FX Positioning: New year’s reshuffle

At the start of the new year speculative investors curtailed their dollar longs, to the benefit of both low and high-yielders. Latest data show that AUD is now the biggest short and CAD the biggest long in G10. The rise in GBP net longs suggests more downside risk to sterling if the Bank of England cuts rates

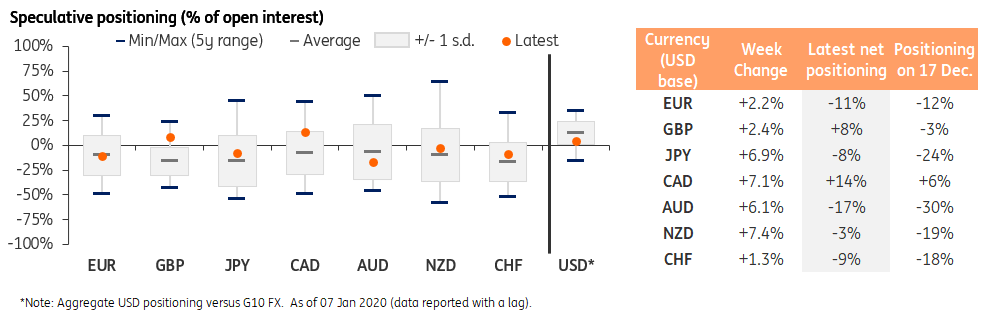

Dollar losing its crown

The CFTC’s Commitment of Traders (COT) report covering the week ending 7 January is displaying a very different G10 market positioning as opposed to late-2019 data.

Primarily, speculators have trimmed their long dollar positions at the start of the new year, in a dynamic that reflects the fall in USD spot in the last days of December. It appears that the re-allocation of speculative positions has benefitted in almost equal shares the low and high-yielders. Figure 1 provides a snapshot of the current G10 positioning compared with the 17 December report.

Figure 1 - FX positioning overview

EUR flat, JPY & CHF run despite Iran

In line with a narrative we are now accustomed to, the euro remains unable to fully cash in on any dollar weakness. We see such dynamics mostly related to the still grim Eurozone economic outlook that is convincing investors rates in the common area will remain depressed for long. The stubbornly flat positioning is reflecting the drop in EUR/USD volatility with both the implied and realised gauges now close to historical lows across most tenors.

The positioning measures on the other low-yielders JPY and CHF, instead, fiercely moved towards the neutral territory, after a prolonged period stationing in the “oversold” area. It appears that speculative investors did not rush to sell safe-haven currencies on the back of the tensions that erupted in Iran earlier this month. At -8% and -9% of open interest, respectively, JPY and CHF net positioning are at their highest since autumn.

However, we may see some correction next week in JPY positioning as the currency kept dropping (it is now approaching 110 vs the USD) in the days following the latest CFTC report.

NZD shorts in free fall, AUD & CAD on opposite sides

Up until a few weeks back, our FX positioning reviews were all about the Kiwi dollar extensive net short positioning, after the gauge touched -56% (of open interest) in late October and stayed in deeply negative territory throughout November and December. As investors curtailed their long USD positions in the past few weeks (Figure 2), it is no surprise the NZD appeared as a valid alternative to reallocate their bullish views.

The RBNZ neutral shift late last year is offering a supportive rate environment compared to its main peer AUD and a medium-term undervaluation still points at upside potential as long as a benign risk environment holds. At this stage, we do not exclude NZD moving into positive territory in the near future.

Figure 2 - NZD net positioning on the rise

The Australian dollar also saw its net shorts being trimmed (from -30% of o.i. in mid-December to -17% as of 07 January), but not enough to avoid the label of biggest G10 short. The bushfire emergency ongoing in Australia (in tandem with the prospect of RBA easing) is likely going to keep appetite for the currency subdued and AUD shorts solidly in place for a bit longer.

The Canadian dollar remains on top of the G10 positioning ranking (+14% of open interest) and has consolidated its status after markets pared most BoC easing expectations and oil climbed on the back of Iran tensions. The subsequent drop in crude prices should be reflected in next week’s CFTC report and a correction in CAD net positions may be in the cards.

GBP in positive territory, for now

Like NZD, sterling has recovered from a period of deep net-short positioning thanks to an intense repricing of Brexit-related uncertainty. The GBP positioning measure (+8% of o.i.) is at its highest since May 2018 and (as shown in Fig. 1) moved outside its 5Y 1 s.d. range. The gauge may however face a correction in the next CFTC report after some comments by BoE officials triggered a rise in rate cut expectations and put pressure on sterling.

In perspective, a neutral/mildly-positive GBP positioning suggests a higher downside potential for the currency should the BoE eventually take steps to ease monetary policy.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article