G10 FX Talking: Pressure against $ building from all sides

- 10 February

- FX Talking

The dollar outlook is broadly bearish. The benign take is that, for the first time since the pandemic, overseas asset markets and currencies look attractive. Here, sentiment in Europe and Asia is picking up, helped by fiscal stimulus. The more negative take is that investors are increasingly concerned about their concentration risk in US assets and USD

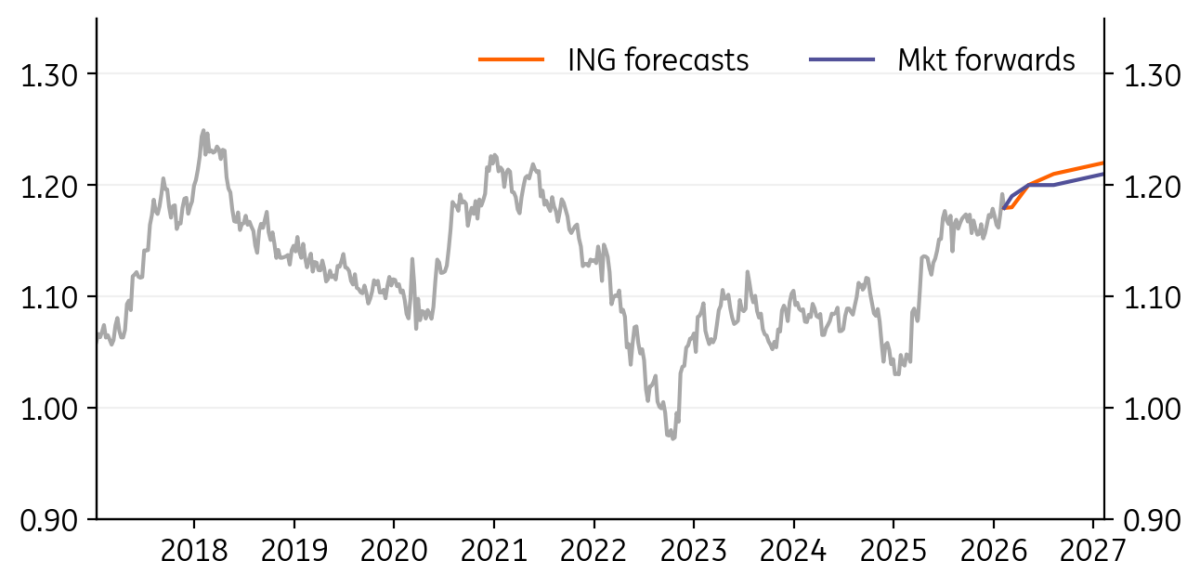

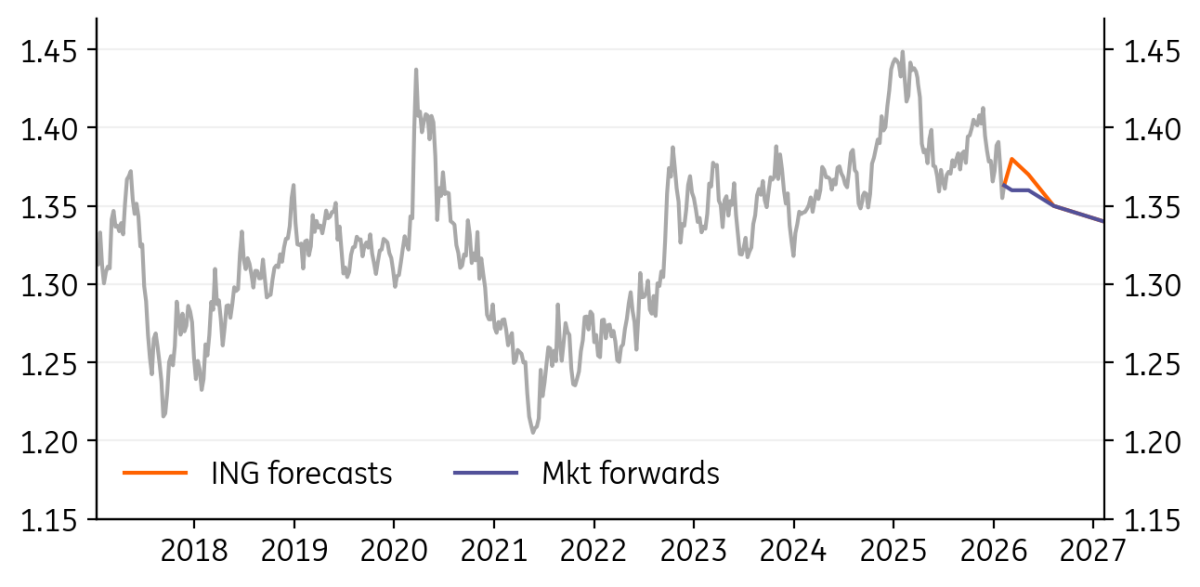

EUR/USD: Dollar negatives stacking up

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/USD

1.19

|

Neutral | 1.18 | 1.20 | 1.21 | 1.22 |

- The dollar remains under pressure on both push and pull factors. The ‘pull’ factor is the rotation into pro-cyclical and EM currencies as investors bet on global growth this year. ‘Resilience’ is an oft-used word to describe much of the global economy, which has so far survived the tariff threat. Additionally, the dollar has struggled to show safe haven characteristics amid geopolitical tensions.

- The ‘push’ factor remains concerns about US policymaking and the future Fed under Kevin Warsh. Equally, the US labour market is softening, and the Fed looks set to cut in June and December.

- It is early days, but it seems the eurozone recovery is on track and the ECB will not react to a strong EUR/USD until it’s closer to 1.25.

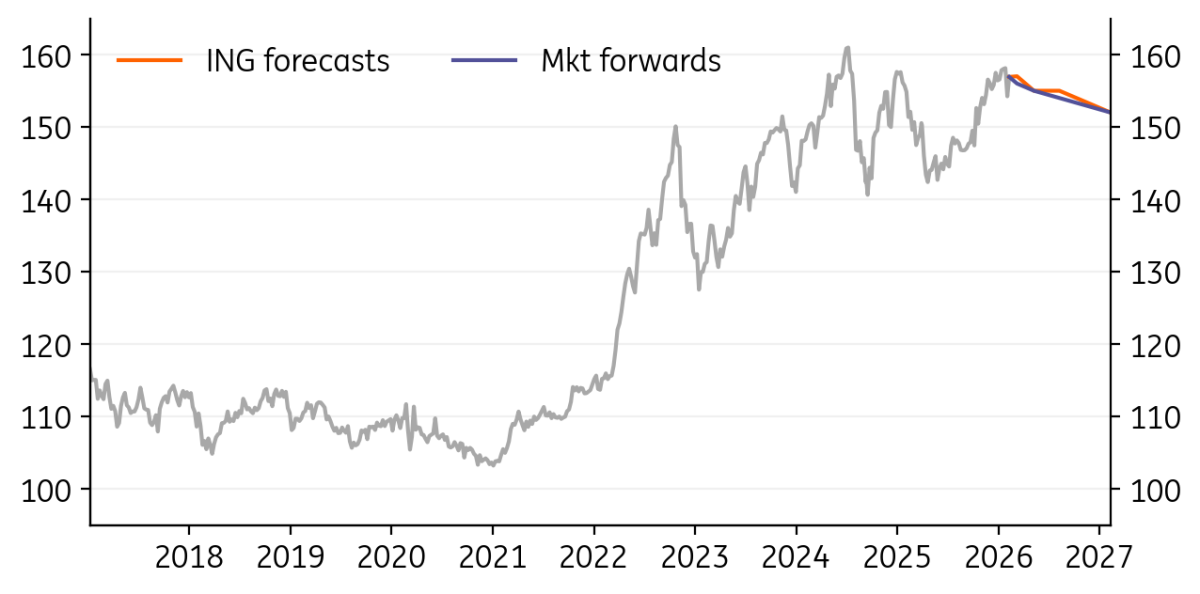

USD/JPY: LDP given a strong mandate

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/JPY

157.00

|

Mildly Bullish | 157.00 | 155.00 | 155.00 | 152.00 |

- February’s snap election in Japan delivered an emphatic win for the ruling LDP. Prime Minister Sanae Takaichi now has a strong mandate to deliver on growth and aggressive foreign policy – including a defence build-out. The challenge for the yen is whether to look at things negatively – eg, the sovereign risk of a JGB sell-off – or positively on the back of looser fiscal and tighter monetary policy.

- Barring a big JGB sell-off, we suspect the yen finds buyers in the 158/160 per USD – knowing that Japanese authorities stand ready to intervene there. $100bn was sold at similar levels in 24.

- Over the year, we look for two Fed rate cuts and at least one Bank of Japan rate hike to drag USD/JPY closer to the 150 area.

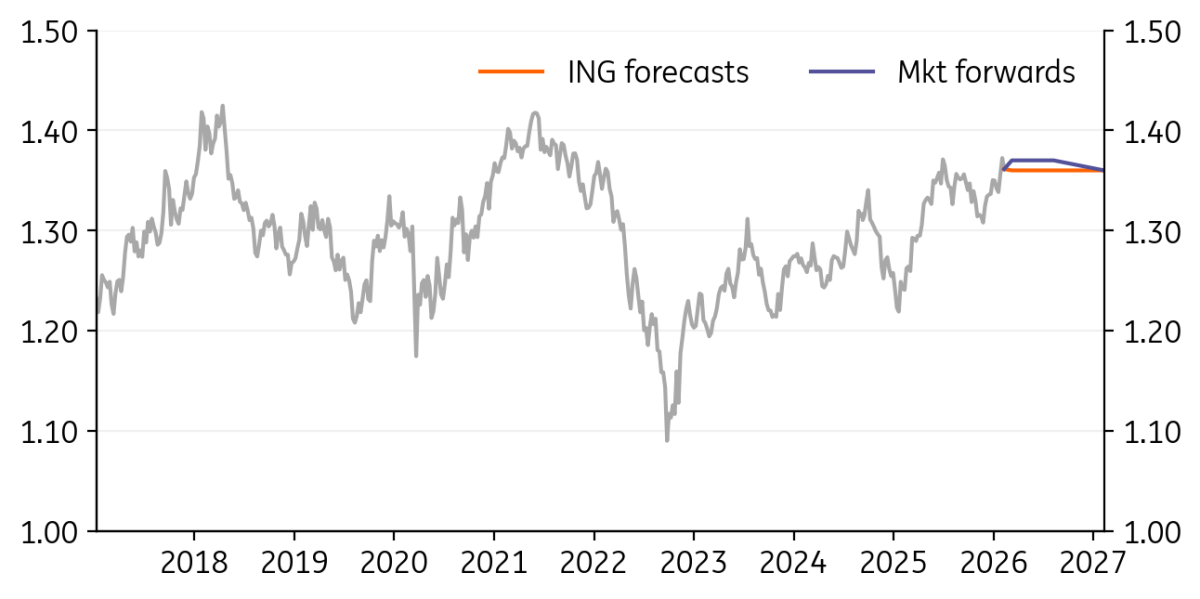

GBP/USD: Politics and dovish BoE to limit GBP gains

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

GBP/USD

1.36

|

Neutral | 1.36 | 1.36 | 1.36 | 1.36 |

- The softer dollar and the benign risk environment have provided support to GBP/USD, but sterling negatives remain. The most pressing is probably the UK political scene. Here, PM Keir Starmer’s judgement is being questioned over the appointment of Peter Mandelson as UK ambassador to the US, with some key allies having already resigned. Starmer’s departure would likely see Chancellor Rachel Reeves also leave – hitting sterling and Gilts.

- At the same time, the BoE in January was more dovish than expected, voting 5-4 for unchanged rates. Markets are coming towards our house call of rate cuts in March and June.

- A weak dollar and a weak pound delivers a flat GBP/USD profile.

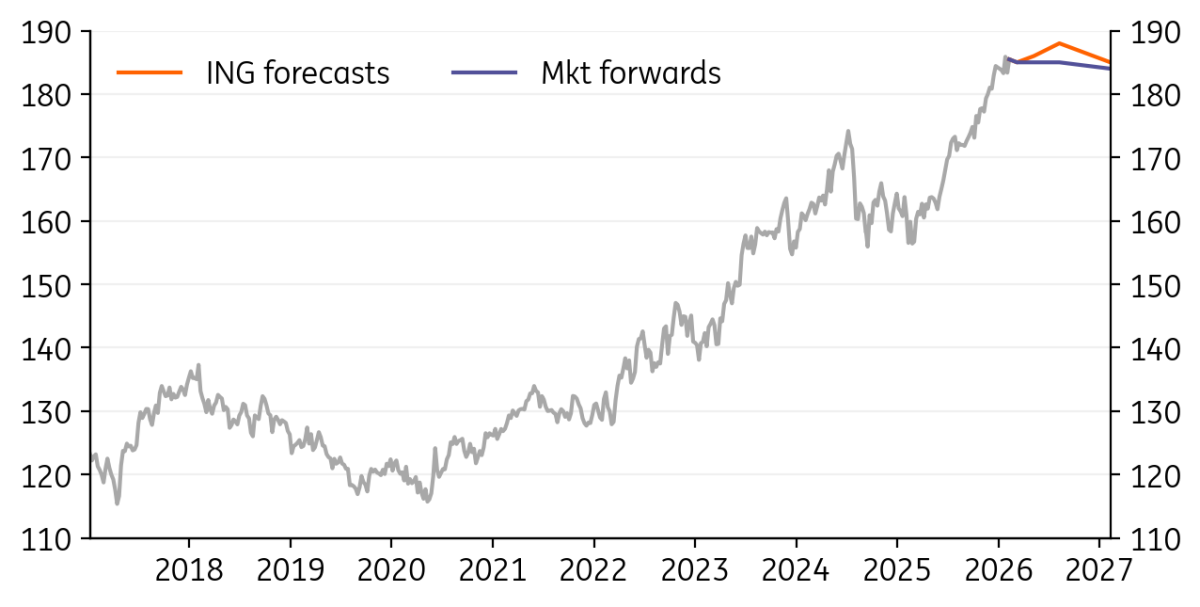

EUR/JPY: No signs of a top yet

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/JPY

186.00

|

Neutral | 185.00 | 186.00 | 188.00 | 185.00 |

- EUR/JPY stay very bid, and there is little confidence that authorities can turn this trend around. The ECB has yet to ring the alarm bells over euro strength – citing this year’s moves as being part of baseline considerations. Tokyo is far more worried by a weaker yen, but it probably requires some earlier and more aggressive BoJ rate hikes to turn this trend around.

- Currently, we do not see the BoJ hiking until June – yen negative. But an earlier April hike (now 50% priced) could provide the yen with some stability.

- On the macro side, eurozone sentiment is picking up and German fiscal stimulus should make a positive mark on growth from 2Q.

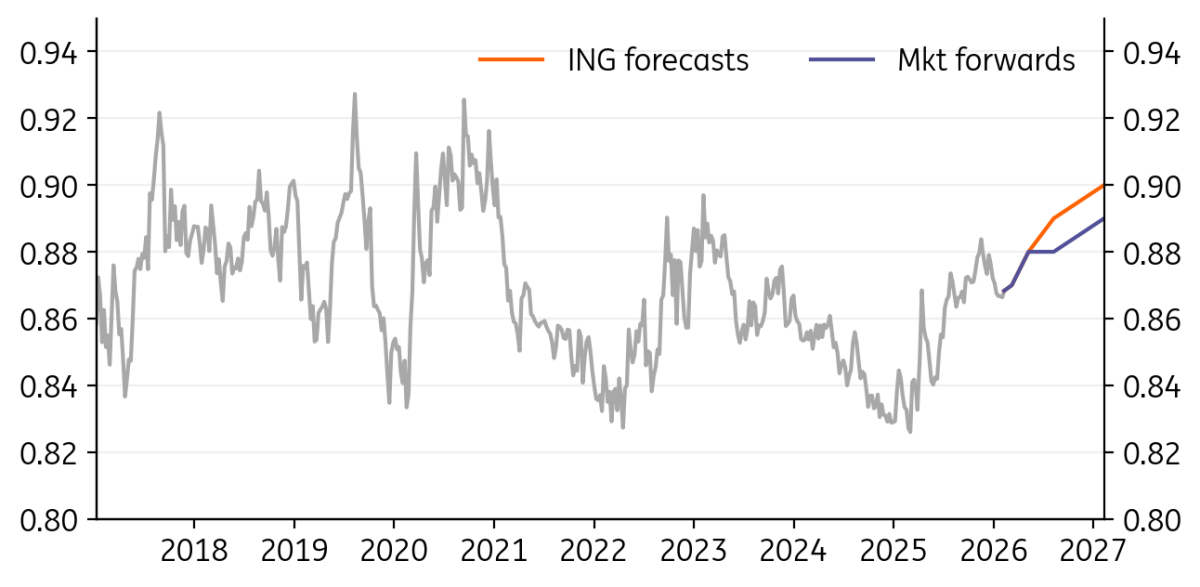

EUR/GBP: Upside risks prevail

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/GBP

0.87

|

Neutral | 0.87 | 0.88 | 0.89 | 0.90 |

- A sterling short squeeze amongst the asset management community had dragged EUR/GBP close to 0.86 before politics and the BoE hit. Now the EUR/GBP bias is higher as we brace for further pressure on PM Starmer. Potential flashpoints are the performance of the Labour Party in a by-election on 26 February and local elections on 7 May. His departure and that of his Finance Minister, Rachel Reeves, would hit sterling and Gilts.

- In terms of the BoE trajectory, we think it will have enough evidence to cut rates to 3.50% on 19 March. Inflation data should then fall even faster in 2Q.

- The Labour Party somehow moving closer to Europe, eg, rejoining the customs union, is the bullish wild card for GBP.

EUR/CHF: Swiss franc proving the dollar debasement hedge

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/CHF

0.92

|

Neutral | 0.92 | 0.93 | 0.94 | 0.95 |

- EUR/CHF remains exceptionally offered as global investors continue to position for the dollar debasement trade. Switzerland’s significant trade and net international investment surplus is one of the main attractions, as is its budgetary position. Real interest rates are not attractive, however, at around 0%.

- The Swiss National Bank has been sounding remarkably relaxed about CHF strength – perhaps because European growth is picking up, but also because its options to cut rates into negative territory or intervene and buy FX look very limited.

- We had favoured a EUR/CHF bounce on European growth this year. But the dollar debasement trade dominating is the risk.

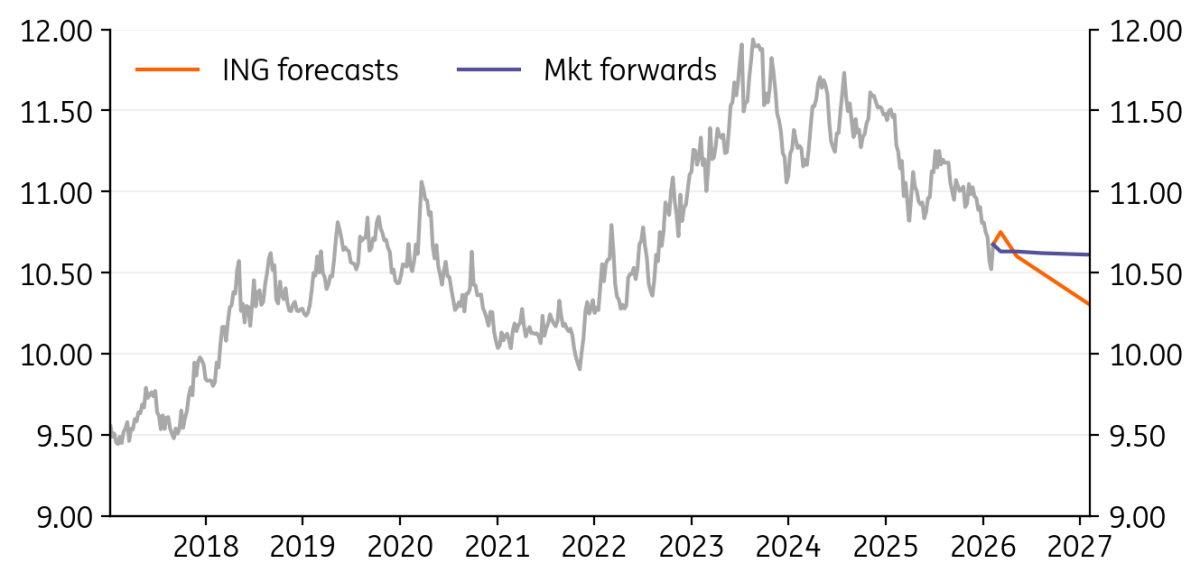

EUR/SEK: Short-term rebound may extend

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/SEK

10.67

|

Mildly Bullish | 10.75 | 10.60 | 10.50 | 10.30 |

- The krona had a good run during January’s market turmoil, likely aided by more capital repatriation. The short-term technical picture still looks supportive for a further EUR/SEK rebound, though.

- Our call is another leg higher in EUR/SEK in the coming weeks, although the recent tendency to undershoot its short-term fair value means the rally could stall before reaching 10.80.

- The outlook into year-end remains positive for SEK, in our view. Sweden’s growth outlook continues to improve, and markets will be tempted to price in rate hikes. We now target 10.30 for year-end in EUR/SEK.

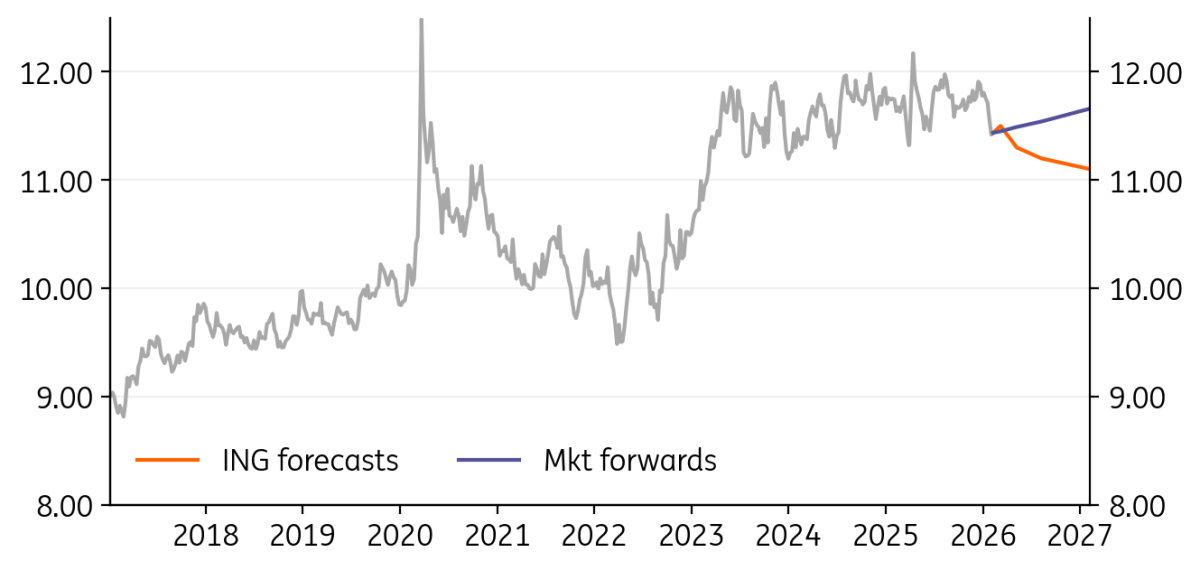

EUR/NOK: Krone looking healthy

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

11.47

|

Neutral | 11.50 | 11.30 | 11.20 | 11.10 |

- The strong start of the year for oil has generated a rare outperformance of NOK over SEK. We also think the krone’s rally has more fundamental justification than SEK’s and see more limited upside room in the short term in EUR/NOK than EUR/SEK.

- Norges Bank’s outlook for 2026 remains very uncertain. We still think underlying CPI needs to drop back below 3.0% to prompt any dovish shift. And while our call remains for two cuts this year, in June and September, the risks are on the hawkish side.

- We have revised our EUR/NOK profile lower. However, we aren’t calling for a break below 11.00 this year, as we expect lower oil prices and rate cuts to partly offset strong NOK fundamentals.

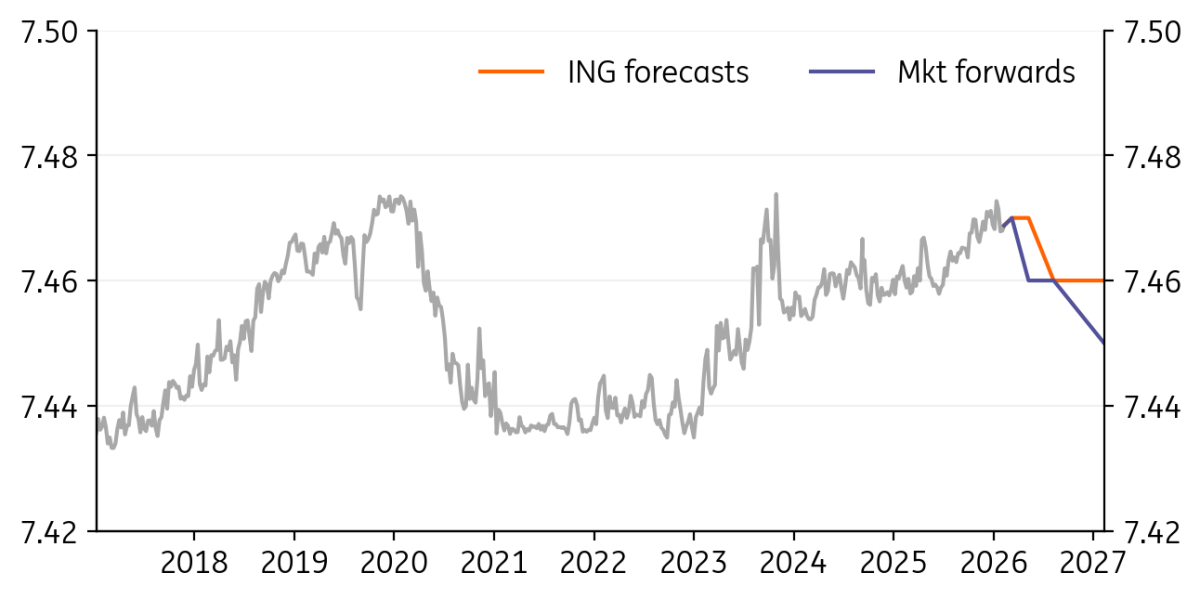

EUR/DKK: No interventions in January

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

EUR/DKK

7.47

|

Neutral | 7.47 | 7.47 | 7.46 | 7.46 |

- EUR/DKK forwards have returned to normality with geopolitical risk abating, and spot is back below 7.470.

- The central bank of Denmark didn’t intervene in the FX market in January; this is good news as it signals spot held up on its own, but it also rules out the knock-on liquidity effect of intervention into forwards. In other words, it tends to confirm speculation that higher rates in Denmark via forwards were driven by Greenland risk.

- We still see an elevated risk that FX interventions will be deployed at some point this year as the rate gap keeps EUR/DKK well supported. That won’t be a problem, anyway, for a very well-equipped central bank reserve-wise, like the Danish one.

USD/CAD: USMCA noise major risk ahead

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CAD

1.36

|

Mildly Bullish | 1.38 | 1.37 | 1.35 | 1.34 |

- Data isn’t giving any strong suggestions to the Bank of Canada, which in turn has remained neutral. Some tightening speculation has abated, and we still expect the jobs market to remain the key factor to watch to gauge the risks of an additional cut.

- That is very much linked to upcoming USMCA renegotiations, which may well prove rocky. Trade uncertainty has had a very tangible impact on hiring intentions in Canada.

- We remain pessimistic on the Canadian dollar’s outlook against most of the G10, although our call for further USD declines throughout 2026 means USD/CAD could still end the year below 1.35.

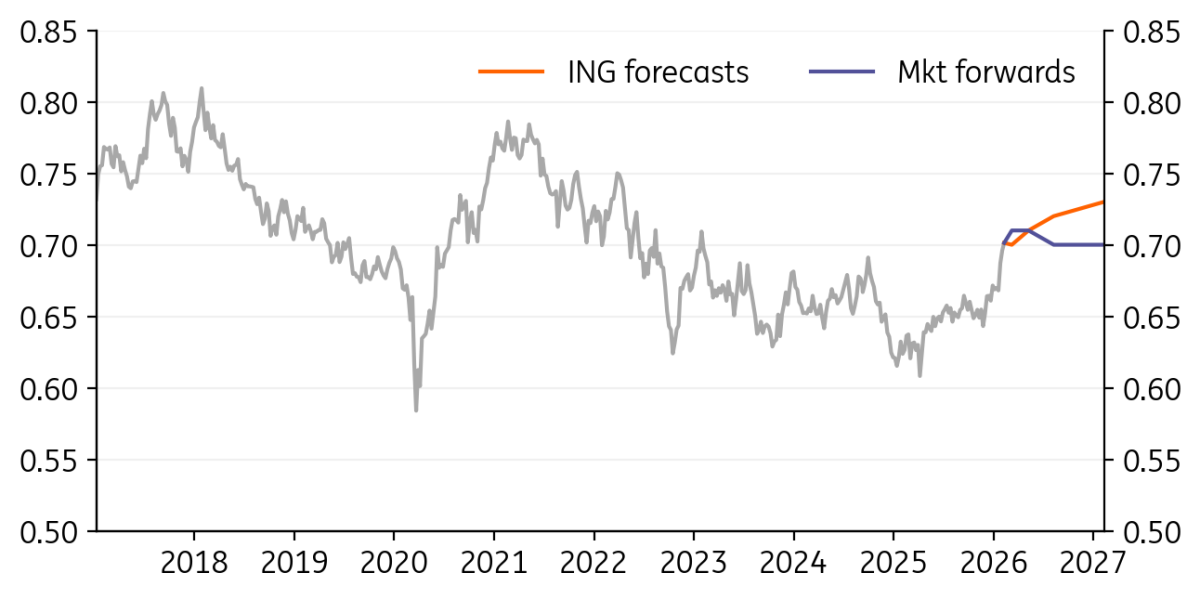

AUD/USD: RBA to hike again in May

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

AUD/USD

0.70

|

Neutral | 0.70 | 0.71 | 0.72 | 0.73 |

- The Reserve Bank of Australia raised rates in February, and markets continue to stay hawkish. The RBA’s communication didn’t provide much clarity: inflation is a concern, but the baseline for rates seems less hawkish than market expectations.

- We are in data-dependency mode, in our view, and we think further inflation stickiness will prompt another hike in May by the RBA. But we think that will be the last one of 2026.

- The AUD/USD rally has gone a bit too far, too fast. We see room for a short-term correction, but after that, fundamentals will still be supportive of a multi-quarter rally. We revise our AUD/USD year-end call to 0.73

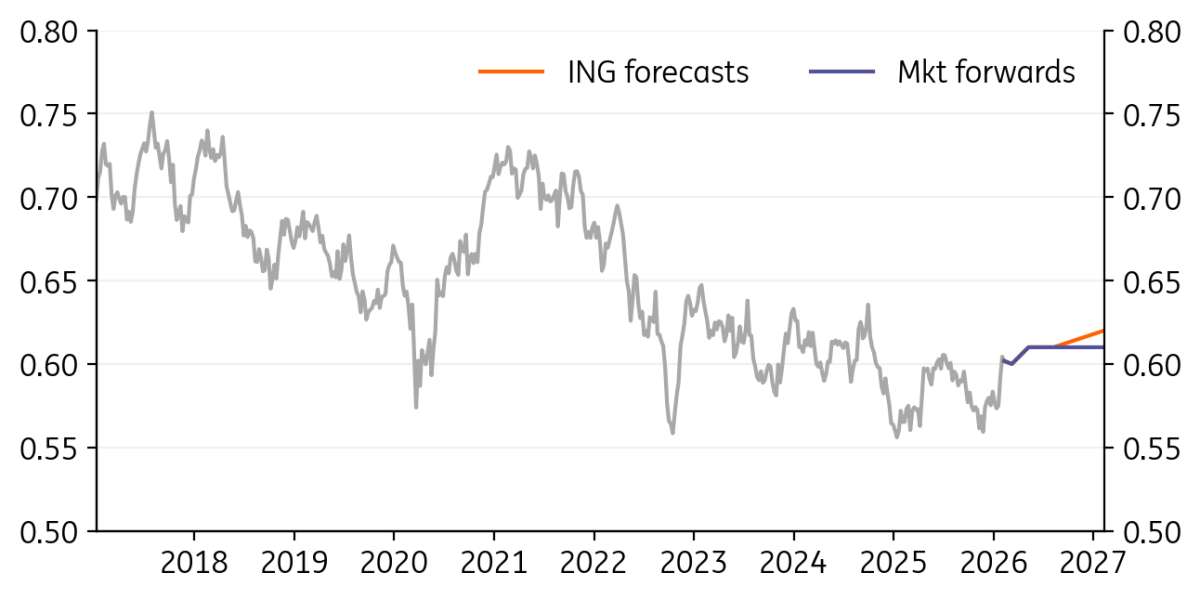

NZD/USD: Ample room for hawkish repricing

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

NZD/USD

0.60

|

Neutral | 0.60 | 0.61 | 0.61 | 0.62 |

- We have a preference for NZD over AUD in the near term. The technical picture is less stretched, and markets have more room to price in hikes on the NZD curve in our view.

- The RBNZ meets on 18 February and will need to acknowledge inflation has been materially hotter than projected, and given the low starting point for rates, we could get some hawkish hints.

- We’ll then need to wait until late April to see 1Q CPI numbers, meaning a potential hike would, if anything, become a possibility only from May onwards – but more likely from the summer. We remain bullish into year-end on NZD/USD given ample room for hawkish repricing and USD weakness.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

10 February

FX Talking: Dollar appetite erodes

- This bundle contains 6 Articles