Global de-dollarisation takes a pause, embattled euro gives room for Asian FX

The latest data suggest that the dollar didn’t lose ground last year, unlike the euro which took a hit. This led to some rebalancing in favour of Asian currencies. Meanwhile, the yuan is facing challenges as a reserve currency, but is making progress as a currency of transactions

In this global de-dollarisation update we take a look at the most recent trends in the FX structure of global assets, liabilities, and transactions. In our view, the data provided by IMF, BIS, SWIFT, and major central banks are pointing at several developments:

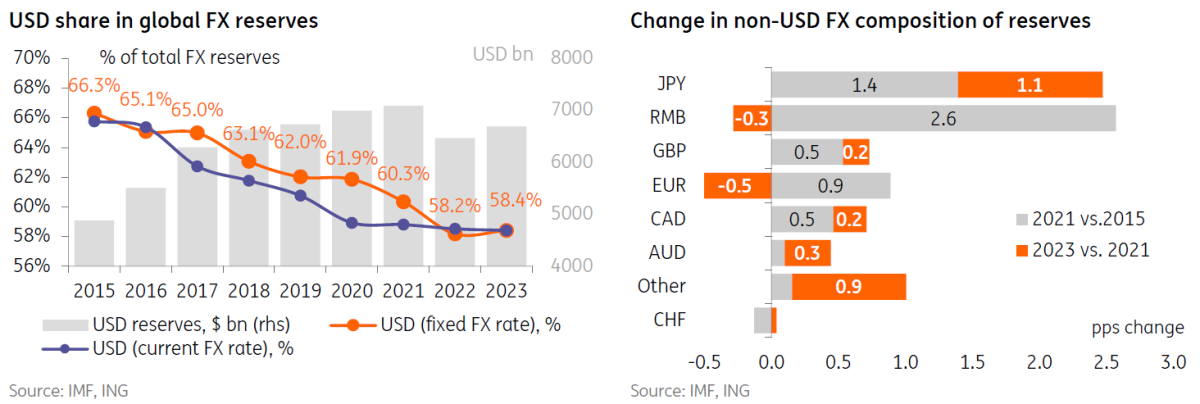

- De-dollarisation of global central bank reserves took a pause. Adjusted for the FX revaluation effects, the share of USD in allocated reserves increased 0.2ppt to 58.4% in 2023, which is a first increase since 2015. This took place amid a 0.9ppt drop in the EUR share to 20.0%. The biggest gainer was JPY with a 0.6ppt jump to 5.7%. Surprisingly, RMB posted a second annual decline in a row to 2.3%.

- Private sector remains true to the dollar. USD accounts for a steady 49-50% of foreign assets of the non-financial private sector; JPY is holding at 5%, vs. 11% for 'other currencies', including RMB. The foreign liabilities side is showing a similar picture to assets (USD c.45%), while the share of USD in international debt securities is more or less stable at around 40%.

- US dollar retains dominance in global transactions, Asian currencies see increased presence. Big movements in the USD and EUR shares in SWIFT in 2023 were largely due to changes in methodology, but the long-term trend still seems more favourable for USD. On the regional level, despite the recent decline in RMB's share in global trade finance market and lower geographical diversification of offshore usage, RMB keeps building up a mass in SWIFT while keeping the growth of its own CIPS system. Meanwhile, similar to other areas, RMB is not alone, with SGD and JPY also gaining share.

Global roles of USD, RMB, JPY

USD is holding its ground, while EUR is losing to other traditional reserve currencies

Assets – central banks still like the dollar, and move away from euro

The recently released IMF COFER data finalises the picture for 2023 in terms of global central banks' preferences when it comes to reserve currencies. Although the headline numbers didn't show any major shifts in the currency structure of the allocated reserves, these have to be adjusted for the exchange rate movements, mainly the 2.1% weakening of the USD vs. major currencies in 2023. Given that all reserves in the survey are reported in USD, exchange rate fluctuations may somewhat distort the actual trends in FX preferences. If we treat the entire historical data set as if the global exchange rates were fixed at their end-2023 levels, it turns out that the share of the US dollar in allocated reserves gained 0.2ppt to 58.4% last year, which is a modest but first annual increase since 2015. In addition, USD holdings gained $227bn in physical terms. While it is too soon to make strong calls about the end of the de-dollarisation trend, it would be safe to assume that it took a pause in 2023.

In 2023, the US increased its share of allocated reserves, whereas the euro and Chinese yuan lost share

Another interesting observation concerns the other currencies in the mix. Euro seems to be the biggest loser, with its share dropping to 20.0%, or 0.9ppt lower than in 2022 and 0.5ppt lower than two years ago. Sterling also lost 0.3ppt. Meanwhile, this has helped only the traditional reserve currencies. The biggest winner was JPY, which gained 0.6ppt (and 1.1ppt in two years) to 5.7%, while the developed/commodity currencies AUD and CAD also gained slightly. In a way, this suggests some rebalancing of holdings among the seasoned players amid the normalisation of interest rates.

The Chinese yuan, on the contrary, which emerged as a reserve currency only recently and gained 2.6% share over 2015-2021 period, lost share in 2022-23. This is partially explained by Russia, which used to account for around one-third of global international RMB reserves before 2022, and which had to spend some of it RMB holdings to finance the budget deficit. Also, those numbers suggest that the process of global reserves yuanisation may have slowed outside of Russia as well. However, we have to note that the IMF COFER data covers 149 out of total of 195 countries and may somewhat underestimate the actual usage of RMB given its growing popularity among frontier countries.

FX structure of central bank reserves

Adjusted for FX revaluation effect, USD stopped losing share in global reserves amid the decline of EUR, but RMB is not taking advantage of that, unlike JPY and other traditional reserve currencies

An important question which always arises when looking at the international reserves is whether a shift in the FX preferences is somehow related to the increased popularity of gold, which has led to another price rally. Central banks have ramped up gold buying compared to 2022, and it is visible through various metrics – from the change in net demand for gold from the central bank recently mentioned by our commodity strategists (see the link to the right) to the level of the official gold reserves reported by the IMF. While the exact gold reserve growth numbers for 2023 may vary depending on the indicator and the methodology used, we can safely assume that this increased demand is there and is related to a recovery in the appetite for the overall increase in the central banks' international assets after a brief period of spending in 2022.

Central banks ramped up their gold buying in 2023 compared to 2022

Meanwhile, looking at the IMF IFS data, we see few signs that gold is significantly more popular than the fiat currencies. Although the headline share of gold increased from 14.4% to 15.9% of total international reserves over 2023, this entire increase was due to revaluation effect. Assuming a fixed gold price of end-2023, the share of gold didn't change over 2023. Looking further back, it seems that the central banks have been showing a relatively stable preference for gold in the last decade. In practice, that means that the physical purchases of gold have been just enough to catch up with the foreign currency portion. So far, this suggests little evidence that recent gold buying from the central bank community represents a new chapter in the de-dollarisation story.

Gold reserves, as a share of total

Despite the ongoing gold purchases, the overall structure of reserves is not moving away from fiat currencies

Private asset holders seem to be even more conservative than the central banks. Looking at the BIS locational banking statistics (available through 3Q23), the dollar remains the primary currency in terms of foreign assets, even slightly gaining share from 49% to 50% among non-banking holders, but generally showing no material change from the situation of the previous years. The FX structure of global private foreign assets has been quite stable in the recent decade. Importantly, given the abovementioned development in Asia, it's worth mentioning that JPY accounts for around 5% of global foreign assets held by non-banks, while RMB is included into the 'other currencies' pool, which has been holding a steady 11% share since 2017.

FX structure of foreign assets ex. CB reserves

USD accounts for a steady 50% of non-financial sector assets; JPY is holding 5%, 'other currencies', including RMB, have been stable at 11% since 2017 (not shown on the picture)

Liabilities, similar to assets, are USD-focused, but show more variety

The foreign liabilities side is generally a mirror image of the assets, especially when it comes to the preference for the US dollar. As of the end of 3Q23, 53% of non-bank foreign liabilities were denominated in USD, which is a 2ppt increase compared to 2022 and is close to the decade high. Meanwhile, it is worth mentioning that the non-dollar portion of the foreign liabilities side, especially among the non-financials, is much more diversified than the assets. For example, the share of euro in liabilities is much modest – at 21% vs. 29% of non-financials' assets, while JPY accounts for only 1% vs. 5%, and 'other currencies' are 22% of liabilities vs. 11% of assets. That said, it does not represent any material change compared to the previous years, therefore not suggesting any recent changes in the trend.

Looking at the FX structure of international debt securities, the recent BIS data showed around a 1ppt decline in the overall USD share to 41% in 2023, however that is explained mainly by the exchange rate effects. Overall, the currency structure of that market has been relatively stable since 2018, with euro accounting for 10-11%, and other currencies 27-28%.

FX structure of foreign liabilities

Liabilities side is showing a similar picture to assets (USD c.50% among non-financials), while the share of USD in debt securities is stable around 40%

Transactions – USD is popular globally, but regional diversification is growing

The global data regarding the FX structure of transactions is also suggesting that the US dollar didn't lose ground in 2023. Here the international SWIFT system with its over 11,000 participants and over $400bn in daily transaction volume and monthly disclosures remains the primary data source. One important caveat for the 2023 data is that there has been a change in methodology which led to the exclusion of a large portion of non-transaction financial messages done by European central banks. This has led to a material drop in the previously inflated share of the euro in transactions. Therefore, both the 14ppt decline in the EUR share to the 22-23% level, the 6ppt increase in the share of USD to 46-47%, and the increase in the shares of 'other currencies' should be taken with a pinch of salt. Nevertheless, the overall picture suggest that the US dollar at least didn't lose its dominant position in transactions, in line with the decade-long trend.

The US dollar has not lost its dominant position in transactions

Another general observation from the SWIFT data, is that despite the stable and high role of the US dollar, diversification is taking place at the regional level and is focused primarily on the Asian currencies. RMB has gained the most in 2023, showing a 2ppt (or 1.3ppt net of the effect of changed methodology) increase in the share to 4.0% in the last year. Meanwhile, the Chinese yuan is not the only winner: Singapore dollar gained 1ppt (0.7ppt net of the methodology shift), while JPY's share increased 1ppt (or by 0.3ppt net of the shift). The change in other major currencies, including GBP, CHF, CAD, AUD adjusted for the changed methodology was, in our estimates, negative. Finally, the group of less common currencies also posted a sizable gain of 2.2ppt (including a statistical boost of 1.4ppt). In a sense, apart from the growth in the role of JPY in transactions, which perhaps requires further investigation, this suggests a divergence in the trends between transactions and assets and hints at some diversification in trade at least at the regional level.

One illustration of this diversificaion would be the wider usage of non-traditional reserve currencies, such as AED, following the expansion of BRICS (see our review of the results of the August 2023 summit on the right). Moreover, the anecdotal evidence from Turkey, which according to Bloomberg saw an increase of transactions in AED (in addition to RMB and other currencies), suggests that diversification of trade is taking place not just due to BRICS. We do not exlude, that the noticeable rise of below-the-radar currencies in the SWIFT data (with shares below 0.3%) seen in 2023 may reflect this trend. This raises the question of whether higher diversification of transactions will inevitably lead in higher variety in assets and liabilities, but the answer is not strraightforward, in our view. On the one hand, higher usage of new currency in trade may prompt a shift in other areas, but on the other hand, longer-term holding of a currency has different requirements in terms of instututional framework.

FX structure of transactions

EUR lost share in SWIFT in 2023 largely due to changes in methodology, but the long-term trend is still favourable for USD; Asian currencies are gaining at the regional level

In the yuan-specific portion of the SWIFT data, we note that in the recent months the role of RMB on the trade finance, that has been growing since 2Q22, has somewhat moderated, returning to 3.8% as of February 2024, a level last seen in 3Q22. It has yet to be seen if that represents a reversal in the trend and what stands behind it, but the picture here seems to correlate somewhat with the rapid growth in Russia-China trade in 2022-23 and some signs of delays in Russia-related transactions by the Chinese banks reported in the beginning of this year.

Another interesting observation is that the diversification of the offshore CNY usage somewhat declined in 2023. Between July 2022 and September 2023 Russia had a noticeable 2-4% share on the global CNY market, but since 4Q23 it disappeared again, helping to restore Hong-Kong's pre-2022 80% share on the global CNY market.

FX structure of trade finance and geography of offshore usage of RMB

USD is regaining ground in the trade finance market, while geographical diversity of CNY users has moderated back to pre-2022 levels

The challenges faced by RMB in terms of global reserves and certain segments of transactions do not mean that the topic of yuanisation is off the agenda. The global presence of the yuan keeps being promoted and expanded through various channels. First, the People's Bank of China (PBOC) keeps widening the network of bilateral swap lines, the most recent addition being the RMB50bn facility with Saudi Arabia signed at the end of 2023. That said, the widening in the swap line has somewhat slowed, and the news about Argentina reportedly utilising the swap lines with PBOC in order to ultimately procure USD may suggest that this internationalisation tool may be used only cautiously.

Second, China's CIPS, the RMB-based financial messaging system, keeps growing rapidly. According to the most recent report published by the PBOC, it appears that in 9M23 the number of daily messages was 35% higher than in the entire 2022, while the daily volume of transactions jumped by approximately 30% to around RMB500bn. By comparison to SWIFT, CIPS is 10-15% in terms of participant number, 15-20% in terms of total transaction value, and a much smaller fraction in terms of number of messages, but it is important to keep in mind that CIPS is so far growing steadily from a low base, and is gaining ground as a regional competitor. Overall, it appears that China's expanding trade ties and financial infrastructure suggest that the potential for further yuanisation has not been exhausted.

Global role of RMB

RMB is still being promoted as the regional currency through swap lines and CIPS transaction platform

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article