G10 FX Outlook 2024: The dollar’s long goodbye

A year ago writing for the 2023 G10 FX outlook, we were calling for less trend and more volatility. That worked for the first half of the year before a dollar bull trend took over. Based on our call for Fed easing next year, we now argue that G10 FX markets will be characterised by more trend – a dollar bear trend, that is – and less volatility

To challenge the dollar, currencies will need a lot of protection

A typical financial market response to the start of a Federal Reserve easing cycle would be a bullish steepening of the US yield curve on the prospect of reflationary policy coming through. To speak of ‘reflationary’ policy right now seems criminal – but the Fed has a dual mandate, and if inflation is coming under control through 2024 it can cut rates to ameliorate the impact on the labour force.

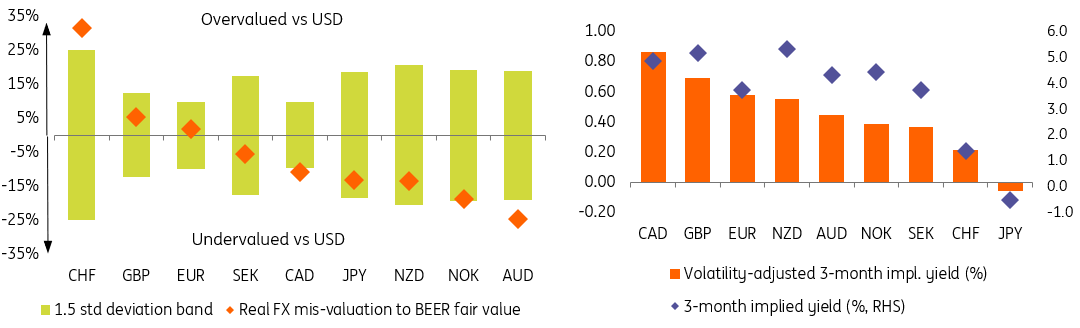

Bullish steepening of the US yield curve normally favours the commodity currencies, and that's our conviction call in the G10 space. As outlined in our Behavioural Equilibrium Exchange Rate (BEER) model below, the commodity currencies are the most undervalued in the G10 space. Their extreme undervaluation provides some much-needed protection against any continuing dollar strength. Notably, the euro and sterling do not have such protection.

Looking across the currency blocs then – after relatively range-bound trading into year-end – we expect the dollar bear trend to pick up a little pace into the second quarter of 2024 as the short-end of the US curve starts to come substantially lower.

European FX should be lifted, but stagnant eurozone growth and the risk that the European Central Bank cuts too early suggest that EUR/USD does not lead this rally. Neither does GBP/USD, given our mildly bullish view on EUR/GBP and 100bp of Bank of England easing. Having outperformed this year, we expect the Swiss franc to be flat against the euro in 2024 as the Swiss National Bank seeks more stability than strength in the nominal trade-weighted franc.

Better positioned in Europe we think (and conditioned on a lower interest rate environment) are the Scandi currencies. Both the Norwegian krone and the Swedish krona are undervalued – the krone more so. Both central banks would prefer stronger currencies and the krone probably has a better chance of a recovery in 2024 given a stronger economy and its more severe undervaluation after the rally in energy prices.

Our favourite currency in 2024 is the Australian dollar

Our favourite currency in 2024, however, is the Australian dollar. High US rates and weak Chinese growth have repressed it and made it the most undervalued currency in the G10 space. The release valve of lower US rates should allow the Aussie dollar to lead the currency recovery against the US dollar. A hawkish Reserve Bank of Australia should not hurt either. We are also bullish on the NZD/USD and are interested in whether the new government changes the Reserve Bank of New Zealand’s remit – a potentially bullish factor for NZD. USD/CAD should come lower too, and while Canada’s high yield helps, its proximity to the US may be more of a burden in 2024.

On the subject of carry, lower volatility favours the carry trade and also the yen as a funding currency. However, we have some quite aggressive forecasts for a lower USD/JPY on the back of a weaker dollar and finally a proper Bank of Japan exit from ultra-loose policy. Big policy changes in Japan can have a big impact on USD/JPY as in 2013. Let’s see how the start of 2024 progresses and whether the BoJ is prepared to make its move after all.

G10 FX valuation and carry

EUR/USD: Lifted higher by the tide of lower US rates

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/USD | 1.08 | Bullish | 1.07 | 1.08 | 1.10 | 1.12 | 1.15 |

US slowdown is central: Our forecast for a higher EUR/USD next year hangs wholly on the view that the US will slow down, inflation will ease and the Fed will be able to make monetary policy less restrictive. Currently we forecast 150bp of Fed easing starting next May/June. This is premised on tighter financial conditions finally weighing enough on aggregate demand to see US growth converge on the stagnant trajectories, especially in Europe. Our team forecast US growth at just 0.5% next year versus the consensus of 1.0%. Equally, our end year 2024 EUR/USD forecast of 1.15 is slightly above the current consensus of around 1.11. In terms of timing the trajectory, our current bias is that EUR/USD strength will become more apparent from the second quarter onwards. The dollar traditionally performs well at the start of the year and with the eurozone in recession, the first quarter may be too early to see a decisive turn higher in EUR/USD.

ECB could crumble: The headwinds to a EUR/USD rally largely stem from weak eurozone growth and the risk that the ECB chooses to cut rates alongside the Fed. This would limit the expected narrowing in yield differentials at the short-end of the curve. Our team forecast three quarters of negative eurozone growth (3Q23 to 1Q24 inclusive) and full-year 2024 eurozone growth at just 0.2%. We expect 75bp of European Central Bank (ECB) easing in 2024 starting in the third quarter, but clearly the risk is that the ECB eases earlier and the Fed later such that the starting pistol for the EUR/USD rally is never fired. Equally, a failure of European governments to agree on fiscal reform by year-end 2023 could see the re-introduction of the Stability and Growth Pact in early 2024 – an unwelcome arrival in a recession.

EUR/USD looks fairly valued: Our medium-term fair value model suggests EUR/USD is fairly valued down at these lowly levels. In other words, there is not the kind of extreme undervaluation that has supported EUR/USD at these levels in the past. This really does build the case that if there is to be a EUR/USD rally, it will have to be driven by the dollar leg. Away from the Fed easing story there is also the risk of US fiscal deterioration and de-dollarisation – perhaps both slow-burn stories. There is also the small matter of the US election. Most commentators warn of a Trump 2.0 administration being ‘louder’. Depending on how the opinion polls progress, we presume any swing in favour of a second term for Donald Trump to be dollar positive – given the experience of the loose fiscal and protectionist policy agenda during his last stay at the White House.

USD/JPY: Tokyo prays for a turn in the dollar

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| USD/JPY | 151.00 | Bearish | 148.00 | 140.00 | 135.00 | 130.00 | 130.00 |

A US slowdown would make life so much easier: So far this year Japanese authorities have chosen not to intervene in FX markets even though USD/JPY has traded over 150. Under similar circumstances last year, the Japanese sold $70bn. While the rhetoric from Tokyo remains acute – meaning intervention could be imminent – we suspect local policymakers are instead waiting for a market-led turn lower in US rates in the dollar. Such a move would of course avoid the need for intervention but also allow the Bank of Japan (BoJ) to exit its super-loose monetary policy next year without Japanese Government Bond (JGB) yields surging. Here our call is that the BoJ will remove its negative 10bp charge on Policy-Rate Balances in the second quarter. This policy adjustment could well be forewarned in January, with the next release of the BoJ’s Outlook for Economic Activity and Prices. A CPI ex food forecast above 2% for FY25 would be a strong signal here that a policy change were forthcoming.

Portfolio flows have been key: Policymakers around the world have acknowledged that higher US yields have dominated the FX environment this year. 10-year US Treasuries have recently been offering over a 400bp pick-up to 10-year JGB yields and Japanese portfolio flow data confirm that Japanese residents have increased their purchases of foreign assets sharply this year. Combined with foreigners cutting back on Japanese investments, data shows that Japan has seen around a net $175bn portfolio outflow over the last six months. The shape of the US yield curves means that a lot of the Japanese flows into US debt will have been unhedged. This means that short-dated US rates – i.e. hedging costs – will have a big say on USD/JPY in 2024. Our call here is that US short-dated rates start to front run the first Fed rate cut in May and that USD/JPY will turn decisively lower.

Geopolitical risks: What we learned in 2022 was that an energy supply shock could do a lot of damage to the yen. As a fossil fuel importer, Japan remains a price taker in energy markets and over recent month’s Japan’s current account figures have only just managed to crawl back into positive territory after the 2022 shock. Clearly any escalation of the conflict in the Middle East and higher crude prices would again hit Japan’s terms of trade and weaken the yen. The only difference now is that Japanese consumers are becomingly increasingly dissatisfied with cost-of-living challenges and dissatisfied with the government. This suggests that government may take an even greater interest than usual in the value of the yen. Equally, the government is now looking at some extra fiscal and at the margin could support higher wage rounds in 2024 – a requirement for the BoJ undoing loose monetary policy.

GBP/USD: A lacklustre recovery

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| GBP/USD | 1.25 | Mildly Bullish | 1.23 | 1.23 | 1.24 | 1.24 | 1.28 |

Bank of England is done: The strong dollar is again keeping GBP/USD pinned down, but compared to this time last year, the UK’s finances are seen in safer hands. This means that we are trading in the low 1.20s rather than the low 1.10s. As above, we have outlined the case for a cyclical fall in the dollar as the decline in short-dated US yields accelerates through 2024. Even though the BoE has re-introduced forward guidance on its restrictive 5.25% bank rate for an extended period, we think a lower policy rate is also likely next summer. We forecast that all of the BoE’s key inflation metrics will be heading in the right direction through 2024, allowing the BoE to deliver 100bp of easing next year starting in August. This probably means that GBP/USD will struggle to sustain any gains over 1.30.

The fiscal monetary mix: A UK general election needs to be held before January 2025, with speculation that the ruling Conservatives may choose May or October. The question is whether Chancellor Jeremy Hunt opts for some fiscal give-ways pre-election – while promising some fiscal consolidation post-election. Fiscal stimulus is not priced, but at the margin could be a mild sterling positive if it were introduced in a credible manner. For instance, our team forecasts modest, positive UK growth every quarter of next year unlike the mild recessions we forecast for the US and the eurozone. Looser fiscal policy at a time of restrictive monetary policy in 1the first half of 2024 would help the pound.

In the orbit of EUR/USD: EUR/GBP realised volatility is not too far off the lows seen over the last two decades. This means that the broad EUR/USD trend will largely define that of GBP/USD – unless we get some enormous independent move in sterling as was seen around the time of the brief Liz Truss government in September 2022. That probably means GBP/USD trading in the 1.20-1.25 range for the next three to six months (with perhaps some downside risks), before better eurozone growth in the second half of 2024 and lower US rates allow EUR/USD and GBP/USD to make their moves higher.

EUR/JPY: The turn will take time

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/JPY | 163.00 | Bearish | 158.00 | 151.00 | 149.00 | 146.00 | 150.00 |

The widow maker: Trying to fight the rally in EUR/JPY has been a fool’s game since 2020, as this cross has rallied close to 40% since then. We had thought that the 160 level might have been some kind of line in the sand for Japanese authorities – but maybe that level is 170. Driving the yen underperformance has clearly been the low rates on offer in Japan and the BoJ’s policy of continuing to print money even during a global inflation scare. The fact that the perennially dovish ECB switched sides last year and have taken deposit rates to 4.00% has clearly justified this EUR/JPY rally too. That divergence should switch in 2024, first as the BoJ prepares to release itself from its dovish straitjacket. And weak eurozone growth next year will now switch market attention to the start of the ECB easing cycle – in the third quarter of 2024 or perhaps sooner.

Eurozone business model requires a weak euro: Of the many challenges to eurozone growth, perhaps the largest is faced by the German industrial sector. Germany can no longer rely on cheap energy and globalisation to run its export machine. While domestic demand stagnates – unaided by any fiscal stimulus – and inflation slows, the eurozone may once again be tempted to rely on exports to buy it some time for economic transition. A weaker euro would help – especially if competing in third markets with the likes of Japan and China. In fact, even though EUR/USD is on its lows, the ECB’s broad, nominal trade-weighted euro is barely 2% off its all-time highs. In real terms the euro is still well off its peak in the mid-2000s, but that was a period when world trade was booming.

Where we’re wrong: EUR/JPY has a modest positive correlation with global equity markets. If a more a traditional business cycle emerges where equities turn lower headed into a US recession (equities normally turn six months before a recession) and bonds rally, then EUR/JPY should come lower in line with our forecasts. If, however, lower US rates lead to both bonds and equities rallying then we are probably underestimating the performance of EUR/JPY. On the bond side as well, we will be interested to watch developments in the eurozone yield. The current inverted yield curves in Europe make it too expensive for Japanese investors to FX hedge European bond portfolios. Bullish steepening of European curves would see FX hedge ratios increase and EUR/JPY finally.

EUR/GBP: What about election risk?

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/GBP | 0.87 | Mildly Bullish | 0.87 | 0.88 | 0.89 | 0.90 | 0.90 |

Labour’s election to lose? Moving into a UK election year, the question is whether sterling requires an election risk premium and if so, why? During the last couple of elections, 2017 and 2019, sterling traded with a 5% risk premium – i.e. EUR/GBP traded 5% higher than conventional drivers would expect. A 5% risk premium at those elections was understandable given that in 2017 Theresa May was struggling to take the UK out of the EU and in 2019 the opposition Labour candidate, Jeremy Corbyn, was proposing ‘quantitative easing for the people’. Labour voters will be hoping that a 2024 election is more akin to Tony Blair’s landslide win in 1997. Back then sterling did not trade with much of a risk premium at all. Indeed, it now seems that the current shadow chancellor, Rachel Reeves, is perceived well by the financial community. Continued strength of Labour in the opinion polls does not need to damage sterling.

Faster BoE easing presents upside bias: Our core view here is that in an environment of lower aggregate demand and inflation moving back towards target, the BoE will ease more aggressively than the eurozone and that EUR/GBP will rise. The BoE has been criticised for the fact that the UK has had a worse inflation problem than elsewhere in the world, but in 2024 we think it will be in a position to unwind its restrictive 5.25% Bank Rate more quickly than the ECB. The risk here is that more disfunction in the eurozone in early 2024 prompts earlier ECB easing than we currently forecast (September 2024), but we doubt that this should lead to too much downside in EUR/GBP.

Low volatility: We have a mildly bullish outlook for EUR/GBP into 2024, but our call for 0.90 in the second half of 2024 is not particularly far above the outright forward. Historical volatility is very low here and that is reflected in one year implied EUR/GBP volatility – now just 5.7%. This had traded as low as 4% in 2006/07 and we do not have any high conviction in saying that volatility cannot fall further. In other words, we are not looking for major swings in EUR/GBP. For reference, however, one year volatility did trade 11% in September 2022 during Liz Truss’s ill-fated government and corporate treasurers, looking for some optionality in FX hedging, could take advantage of the current low level of implieds.

EUR/CHF: SNB will want to keep things stable

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/CHF | 0.97 | Neutral | 0.96 | 0.96 | 0.96 | 0.96 | 0.96 |

The strongest G10 currency: The Swiss franc (CHF) has proven to be the strongest G10 currency in the world this year – even surpassing the dollar. Despite the natural demand for the CHF from Switzerland’s perennially large current account surplus (now around 10% of GDP), the Swiss National Bank (SNB) has also been buying CHF. SNB sales of FX reserves amounted to CHF75bn in the first half of this year and continued the U-turn on FX intervention that the SNB undertook in the summer of 2022. Having traditionally been a large buyer of FX, the SNB switched to FX sales as part of its monetary policy toolkit. As we understand it, its decision has been to target a stable real CHF – requiring nominal CHF appreciation to offset higher inflation amongst overseas trading partners. In fact, the SNB has even allowed the real exchange rate to appreciate this year too – which we speculate could be part of a desired tighter monetary conditions package.

Crunching the numbers: Given that we are not forecasting SNB rate cuts next year, we make the assumption that the SNB will not be looking for monetary stimulus from a weaker real CHF. We assume at a minimum the SNB will want a stable real exchange rate. Plugging in our forecasts for Switzerland’s inflation differential with trading partners, what was a 5.5% differential in late 2022 could be narrowing close to zero by the end of 2024. Thus in order to keep the real exchange rate stable, the zero inflation differential means the nominal CHF exchange rate should be roughly stable too. If we plug in our FX assumptions and weights for the Swiss franc’s main trade partners, such as the eurozone (49%), the US (20%), China (12%) and the UK (9%), we can calculate what level of EUR/CHF would deliver a stable trade-weighted CHF by the end of 2024. Those assumptions of e.g. EUR/USD at 1.15, USD/CNY at 7.00 and GBP/USD at 1.28 produce a EUR/CHF number near 0.95/96.

Eurozone recession favours a soft EUR/CHF too: Our team forecasts the eurozone entering a technical recession in the first quarter of 2024. Periods of weak growth in the eurozone typically pressure test the system including the fiscal policy of southern Europe. The potential return of the Stability and Growth Pact may clash with loose Italian fiscal policy and hit Italian government debt. These periods typically see EUR/CHF under pressure. As above, we think the SNB may tolerate EUR/CHF down near 0.95 during 2024 while it is still concerned with 2%+ inflation. Into 2025, however, Swiss CPI should be dropping below 2% and the SNB will be more open to listening to Swiss exporters that the Swiss franc is too strong. 2025 is our preliminary estimate for when EUR/CHF turns higher.

EUR/SEK: Obstacles remain for a long-awaited decline

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/SEK | 11.56 | Bearish | 11.65 | 11.50 | 11.30 | 11.10 | 11.00 |

FX hedging sales aren’t key. The pace at which the Riksbank has conducted FX hedging operations has put them on track to complete the programme (USD8bn, EUR2bn) in the shortest possible window: four months. That means the bank has a rather restricted room to materially increase SEK purchases, if indeed one of their goals is to prevent SEK sell-offs, and unless SEK is driven higher by other factors in the next couple of months. There is some scope to speed up EUR (but not USD) sales, although some of those sales are done via the EU payments channel that may not be as impactful as FX swaps in moving the exchange rate. In practice, if the Riksbank wants to drive SEK sustainably and substantially higher via FX sales, it needs to increase the size of the programme. For now, FX hedging is a relatively marginal factor for EUR/SEK, and can only help limit short-term upside into 2024.

Overvaluation versus economic slack. EUR/SEK is approximately 8% overvalued in real terms, according to our medium-term BEER model. The path for a reconnection of the krona with its better fundamentals is obstructed not only by the uncertain outlook for pro-cyclical currencies in a high-rates environment, but also by idiosyncratic weakness in the Swedish economic outlook. The fears of a real estate collapse have subsided of late, but we probably haven’t seen the bottom in the house price correction. Growth will remain very soft at least until mid-2024 and the risk of recession is high. Inflation is receding at a slow pace, meaning high rates for longer, to which Swedish households are significantly exposed to.

Riksbank to pick inflation battle over growth. We expect one more hike by the Riksbank before year-end. This should be the last one of the cycle, but we see policymakers continue to prioritise the inflation battle over growth concerns. This will be done primarily by keeping a hawkish bias and pushing back against rate cut speculation (which should intensify with sluggish growth figures), even though easing should start with the ECB in the third quarter of 2024. Orthodox and unorthodox attempts to keep supporting the krona will remain part of the script, and we cannot exclude an expansion of the FX hedging programme in 2024. Fed cuts should favour a rotation to activity currencies including SEK, and allow it to cash in on respectable carry and undervaluation. We see EUR/SEK around 11.00 in the second half of 2024.

EUR/NOK: Finally the year of love for the krone?

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/NOK | 11.87 | Bearish | 11.80 | 11.70 | 11.30 | 10.90 | 10.60 |

Big misvaluation. NOK is considerably undervalued in the medium term. Our BEER model shows EUR/NOK is trading around 20% above its real fair value, with the mis-valuation having been exacerbated in recent quarters by a growing terms of trade advantage for NOK. The convergence to the krone’s higher fair value will continue to be slowed by the poor liquidity characters of the currency, which will make it attractive only in an environment where global rates take a decisive turn lower. It is our base case that this will happen from the second quarter onwards in 2024, but we cannot ignore the risk that an extra resilience in the US economy leaves procyclical currencies in a choppier for longer trading environment.

FX purchases to stay high. Norges Bank foreign currency purchases on behalf of the government will remain elevated for most of 2024 in our view. Our commodities team’s view that oil will average $90/bbl next year, and the government’s petroleum tax income forecasts have tended to stay on the optimistic side. Unless policymakers decide to ease tension on the currency with lower FX purchases, we currently estimate the monthly amount to average 1.6bn NOK in 2024. That could hinder the pace of re-appreciation of the krone and exacerbate sell-offs during risk-off phases.

Norges Bank can “out-hawk” the Fed. The krone’s (under-) performance has taken a more central role in monetary policy decisions throughout 2023. Norges Bank normally operates under a rather strict model-based regime, where NOK is one factor along with rates and oil prices. Our economics team has an out-of-consensus dovish call on the Fed in 2024, which implies a sharp decline in global rates and argues for Norges Bank rate cuts. However, NOK may face more headwinds before US data turns (also given high FX purchases), and Norges Bank could see benefits in holding a hawkish stance longer than the Fed to favour a stable NOK recovery after hiking in December of this year. After all, high commodity prices mean Norway’s growth should be among the highest in Europe next year (we forecast 1.2% annualised) and inflation recently rebounded, which grants policymakers room to keep rates tighter for longer. Our base case remains a decline in EUR/NOK below 11.00 before year-end 2024.

EUR/DKK: Intervention to sell DKK unlikely next year

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| EUR/DKK | 7.46 | Neutral | 7.46 | 7.46 | 7.46 | 7.46 | 7.46 |

Low-intervention environment to linger. Danmarks Nationalbank has stepped out of the FX market in 2023, intervening for only DKK13bn (all in January) to weaken DKK this year after selling almost DKK55bn in 2022 and DKK120bn in 2021. A switch at the helm of the DN led to a smaller hike than the ECB in February, which helped relieve pressure from the Bank to keep intervening. EUR/DKK appreciated gradually until reaching central parity at 7.46 in October. The new levels suggest that the chances of DN returning to a high-intervention regime to sell DKK aren’t very high in 2024, especially given our view that EUR/USD will appreciate next year.

How to deal with rate cuts? If anything, interest for DKK as a funding currency could lead to some weakness and DN buying, rather than selling, the krona. Should DKK strength prove persistent – or should DKK appreciate against our predictions – DN will have the chance of adjusting the rate gap with the ECB as rate cycles in Europe start: from the third quarter in our forecasts, but the ECB might move earlier. For now, our call is that DN will mirror ECB moves 1:1 in 2024. While EUR/DKK may trade slightly above the upper-bound of the Bank’s tolerance band, we expect DN will be able to tame FX volatility using only FX intervention.

USD/CAD: Good carry, tricky correlations

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| USD/CAD | 1.37 | Bearish | 1.37 | 1.35 | 1.33 | 1.29 | 1.27 |

Strong correlation with US data. Our core view for 2024 in FX is a US dollar decline across the board, with lower Treasury yields offering a breeding ground for pro-cyclical currencies to rebound. However, the loonie is in a peculiar spot though. Fed easing would come as a consequence of deteriorating US activity data, to which – somewhat unintuitively – USD/CAD has negative correlation. Even when looking at the sensitivity of G10 currencies to US yields in the past six months, the impact on CAD is neutral. At times, CAD has traded as a proxy of US economic sentiment, and in our view that can put it in a disadvantageous spot against other pro-cyclical currencies in the period antecedent to Fed cuts, when US data deteriorates. At the same time, a soft-landing scenario in the US would likely shield CAD more than other high-beta currencies in a higher for longer environment.

Best carry in G10, for now. We see more than one scenario where carry trades become an attractive strategy in 2024. As things stand now, the Canadian dollar has the best risk-adjusted 3-month carry in the G10 space excluding USD. We expect, however, the Bank of Canada to follow the Fed with big rate cuts in 2024: 150bp over the course of the year, around 100bp more than what markets are pricing in. We expect the loonie’s carry advantage to be slightly eroded over the course of the year, even though the structurally lower volatility compared to other high yielders should keep it a good option should markets interest for carry be revamped.

Canada has already landed hard. Our call for large Bank of Canada (BoC) cuts aren’t solely a function of Fed easing. The Canadian economy contracted in the second quarter and growth was zero in July and August, meaning a tangible risk of a technical recession in the third quarter. That said, we expect the growth differential with the US (where we are calling for a recession) to swing in favour of Canada in the first half of 2024. The high exposure of the Canadian economy to the US one will make stagnation the most likely scenario north of the border, but high commodity prices will offer some shield. The BoC could, however, start cutting before the Fed. In two previous instances where the short-term swap rate USD-CAD gap was at the current levels in 2023, USD/CAD was trading below 1.35, so the starting point should be lower. A return to levels below 1.30 by the second half of 2024 remains our base case.

AUD/USD: The cheapest pro-cyclical bet

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| AUD/USD | 0.65 | Bullish | 0.64 | 0.65 | 0.67 | 0.69 | 0.71 |

Risks skewed to a hawkish Reserve Bank of Australia. In November, the RBA hiked by 25bp after a rebound in inflation, bucking the pausing trend among most developed central banks. Markets, however, interpreted the statement as an implicit admission that rates have peaked: we don’t agree, and think there is an underestimated risk the RBA tightens further – even if not our base case. Assuming rates have indeed peaked at 4.35%, the pressure of easing rates from Fed rate cuts should intensify from the second quarter of 2024 onwards. However, we estimate a much smaller package of monetary easing in Australia (50bp) compared to the Fed (150bp), with multiple outside risks of hawkish surprises by the RBA along the path that can help the Aussie dollar recover from the currently deeply undervalued levels. Our BEER model shows medium-term real AUD/USD trading well over 20% below its fair value.

Decent economic outlook. To achieve the RBA’s 2-3% inflation target range, CPI needs to average an increase of almost exactly 0.2% each month, and here is where we see potential dislocations getting in the way of an RBA transition to easing. At the same time, the economic outlook should not deteriorate in Australia as fast as we estimate it will in the US. Less squeeze from rates on the economy compared to other countries, a stabilising real estate story (house prices back on the rise) and elevated commodity export prices should contribute to a respectable 1.6% annual growth rate in 2024. On the commodity side, our strategy team forecasts iron ore (62% Fe) prices to average USD104/t next year, below current levels but in line with the 2022-2023 average and above the 2021 average.

External factors will remain key. While we think the Aussie dollar should have an edge over other pro-cyclical currencies based on domestic factors and sharp undervaluation, external drivers – namely US yields, global risk sentiment and China’s economic outlook – will effectively dictate the big bulk of AUD/USD moves in 2024. Our baseline scenario that sees USD yields falling on the back of US economic underperformance and Fed easing would put currencies that have had so far been penalised by the high rate environment and embed many external negatives like AUD in a very advantageous position. When it comes to China, our estimate for 5.0% growth in 2024 mean that there should be enough gradual rebuilding in optimism to direct market attention towards proxy trades for a recovery in Chinese economic sentiment. AUD is one of our favourite currencies for next year.

NZD/USD: New government, higher rates?

| Spot | Year ahead bias | 4Q23 | 1Q24 | 2Q24 | 3Q24 | 4Q24 | |

|---|---|---|---|---|---|---|---|

| NZD/USD | 0.60 | Bullish | 0.59 | 0.60 | 0.61 | 0.62 | 0.64 |

Kiwi $ should rally in our base-line scenario. The benign outlook we currently forecast for pro-cyclical currencies as the USD declines on Fed easing should see the Kiwi dollar shine from 2Q24 onwards. NZD is not as undervalued as AUD due to New Zealand’s current account deficit (which has widened significantly in the past few quarters), but is still some 12% cheaper than its medium-term fair value in real terms. It is also the highest-yielding currency in G10 after the USD, although it is materially more volatile than other high-yielders like CAD and GBP, meaning that a substantial abatement in FX volatility is likely necessary to boost carry-motivated long positioning on NZD. The kiwi dollar should benefit like AUD from a gradual optimistic rerating of growth expectations in China.

Reserve Bank of New Zealand heading to a remit change? The slowdown in inflation, hiring and wage growth in the third quarter suggest the RBNZ’s next move will be a cut, in our view in the summer of 2024. Uncertainty about the impact of booming migration, big spending from the outgoing government and increasing incidence of extreme weather events are all risks that inflation will prove stickier than expected into the new year. The recent change in government can have big implications for the RBNZ policy. The new coalition will almost surely be led by the National Party, which promised less spending than the previous Labour-led government, but also tax cuts (which are inflationary). More importantly, it had advocated for a change of the RBNZ remit, so that the dual mandate is dropped to focus on a stricter inflation targeting. The remit review normally happens in June, and should it be changed, it could mean higher for longer rates in New Zealand – an NZD positive.

Clouded economic outlook. On the economic side, we are less optimistic on the outlook for New Zealand than for Australia. Higher rates and risks of more persistent inflation mean a tighter grip on households. On the real estate side, the worst of the correction looks past us, but house prices are still 13% below the 2022 peak. We are broadly optimistic on energy commodities in 2024, but New Zealand is a net energy importer and its exports are mostly concentrated in dairy products. Fonterra estimates a moderate downside risks in milk prices next year (mid-point at NZD6.50 – 8/Kg milksolids). Recession is a non-negligible risk in 2024, but whether this will mean a more dovish RBNZ will effectively depend on a remit review: should the new government leave it unchanged, then bigger rates cuts would likely get in the way of a smooth NZD recovery.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

FX Outlook 2024Download

Download article

15 November 2023

FX Outlook 2024: Waiting for the tide to come in This bundle contains 7 Articles