Germany needs an ‘Agenda 2030’

A stagnating economy, cyclical headwinds and structural challenges bring to mind the early 2000s and call for a new reform agenda

As Mark Twain is reported to have said, “History doesn't repeat itself, but it often rhymes.” Such is the case with the current economic situation in Germany, which looks eerily familiar to that of 20 years ago.

Back then, the country was going through the five stages of grief, or, in an economic context, the five stages of change: denial, anger, bargaining, depression and acceptance. From being called ‘The sick man of the euro’ by The Economist in 1999 and early 2000s (which created an outcry of denial and anger) to endless discussions and TV debates (which revelled in melancholia and self-pity) to an eventual plan for structural reform in 2003 known as the 'Agenda 2010', introduced by then Chancellor Gerhard Schröder. It took several years before international media outlets were actually applauding the new German Wirtschaftswunder in the 2010s.

It's hard to say which stage Germany is in currently. International competitiveness had already deteriorated before the pandemic but this deterioration has clearly gained further momentum in recent years. Supply chain frictions, the war in Ukraine and the energy crisis have exposed the structural weaknesses of Germany’s economic business model, and come on top of already weak digitalisation, crumbling infrastructure and demographic change. These structural challenges are not new but will continue to shape the country’s economic outlook, which is already looking troubled in the near term.

Order books have thinned out since the war in Ukraine started, industrial production is still some 5% below pre-pandemic levels and exports are stuttering. The weaker-than-hoped-for rebound after the reopening in China together with a looming slowdown or even recession in the US, and the delayed impact of higher interest rates on real estate, construction and also the broader economy paint a picture of a stagnating economy. A third straight quarter of contraction can no longer be excluded for the second quarter. Even worse, the second half of the year hardly looks any better. Confidence indicators have worsened and hard data are going nowhere. We continue to expect the German economy to remain at a de facto standstill and to slightly shrink this year before staging a meagre growth rebound in 2024.

Headline inflation to come down after the summer

What gives us some hope is the fact that headline inflation should come down more significantly after the summer. Currently, inflation numbers are still blurred by one-off stimulus measures last year. Come September, headline inflation should start to come down quickly and core inflation should follow suit. While this gives consumers some relief, it will take until year-end at least before real wage growth turns positive again. At the same time, an increase in business insolvencies and a tentative worsening in the labour market could easily dent future wage demands and bring back job security as a first priority for employees and unions. In any case, don’t forget that dropping headline inflation is not the same as actual falling prices. The loss of purchasing power in the last few years has become structural.

Fiscal and monetary austerity will extend economic stagnation

With the economy on the edge of recession, the government’s decision to return to (almost) balanced fiscal budgets next year is a bold move. No doubt, after years of zero and sometimes even negative interest rates, Germany’s interest rate bill is increasing and there are good reasons to stick to fiscal sustainability in a country that will increasingly be affected by demographic change (and its fiscal impact). Nevertheless, the last 20 years have not really been a strong argument for pro-cyclical fiscal policies. With both fiscal and monetary policy becoming much more restrictive, the risk is high that the German stagnation will become unnecessarily long.

Waiting for 'Agenda 2030'

In the early 2000s, the trigger for Germany to move into the final stage of change management, 'acceptance' (and solutions), was record-high unemployment. The structural reforms implemented back then were, therefore, mainly aimed at the labour market. At the current juncture, it is hard to see this single trigger point. In fact, a protracted period of de facto stagnation without a severe recession may reduce the sense of urgency among decision-makers and suggests Germany could be stuck in the stages of denial, anger, bargaining and possibly depression for a long time. Two decades ago, it took almost four years for Germany to go through the five stages of change. We hope this time that history will not be repeated.

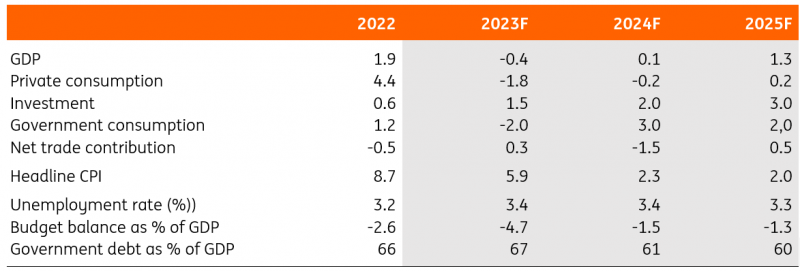

German economy in a nutshell (%YoY)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

12 July 2023

Eurozone Country Update: More accidents on the road to recovery This bundle contains 13 Articles