Germany: Unprepared for a perfect storm

Recession has become our base case but there is more: the economy is facing its biggest overhaul in decades

At the start of the year, we predicted a strong cyclical rebound for the German economy over the course of 2022. Richly filled order books, relief in global supply chains and big investment plans by the German government were just a few of the ingredients in this forecast. But the war in Ukraine has changed everything. What German Chancellor Olaf Scholz had called a ‘Zeitenwende’ (a historic turning point) for geopolitics and military spending, has actually become a ‘Zeitenwende’ for the entire German economy. For several decades, the German economy has benefited from importing cheap energy and globalisation. It now no longer will.

Recession is hard to avoid

The latest hard macro data has confirmed our concern that the economy might already have contracted in the second quarter of the year. Admittedly, this is only data up to May but almost all of the data is down compared with the first quarter. If it weren't for still relatively strong business sentiment and a particularly solid current assessment, a contraction would have been the consensus view already. At face value, absolute levels of most leading indicators suggest that the German economy should have grown in the second quarter. However, supportive factors for the economy such as post-lockdown reopenings and filled order books have been losing momentum rapidly. Weaker global demand, supply chain frictions, and high inflation denting consumption are hitting the German economy. In fact, consumer confidence is already in clear recession territory and it looks as if the rest of the economy is quickly following suit.

Looking ahead, even if the current holiday mood wants to make us believe that all is well, the outlook for the German economy is anything but rosy. Currently, in the base case scenario with continuing supply chain frictions, uncertainty and high energy and commodity prices as a result of the ongoing war in Ukraine, the German economy will be pushed into a technical recession. To make matters worse, the current dry weather has reduced water levels in the main rivers close to their 2018 levels, when low water levels led to the disruption of supply chains. All of this makes for a perfect storm in the second half of the year.

Energy dependence biggest vulnerability

Needless to say that currently there are more downside than upside risks to the outlook. The single largest risk is further disruption to Germany’s energy consumption and a complete stop in the Russian gas supply. Currently, Germany’s gas reserves are filled by only around 60%. To get through the winter without any Russian gas, the government intended to have reserves filled up to 90%. This target increasingly looks unachievable. It will not take until the winter before the energy crisis escalates further. The government’s decisions to bail out an energy company and to change the so-called pricing adjustment mechanism, which allows firms to pass on costs to the consumer, as well as the fact that NordStream 1 just went – temporarily – offline, are just a few of the dark clouds gathering. In case of a complete shut-off from Russian oil and gas, available studies suggest that the German economy could shrink by between 2% and 10% - a very wide range as assumptions in these model estimates differ significantly.

Germany's economic 'Zeitenwende'

The perfect storm in the coming quarters is not where the ‘Zeitenwende’ for the German economy will stop. In fact, we have often written about the need for more investment and structural changes. The war in Ukraine is the mother of all reasons for significant structural change. Actually, the war in Ukraine puts an end to the German economic business model as we knew it - a model which was mainly based on cheap energy imports and industrial exports into a increasingly globalised world. Of course, everything is possible but it does not really look as if this world will return any time soon. Instead, Germany needs to reduce its energy dependence and step up the green transition. It also needs to adjust to a world of friendshoring, in which services will increasingly take over from industrial exports. The needs for scaling up investment in education, infrastructure and digitalisation add to a long list of Germany’s economic ‘Zeitenwende’. In this regard, the finance minister’s announcement to return to balanced budgets next year is as surprising as it is unrealistic, and in our view, rather driven by political motives than by economic foresight.

Germany’s track record with structural change is not overly successful, at least not with swift structural reforms. Think of reunification or the labour market reforms of the early 2000s. In the early phases, structural reform almost always comes at an economic cost. The same holds for the current ‘Zeitenwende’. Real disposable incomes of households will suffer, and companies will have increasing difficulty in dealing with the costs of higher energy and commodity prices, putting corporate profit margins under pressure. A loss of economic wealth looks like a logical consequence. However, the upside from structural change is that eventually, Germany will manage to deal with these issues and challenges. At the current juncture, this offers a scarce silver lining. For German industry and the entire economy, the green transition and the need for investment are both a challenge and an opportunity.

Germany will need time and money to manage its economic ‘Zeitenwende’. In the short run, the economy is facing a perfect storm, and a recession looks almost unavoidable. In the longer run, the economy can only return as Europe’s powerhouse if it implements investment and structural change as determined and committed as it demanded from other eurozone countries in the past.

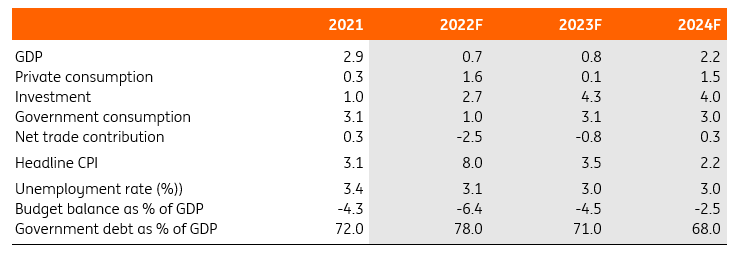

The German economy in a nutshell %YoY

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

12 July 2022

Eurozone Quarterly: This is going to hurt This bundle contains 11 Articles