Gold Monthly: $3,000 is now in sight

Gold is already up more than 9% year-to-date, having hit a series of consecutive record highs along the way. Here's why we think gold at $3,000/oz is within reach

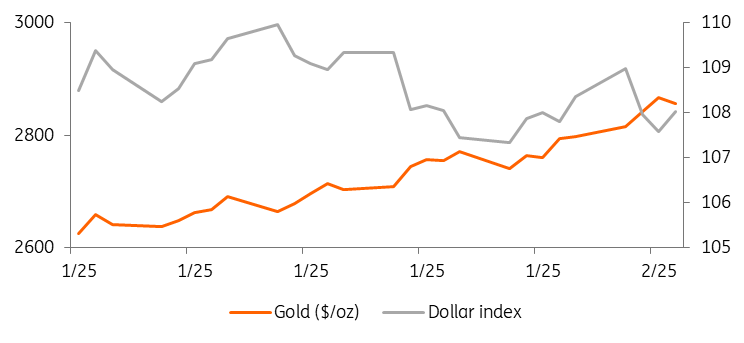

Gold is already up 9% this year

Trump spurs haven demand

It is only February, and gold has already hit a series of fresh record highs this year. Tariff concerns that risk higher inflation and slower economic growth are spurring demand for safe haven assets like gold.

Tariffs on Canada and Mexico have been delayed by a month, but 10% tariffs on China went ahead. Beijing retaliated immediately by imposing a range of tariffs on US products.

Despite the US coming to a deal with Canada and Mexico, the uncertainty over trade and tariffs will continue to buoy gold prices. If trade tensions intensify and we see more retaliatory measures, safe haven demand for gold will continue.

US President Donald Trump's latest comments suggesting that the US takes over the Gaza strip and assumes responsibility for reconstructing the territory have added to this uncertainty, further boosting gold prices.

With Trump back in the White House, uncertainty and unpredictability are running high. And gold will continue to benefit from this environment.

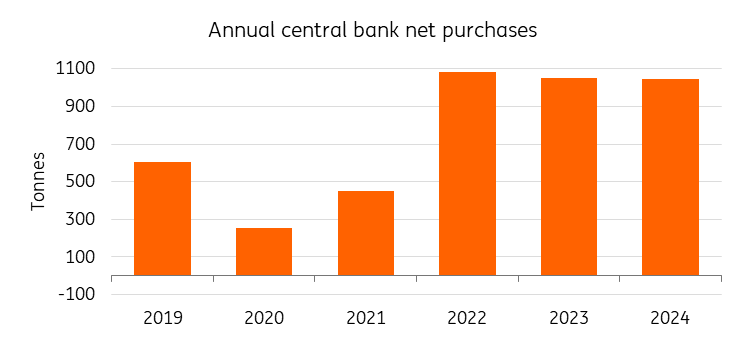

Central banks are still bullion hungry

Gold’s rally in 2024 was driven by central bank buying, especially from China. Central banks are still buying and will probably continue to do so as geopolitical tensions and the economic climate continue to push them to increase their allocation towards safe haven assets.

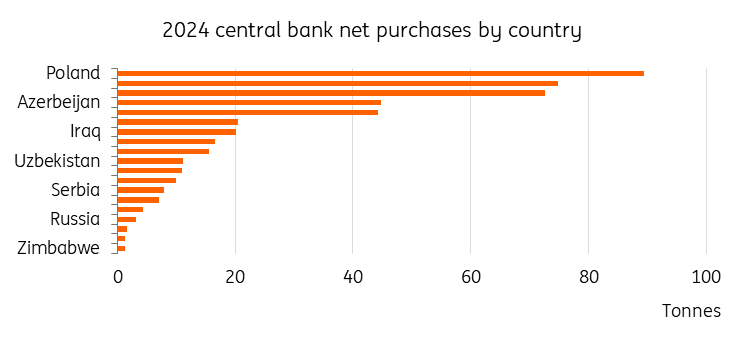

Last year, central banks buying exceeded 1,000 tonnes for the third year in a row, accelerating sharply in the fourth quarter to 333 tonnes, bringing the net annual total to 1,045 tonnes, according to the latest data from the World Gold Council. The National Bank of Poland led the charge, adding 90 tonnes to its gold reserves last year, but demand was seen from a broad range of emerging market banks.

Central banks’ healthy appetite for gold is also driven by concerns from countries about Russian-style sanctions on their foreign assets in the wake of decisions made by the US and Europe to freeze Russian assets, as well as shifting strategies on currency reserves. Looking ahead, we expect central banks to remain buyers.

Central banks demand tops 1,000t for the third year in a row

Central banks’ appetite for gold likely to continue in 2025

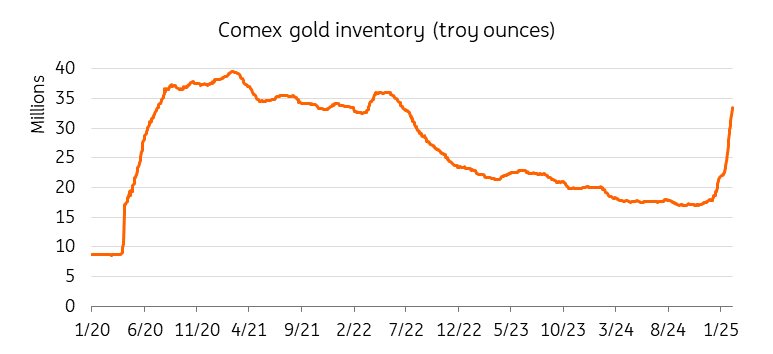

Meanwhile, soaring gold stockpiles in America could further boost gold prices. Following Trump’s election win in November, Comex gold inventories surged to their highest level since 2022. Tariff fears and a profitable arbitrage – after gold prices on Comex moved to a premium over international prices in December – have caused a rush of gold to fly into New York. Gold’s exports to the US from Europe’s main refining hub in Switzerland have also jumped to the highest level since Russia’s invasion of Ukraine.

While the US president hasn’t specifically targeted gold in his tariff threats, traders have been concerned that gold could be included in potential blanket tariffs he has threatened to impose.

If tariffs on gold are applied, this would lead to higher and more volatile gold prices in the US and a potential reshuffle of trade routes. The US is reliant on imports of gold from both Mexico and Canada. In 2024, Mexico accounted for around 30% of US imports of gold, and Canada for around 15%.

This surge in demand from the US could provide a further boost for gold prices.

Trump sparks a huge gold rush

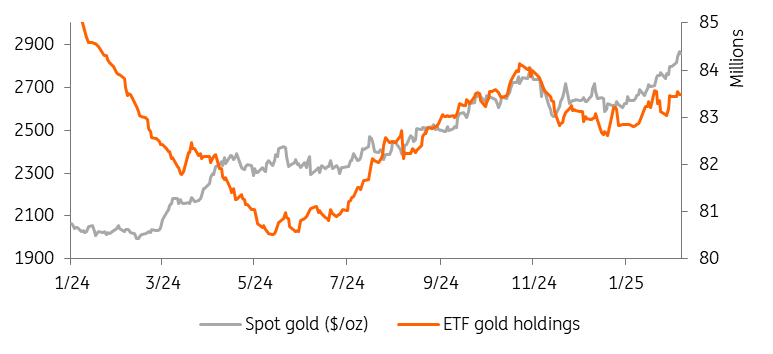

ETFs are ticking higher

Investor holdings in gold ETFs generally rise when gold prices gain, and vice versa. Global holdings in gold ETFs were effectively flat in the fourth quarter and ended the year very close to where they had started even as gold prices surged 27%. However, ETF holdings have been ticking higher over the past couple of sessions. If we see more additions, perhaps driven by geopolitical uncertainty, optimism about further US rate cuts and/or a stronger gold performance, this would give bullion prices a further tailwind.

More ETF flows would give gold prices further boost

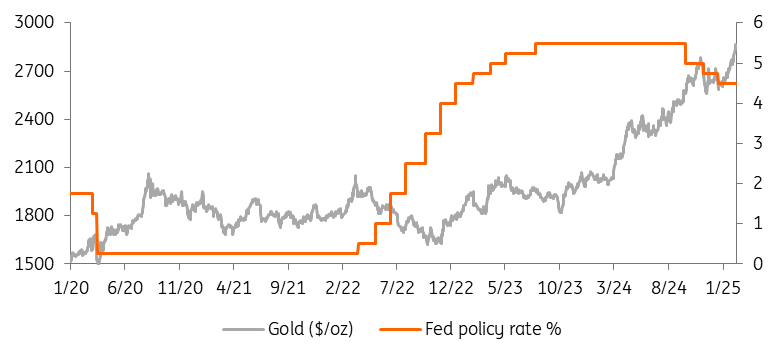

US Fed cuts will boost gold

The main question for the gold market now is the pace at which the Federal Reserve will ease its policy. Lower borrowing costs are positive for gold as the metal doesn’t pay interest. After 100bp of interest rate cuts in the latter part of 2024, the Fed held policy steady in January and suggested it was in no hurry to cut again. The recent developments surrounding tariffs are likely to keep it that way through the first half of 2025, our US economist believes.

If the central bank is forced to maintain higher rates for longer, this could undermine gold’s appeal.

However, the central bank will still ease its policy over the course of the year, even if its path to easing is slower than previously expected. Our US economist now expects the Fed to cut rates twice in the second half of this year. What happens next is highly uncertain, but assuming a gradual de-escalation of tensions that sees tariffs being removed, he is forecasting one further rate cut in early 2026.

Lower borrowing costs are positive for gold

We believe gold will hit more record highs this year, with $3,000/z now in sight. The macro backdrop will remain favourable for gold as interest rates decline and foreign reserve diversification continues amid geopolitical tensions. A stronger USD and tighter monetary policy could eventually provide some headwinds to gold. However, increased trade friction could add to gold’s haven appeal. We see gold averaging $2,800/oz in the first quarter with prices likely to reach the $3,000/oz level this quarter. We see an average of $2,760/oz in 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article