Germany’s latest fiscal reform poses obstacles for the housing market’s recovery

By the end of 2024, German house prices were around 11% below their peak in the second quarter of 2022. Looking ahead, the recent increase in bond yields is expected to slow the housing market’s recovery

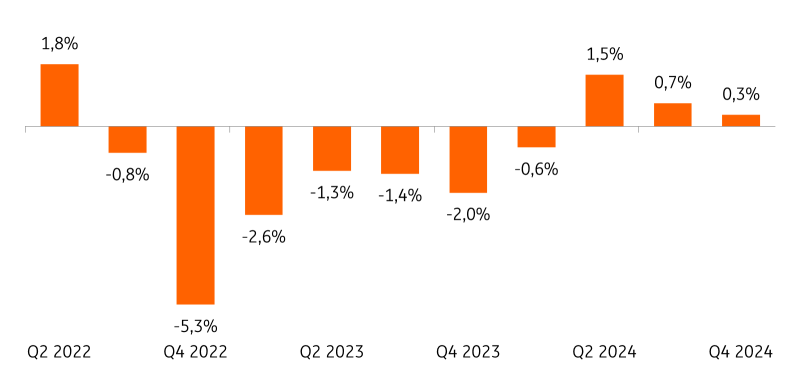

The 2024 house price slump masks evidence of tentative recovery

German house prices dropped by 1.6% in 2024, according to the just-released house price index from the German Statistical Office. This is the first time since the years 2006 and 2007 that house prices have fallen for two consecutive years. However, the overall drop in prices conceals the gradual recovery of the housing market that began early last year, largely driven by improved affordability.

House price index (%QoQ)

The current recovery is more of a marathon than a sprint, with its fair share of ups and downs. In the fourth quarter of 2024, house prices increased by 0.3% quarter-on-quarter, down from 0.7% in the third quarter, and remain significantly below their peak levels.

Last year's tailwinds are fading

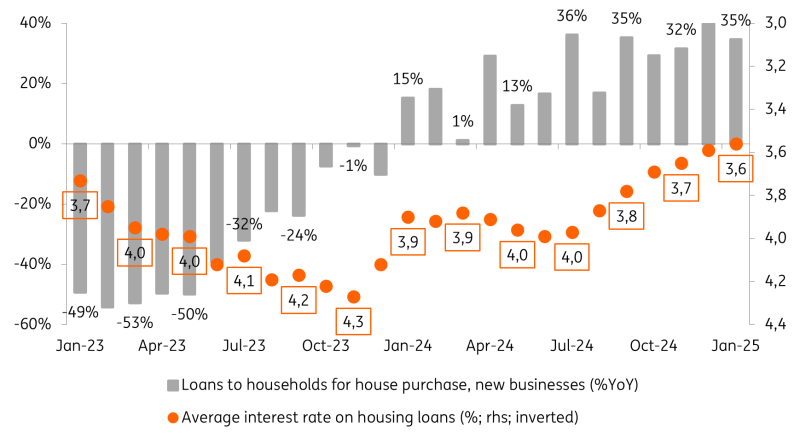

Last year, mortgage interest rates consistently declined, dropping from 4.1% in December 2023 to 3.6% by the end of 2024, reaching their lowest point in two years. Additionally, German real wages increased by 3.1%, the fastest growth rate since the series began in 2008.

These factors combined to enhance affordability, thereby increasing demand for housing loans. Consequently, the volume of new mortgage lending rose by more than 20% year-on-year in 2024.

Average mortgage rates and demand for housing loans

The positive trend in demand has continued this year. However, looking ahead, factors that positively impacted affordability last year look set to turn into headwinds.

After the German government's landmark decision to reform the debt brake to boost defence spending and the planned €500bn special fund for infrastructure investments, capital market interest rates have surged. This increase is driven both by rising expectations of government debt and improving growth prospects.

At the end of February, the German 10yr government bond yield stood at 2.39%. In early March, it jumped by 50 basis points in a single day in reaction to the new fiscal reality and has fluctuated around this elevated level since then. In the short-term, volatility looks set to remain high given the various forces at play and the high level of uncertainty. Looking further ahead, there is more upward than downward potential for longer-term government bond yields.

Due to the strong correlation between longer-term capital market interest rates and mortgage interest rates, interest rates on loans to households for house purchase could well continue to rise. Furthermore, wage growth is expected to slow as a result of the turning labour market. With house prices still climbing, there's little to suggest a significant improvement in affordability.

In short, whatever provided a tailwind to the housing market recovery over the past year is now being reversed.

Germany's new fiscal reality creates short-term challenges and long-term hopes

On a more positive note, consumer confidence should improve given recent political developments in Germany. As a result, the willingness to spend, currently at extremely low levels, could increase while the propensity to save could decrease from its record highs. However, near-term developments in the housing market will largely depend on whether improved consumer sentiment can compensate for increased financing costs.

In the long term, the key factor supporting the housing market recovery will be the successful implementation of the announced investment package.

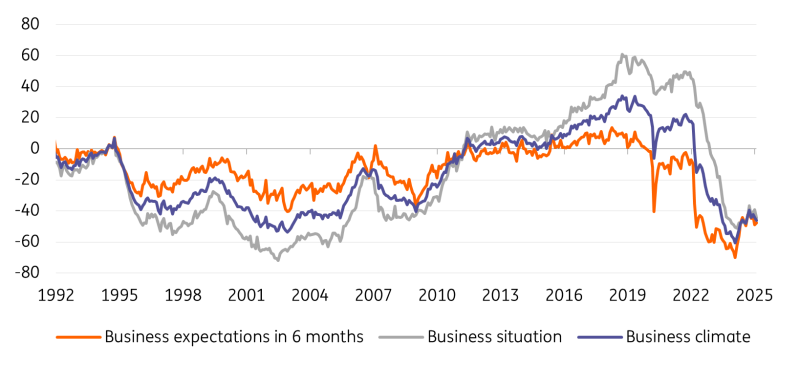

Increased investment in infrastructure will impact the construction industry, aggravating the shortage of skilled workers and potentially pushing up costs and prices. Plans by CDU/CSU and SPD to speed up procedures and simplify standards in order to promote residential construction could bring some relief. Thus, following the downturn at the beginning of the year, sentiment is likely to improve in the residential construction sector.

Business climate in the residential construction sector (net balance)

However, it will take well into the second half of the year before any measures are actually implemented and, most importantly, take effect. As a result, the housing market is likely to benefit from a short-term boost in sentiment. Looking beyond the short term, higher financing and construction costs will continue to weigh on the housing market.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article