FXFX Talking

G10 FX Talking: Tighter financial conditions to support the dollar

Tightening financial conditions – especially in the US – create further headwinds to global growth. These conditions look set to support the dollar over the coming months, even if November through December is seasonally a weak period for the dollar. EUR/USD can continue to trade near 1.05 and undervalued commodity currencies can stay undervalued

Main ING G10 FX forecasts

| EUR/USD | USD/JPY | GBP/USD | ||||

| 1M | 1.04 | ↓ | 150 | ↑ | 1.21 | → |

| 3M | 1.06 | → | 148 | ↑ | 1.22 | → |

| 6M | 1.08 | ↑ | 140 | ↓ | 1.23 | ↑ |

| 12M | 1.15 | ↑ | 130 | ↓ | 1.28 | ↑ |

| EUR/GBP | EUR/CHF | USD/CAD | ||||

| 1M | 0.86 | → | 0.95 | ↓ | 1.38 | ↑ |

| 3M | 0.87 | → | 0.95 | → | 1.32 | ↓ |

| 6M | 0.88 | ↑ | 0.95 | → | 1.29 | ↓ |

| 12M | 0.90 | ↑ | 0.97 | ↑ | 1.25 | ↓ |

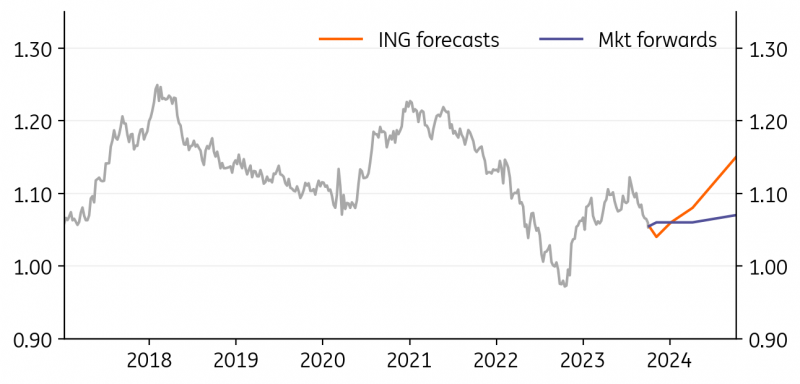

EUR/USD: Dollar could hold gains for a few more months

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/USD

1.0548

|

Mildly Bearish | 1.04 | 1.06 | 1.08 | 1.15 |

- The dollar has been stronger for a lot longer than we were expecting. 4% QoQ annualised US growth in 3Q23, helped by the US consumer, has kept the Fed in hawkish mode. We doubt, however, the Fed will need to hike rates again this year. And given our sub-consensus forecast of 0.2% US growth and a 200bp easing cycle next year, we still look for the dollar to turn lower.

- Typically, November and December are weak months for the dollar. But poor growth in the Eurozone and what could be some political risk premium going back into the euro could keep EUR/USD at these low levels near 1.05 into year-end.

- Even at 1.05, EUR/USD does not looks substantially undervalued

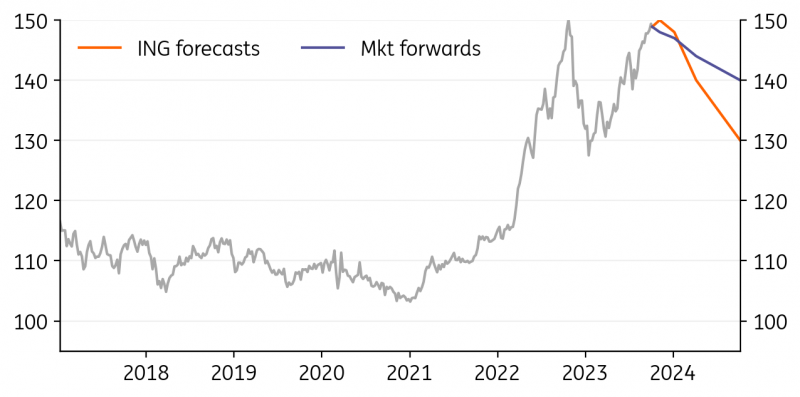

USD/JPY: A line in the sand at 150?

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/JPY

148.88

|

Mildly Bullish | 150.00 | 148.00 | 140.00 | 130.00 |

- Unless formally in an exchange rate mechanism (e.g. ERM-II) FX market players do not generally subscribe to ‘lines in sand’ – i.e. key FX levels which are protected by FX intervention. Yet last year Japanese authorities sold $37bn on the day $/JPY traded over 150. And recently $/JPY sold off 2% from just above 150 on suspected intervention. We’ll find out whether intervention did indeed take place when new data is released on 31 October.

- 31 October will also play a key role in the calendar given it is a Bank of Japan policy meeting, including new CPI forecasts. Speculation will build that dovish policy can be further reversed.

- However, expect $/JPY to stay near 150 until the $ turns in 1Q24.

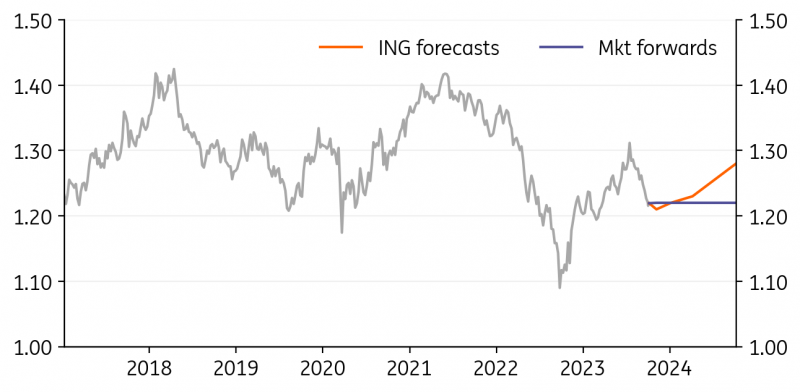

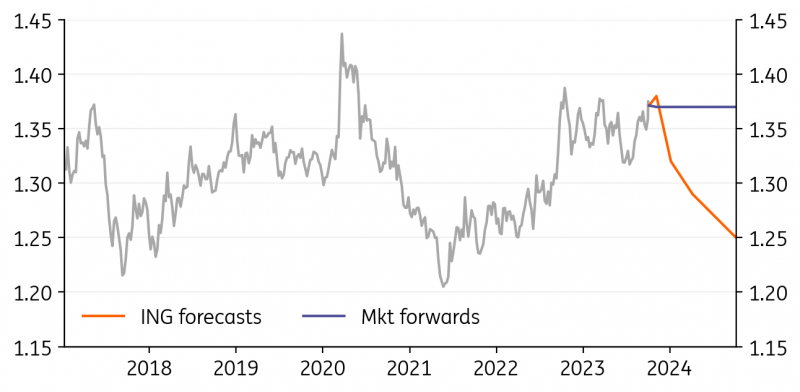

GBP/USD: Bank Of England looks done

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

GBP/USD

1.2194

|

Mildly Bearish | 1.21 | 1.22 | 1.23 | 1.28 |

- The Bank of England surprised some by leaving the Bank Rate unchanged at 5.25% in September. The vote was close however: 5-4. Barring some big upside surprises to the inflation and wage data published on October 17/18th, we think policy will be left unchanged at the Nov 2nd meeting and the cycle will be over.

- Investors still price 18bp of further BoE tightening, which suggests sterling can drop a little when this is priced out. But GBP/USD should find support at the lower end of this 1.20-1.30 range.

- Another date for the diary is November 22nd, when the Chancellor releases his Autumn Statement. He has said there is no room for tax cuts, but heading into an election year one never knows.

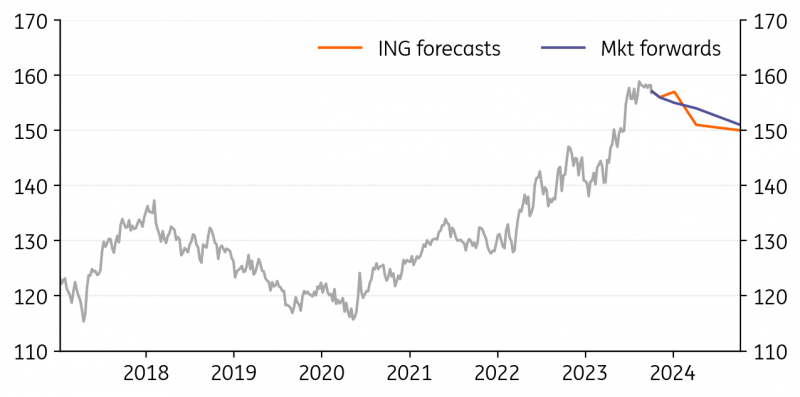

EUR/JPY: The Bank of Japan will decide its fate

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/JPY

157.05

|

Mildly Bearish | 156.00 | 157.00 | 151.00 | 150.00 |

- This year’s rally has stalled at 160 and could represent as significant a psychological level as 150 in USD/JPY. Expect the BoJ to increasingly determine the fate of EUR/JPY – be it through FX intervention or the BoJ deciding to finally unwind its Yield Curve Control policy. Late October may be too soon for that, but we do forecast this in 2Q24 along with a rate hike. As such the yen should outperform the euro in 24 as policy cycles switch.

- The yen is also uncorrelated, with risk assets meaning that it should see some natural safe haven demand if the investment environment deteriorates this Autumn.

- Both the euro and yen suffer equally from high energy prices.

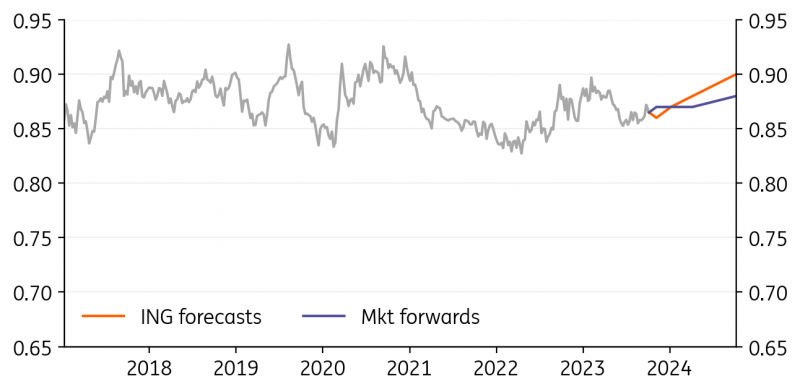

EUR/GBP: Sterling may face the greater headwinds in 2024

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/GBP

0.865

|

Neutral | 0.86 | 0.87 | 0.88 | 0.90 |

- We continue to have a gentle upside bias for EUR/GBP. On the activity side, the UK homeowner faces greater headwinds from higher mortgage rates as they slowly work through the system. Here the average rate on the UK mortgage stock is now 3.0% and will rise to 4.5% through 2024 as refinancing goes through.

- Expect EUR/GBP to bump up a little higher this year as the last vestiges of the BoE tightening cycle is priced out. And our call for 100bp of BoE easing in 24 (not priced now) could see 0.90.

- The wild card here is European politics. Elections this year mean that a lack of cohesion could see the Stability and Growth Pact automatically reintroduced next year and EZ peripheral debt hit.

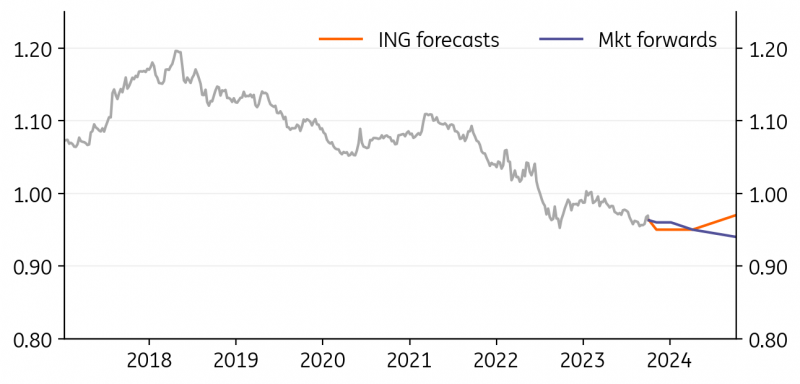

EUR/CHF: SNB ensures CHF is the strongest G10 currency this year

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CHF

0.9628

|

Mildly Bearish | 0.95 | 0.95 | 0.95 | 0.95 |

- The Swiss National Bank’s somewhat surprising decision to leave rates unchanged at 1.75% in September did not do too much damage to the Swiss franc. That is because the SNB says it is still selling FX as part of its effort to manage the trade-weighted Swiss franc higher. The SNB sold CHF30bn of FX in 2Q23 and probably continues to sell. That has helped make the franc the strongest G10 currency this year.

- Assuming the dollar stays strong for a while, the SNB will need to get its stronger trade-weighted franc (needed for monetary policy purposes) via a lower EUR/CHF. Hence our 0.95 forecasts.

- Some weakness in EZ peripheral debt markets will also help CHF.

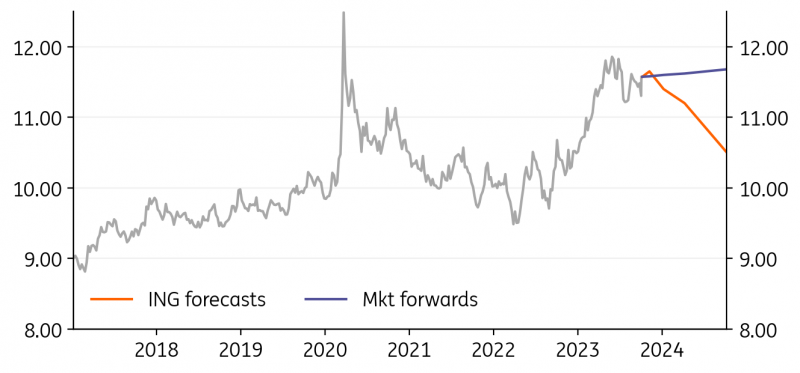

EUR/NOK: Back above 11.50, upside risks in the short term

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/NOK

11.57

|

Mildly Bullish | 11.65 | 11.40 | 11.20 | 10.50 |

- EUR/NOK volatility has finally rebounded, although the attempt to break lower was thwarted by the unwelcoming risk environment. The pair has spiked back above 11.50.

- Norges Bank is set to deliver another hike in December. That should be the last one but, if NOK depreciates, NB can easily add more tightening: the domestic economic picture isn’t worrying.

- The global bond selloff is negative for NOK, and while tighter monetary policy helped ease the pain, the recent oil price correction left the krone without a floor. Also, daily FX sales will remain high into year-end, and NOK downside risks remain tangible before any turn in US data boosts pro-cyclicals.

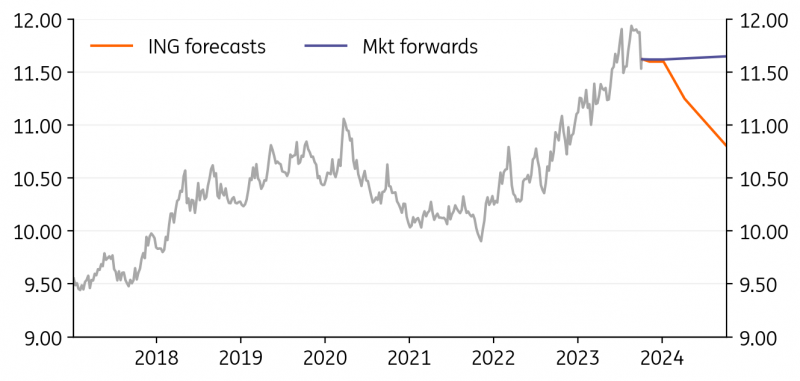

EUR/SEK: Riksbank plays the smart hedging game

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/SEK

11.62

|

Neutral | 11.60 | 11.60 | 11.25 | 10.80 |

- The Riksbank is officially in the FX market. FX reserves hedging operations are conducted for risk management purposes but have so far managed to make SEK the best performing G10 currency since their start.

- The first round of FX hedging data is due this week: we don’t know how much detail will be given, but we should be able to double-check our suspicion that the Riksbank is selling more FX when USD/SEK and EUR/SEK are higher. It may look like FX intervention, but the Riksbank will say it is loss-minimisation.

- The weekly FX hedging amounts aren’t enough to drive EUR/SEK much lower, but they should prevent a return to the highs. Another hike in November or January remains possible.

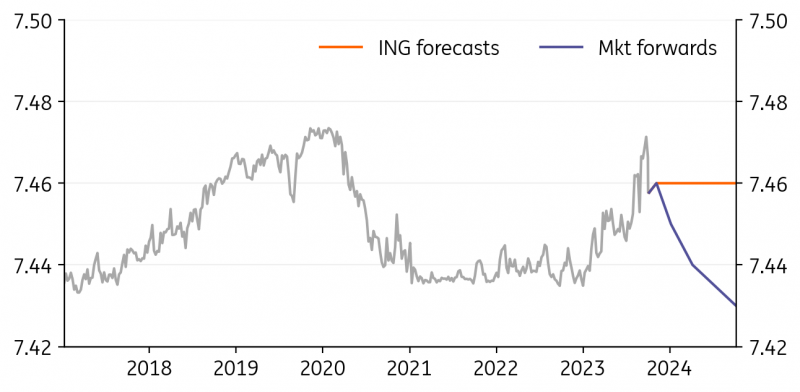

EUR/DKK: Some volatility, but back to 7.4600

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/DKK

7.4577

|

Neutral | 7.46 | 7.46 | 7.46 | 7.46 |

- Danmarks Nationalbank did not buy or sell DKK in FX interventions for the eighth straight month in August.

- EUR/DKK had a rather volatile month of September. The central parity mark (7.4600) was breached a few times in the first half of the month, but was followed by a drop to 7.4525 after the DN mirrored the ECB’s 25bp rate hike. The pair has rebounded to levels marginally below 7.4600.

- The recent volatility should not concern DN, as EUR/DKK remains very close to central peg parity. DN currently has no incentive to diverge from the ECB decision (likely, no more hikes). We expect stabilisation around 7.4600 or slightly below.

USD/CAD: The BoC may deliver another hike

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CAD

1.3713

|

Mildly Bullish | 1.38 | 1.32 | 1.29 | 1.25 |

- The data since the latest BoC meeting has flipped the narrative in Canada: employment jumped, wage growth accelerated, CPI rebounded to 4.0%, summer retails sales and GDP were strong.

- Markets are pricing in a 30% implied probability of an October BoC hike, and 50% of a December hike. Pricing would likely turn more hawkish if inflation stays sticky, helping the loonie.

- USD/CAD has spiked on the back of the dollar’s strength and the loonie’s sensitivity to high treasury yields. Unlike last time, the pair isn’t clearly overvalued, meaning that it will take a BoC surprise, improvement in general risk environment or oil prices to rebound to take it back to the 1.32/1.34 area by year-end.

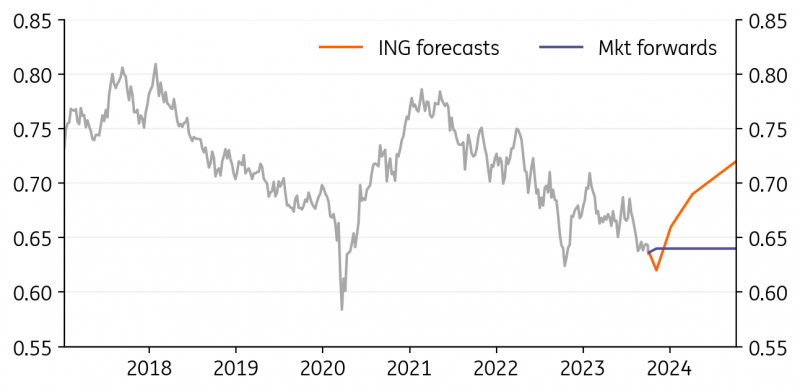

AUD/USD: Eyeing new lows

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

AUD/USD

0.6365

|

Mildly Bearish | 0.62 | 0.66 | 0.69 | 0.72 |

- We had called for a drop to 0.63 in last month’s edition of FX Talking: we believe there is still room for another drop in AUD/USD. The new bottom may be 0.61/0.62.

- The external environment remains very detrimental for the pair, which should stay under pressure unless the US data narrative flips, and that should not happen in the near term. Improvements in Chinese sentiment are – if anything at all – very gradual.

- The RBA might surprise with a hike after pausing in October. That depends on the 3Q CPI figure. Even so, the best a rate hike can do is offer a short-lived breather to AUD: developments in risk sentiment and the US bond market remain way more important

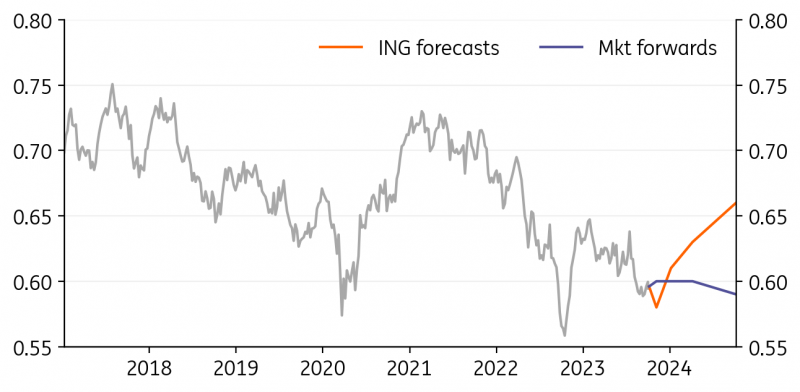

NZD/USD: Elections and inflation can help NZD in the crosses

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

NZD/USD

0.596

|

Mildly Bearish | 0.58 | 0.61 | 0.63 | 0.66 |

- The RBNZ stayed put in October, as expected given the proximity to the 14 October election in New Zealand and the lack of data.

- We recently published an update on NZD ahead of key events. Opinion polls are pointing to a win by the National Party, which has pledged to change the RBNZ remit to remove the dual mandate in favour of a stricter inflation objective. That can be a positive for NZD as long-term RBNZ rates can be repriced higher.

- In the shorter run, we still deem the RBNZ disinflation projections as a gamble, and see upside risks to the 3Q CPI figures (released on 16 October). A return to tightening is a real possibility. Any benefits to NZD would be more visible in the crosses: NZD/USD stays mostly a USD story, and may struggle to recover just yet.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download articleThis article is part of the following bundle

9 October 2023

FX Talking: Bond vigilantes take control This bundle contains 5 Articles