Gold enters bear territory

- 27 September 2022

- Commodities, Food & Agri

US dollar strength and central bank tightening have weighed heavily on the gold market. And with further tightening expected there is room for more downside in the near term. However, the medium-term outlook is more constructive

USD strength and rising yields hits investor demand

Given the amount of uncertainty at the moment coupled with high inflation, many in the market may have thought gold prices should be well supported. However, this has not been the case. Spot gold is trading at its lowest levels in more than two years and has fallen more than 20% from its recent peak in March, pushing it into a bear market.

The dominance of the US dollar has hit sentiment across the commodities complex and gold has not been spared in this move. The USD index has surged to a 20-year high. This strength is largely a result of the aggressive stance the US Federal Reserve has taken in terms of monetary tightening in order to fight inflation. And with inflation proving to be stickier than anticipated, the Fed is expected to be even more hawkish than originally thought for the remainder of the year. Our US economist is of the view that we will see a further 75bp hike in November and a minimum of 50bp in December, which would leave the target range at 4.25-4.5%.

Despite sticky inflation, real yields have also been climbing. 10-year real US yields have reached their highest levels in more than a decade and are firmly back in positive territory. Given the strong negative correlation between gold prices and real yields, it is not surprising to see that gold has struggled in this rising yield environment.

Higher yields increase the opportunity cost of holding gold, which appears to be turning investors off the yellow metal. Total known exchange-traded fund (ETF) holdings in gold have declined by almost 9% since April to stand at around 97.9m oz – levels we last saw back in January. Data from the World Gold Council shows that over August, ETF outflows amounted to 51 tonnes, which is the fourth consecutive month of net outflows. And it is pretty clear that the market is set to see further outflows in September.

Speculative positioning in COMEX gold is no better with speculators holding a net short position. The net short stands at 32,966 lots as of 20 September, which is the largest short speculators have held since late 2018. From a pure positioning point of view, speculators still have room to increase this short. Back in late 2018, the net short in COMEX gold was in excess of 100k lots.

Weak investor interest in gold as yields surge

Central banks keep adding to gold reserves

So far this year central banks have continued to increase gold reserves. During these times of uncertainty (both economic and geopolitical) and high inflation, banks appear to be turning to gold as a store of value. In addition, some central banks may have been concerned about the freezing of Russia’s central bank foreign reserves following its invasion of Ukraine. This action is likely to have left some central banks uneasy, and so looking to diversify into gold. The latest numbers from the World Gold Council show that central bank holdings over 2Q22 increased by almost 180 tonnes (although still down 14% year-on-year). Whilst for July, central bank buying amounted to 37 tonnes over the month. Given the current environment is likely to persist, central banks are likely to continue to add to their gold holdings in the months ahead.

Chinese gold demand picks up

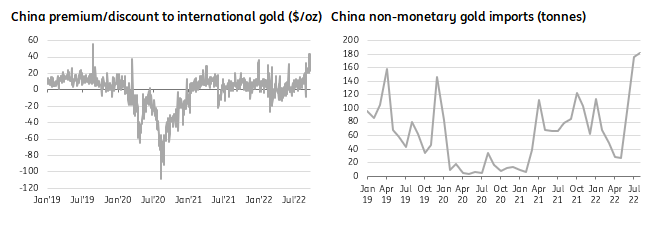

Chinese gold demand suffered earlier in the year due to the Covid-related lockdowns, particularly over 2Q22, which is when strict restrictions were in place across Shanghai and Beijing. According to WGC data, Chinese consumer demand was down 23% YoY over 1H22. However, the premium in local Chinese gold prices compared to international prices has grown more recently, suggesting that we are seeing stronger domestic demand coming through. Import data appears to back this up, with non-monetary gold imports hitting more than a four-year high in August and up 134% YoY.

Meanwhile, another key gold consumer, India, is expected to see stronger gold demand as we head towards Diwali in late October.

However, whilst we may see stronger consumer demand, it is clear that price direction is driven by investment flows. And the outlook for this is less constructive in the short term.

China gold imports surge

Eventual signs of Fed easing will lift prices

While in the short term we suspect gold prices will remain under pressure due to monetary tightening, we will need to keep an eye on signals from the Fed. Any hints of an easing in its aggressive hiking cycle should start to provide some support to gold prices. And in order for this to happen we would likely need to see some clear signs of a significant decline in inflation. We should see inflation coming off quite drastically over 2023 and this will then open the door for the Fed to start cutting rates over 2H23, our US economist believes. This differs from the Fed’s dot plot, which implies higher rates as we move through 2023. However, under the assumption that we see easing over 2H23, we expect gold prices to move higher over the course of 2023.

Obviously, the key risk to this view is if inflation turns out to be even stickier than expected, which would require a longer tightening cycle from the US Fed.

In addition, the inverted yield curve will raise worries over a looming recession. And these concerns might see some investors seeking safe haven assets, such as gold. Although in the short term, rising rates will likely counter this to a certain degree.

ING gold price forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more