FX Positioning: No clear impact from Russia-Ukraine tensions

CFTC positioning data for the week ending 15 February shows no clear impact from geopolitical tensions in Ukraine, as aggregate USD net-longs continued to inch lower along with JPY net positioning. The pound jumped back into net-long positioning for the first time since November

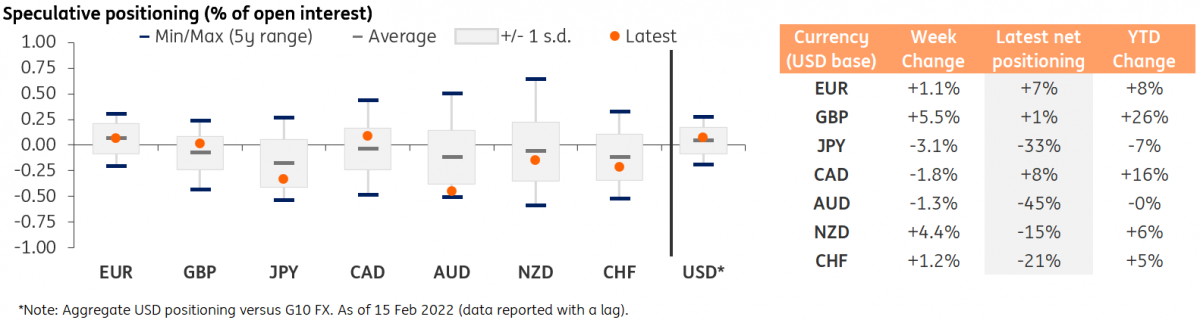

Dollar positioning keeps edging lower

CFTC data on FX positioning shows that the aggregate dollar positioning versus reported G10 currencies (i.e. G9 excluding NOK and SEK) declined for a fifth consecutive week in the seven days to 15 February.

There appears to be no clear impact on positioning from rising geopolitical tensions in Ukraine, as the picture appears quite mixed within the safe-haven and pro-cyclical currency segments. The yen saw another increase in net short positions, which now amount to 33% of open interest, while the Swiss franc faced a marginal short-squeeze. In the commodity space, CAD saw a minor pullback in net-longs, AUD yet another rise in its net shorts (which are considerably overstretched), while NZD experienced a quite material short-trimming, with its positioning now at -15% of open interest.

EUR and GBP longs rise

CFTC does not report on the positioning for NOK and SEK, but the two other reported European currencies EUR and GBP both showed an increase in net positioning in the week ending 15 February.

EUR/USD net positioning has been on a positive run since the start of the year (+8% of open interest YTD) and is currently at the centre of its standard-deviation band with net longs amounting to 7% of open interest. While the recent ECB hawkish turn has provided support to the euro, we think that the current positioning data is another indication of how markets have not priced a considerable amount of geopolitical risk into EUR/USD, leaving it quite vulnerable to further escalations in Russia-Ukraine tensions.

The pound recorded the biggest increase in net positioning in the reference week (+5.5% of open interest) with long positions exceeding short positions for the first time since November 2021. This is clearly a sign of how the Bank of England’s plans to front-load rate hikes has translated into some solid support to the currency, even in spite of a deteriorating global risk environment.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more