Gold Monthly: US rate cut drives gold rally

The highly awaited US interest rate cut finally materialised in September driving gold prices to a new record. We believe the bullish macro picture combined with safe-haven demand amid an escalation of tensions in the Middle East and the ongoing war in Ukraine will drive gold to new highs

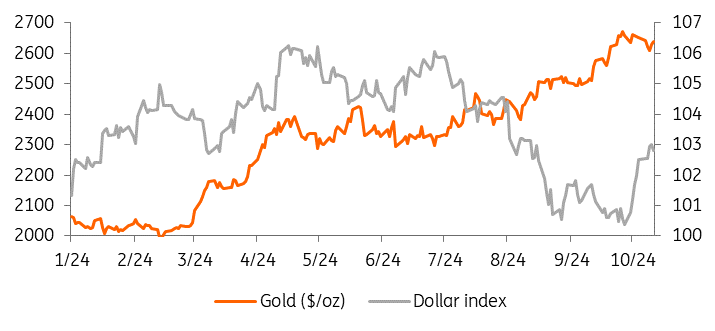

Gold surges to new highs amid Fed rate cut, Middle East tensions

Gold has been one of the best performers among major commodities this year. It has surged more than 28% year-to-date, hitting a series of records on the way, supported by rate-cut optimism, strong central bank buying and robust Asian purchases. Safe-haven demand amid heightened geopolitical risks as well as uncertainty ahead of the US election in November has also supported gold’s record-breaking rally this year.

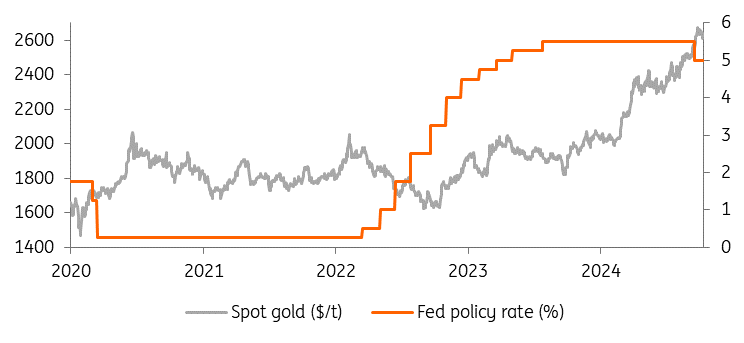

US rate cut boosts gold

The US Federal Reserve implemented its highly-awaited interest rate cut on 1 September, its first since March 2020, clipping rates by 50bp, and providing a tailwind to gold prices.

Lower borrowing costs are positive for gold as the metal doesn’t pay interest. The Fed had held its key policy rate in a target range of 5.25% to 5.5% – the highest level in more than two decades – since last July.

The question for the gold market now is the pace at which the Fed will ease its policy after hotter-than-expected inflation and a slowdown in the labour market.

Our US economist’s base case remains 25bp rate cuts in November and December.

Lower borrowing costs are positive for gold

ETFs see more inflows

Global physically-backed gold ETFs saw their fifth consecutive month of net inflows in September, attracting $1.4 billion, according to the latest data from the World Gold Council (WGC). The gain was driven by North America, while Europe was the only region that saw net outflows.

Investor holdings in gold ETFs generally rise when gold prices gain, and vice versa. However, gold ETF holdings have been in decline for much of 2024, while spot gold prices have hit new highs. ETF flows finally turned positive in May.

ETF holdings have been rising since May

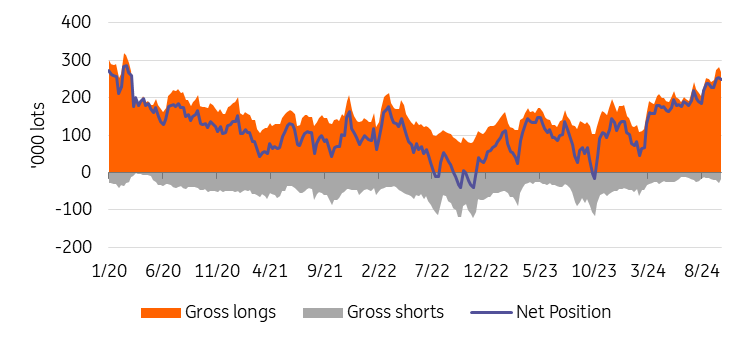

COMEX futures net long rise further

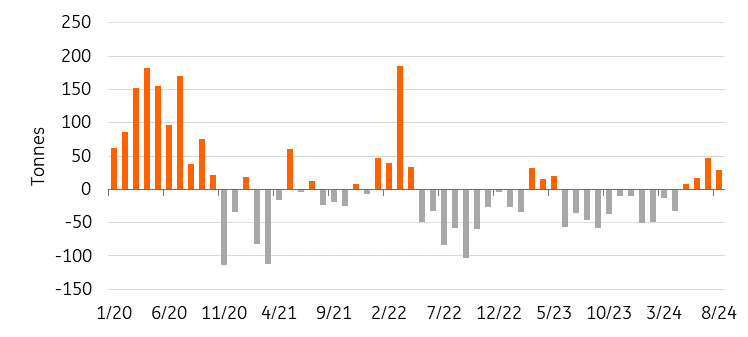

Central bank demand slows

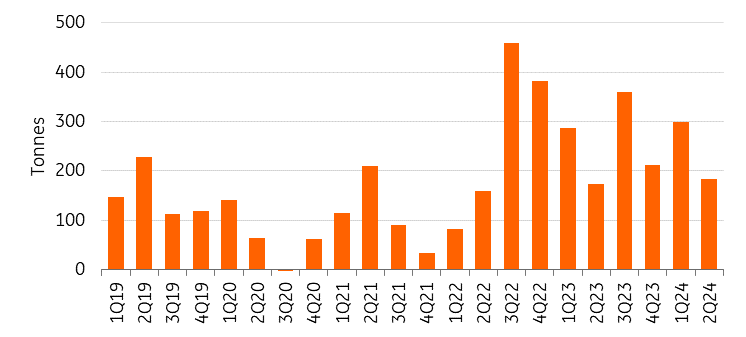

Central banks continued to accumulate gold in August, however at a slower pace, reporting net purchases of 8 tonnes – the lowest since March, according to data from the WGC. The National Bank of Poland was the leading buyer in the month, followed by the Central Bank of Turkey and the Reserve Bank of India. Meanwhile, the Central Bank of Kazakhstan reduced its gold holdings by 5 tonnes in August.

Meanwhile, the People’s Bank of China (PBoC) didn’t add gold to its reserves for the fifth straight month in September. Bullion held by the PBoC was unchanged at 72.8 million troy ounces at the end of last month, according to official data. China has seen a slowdown in gold purchases over recent months. China’s central bank ended an 18-month buying spree in May that had driven gold prices to all-time highs, with these record-high prices likely deterring further purchases for now.

In 2023, central banks added 1,037 tonnes of gold – the second-highest annual purchase in history – following a record high of 1,082 tonnes in 2022. Looking ahead, we expect central bank demand to remain strong amid the current economic climate and geopolitical tensions.

August’s central banks gold purchases the lowest since March

Gold’s rally not over yet

The bullish macro picture combined with safe-haven demand amid an escalation of tensions in the Middle East and the ongoing war in Ukraine will drive gold to new highs. The US presidential election in November will also continue to add to gold’s upward momentum through to the end of the year, in our view, and is likely to perform well regardless of the election outcome. Central banks are also expected to keep adding to their holdings, which should offer support.

We see prices averaging $2,580 in the fourth quarter, with an annual average of $2,388. Gold’s upward momentum will continue next year with 2025 prices averaging $2,700.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article