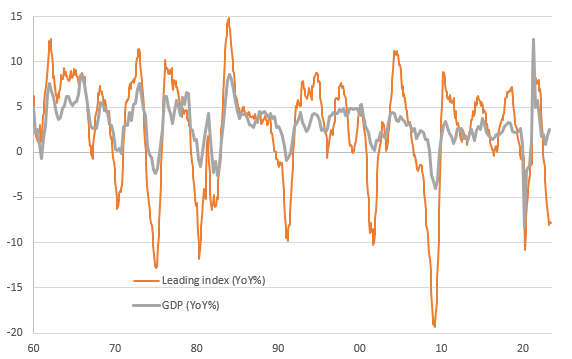

Leading indicators still point to downside risk for GDP growth

Recessions risks linger on

In terms of the outlook, we remain concerned that the cumulative effect of tighter monetary policy plus tighter lending conditions will increasingly restrain economic activity and growth will slow and possibly contract from the fourth quarter. Certainly the leading economic indicator suggests that the risks are skewed to the downside for economic activity. This should result in weaker employment numbers through the second half of this year and into 2024, which will further dampen price pressures, As such, we continue to believe that while the Fed will leave the door open to further interest rate hikes, there is less urgency to do so and that yesterday’s rate hike to 5.25-5.5% will end up marking the peak for US interest rates.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article