FX Positioning: More USD long squeeze before Fed-induced rally

CFTC data as of 25 January show that the net aggregate dollar positioning vs G10 dropped to the lowest since September. This suggests that the dollar benefitted from a more balanced positioning into the FOMC 26 January meeting, which led to widespread USD gains

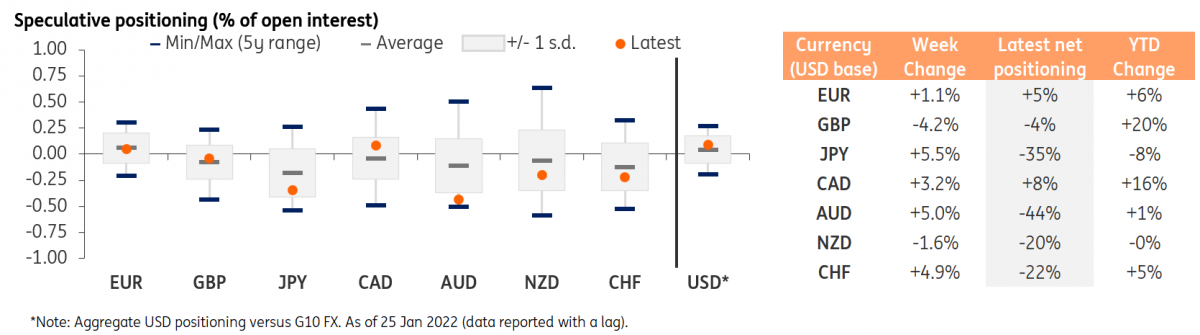

Dollar positioning more balanced before Fed meeting

CFTC data show that the dollar’s net speculative positioning versus reported G10 currencies (i.e. G9 excluding NOK and SEK) continued to decline in the week ending 25 January, despite the greenback rebounding across the board in the spot/future market.

This appears to be a case of positioning data being detached/lagging market moves, but it likely indicates that the market had a more balanced (i.e. less overbought) positioning on the dollar heading into the FOMC 26 January meeting. That ultimately allowed some sizeable room for dollar longs to be built back on the back of Chair Powell’s hawkish message: the size of that jump in net positioning will emerge in the next couple of CFTC COT reports, and will provide some indication of whether the dollar rally is now looking overstretched from a technical perspective.

All G10 currencies' positioning rose except for GBP and NZD

EUR/USD positioning rose to 5% of open interest: while not qualifiable as “overbought”, that was the highest level recorded since August 2021. The other low-yielders, JPY and CHF, both experienced some sizeable short-squeeze, although they both remained deep into oversold territory.

The most oversold G10 currency, AUD, experienced a short trimming worth around 5% of open interest, but likely saw another sharp rise in shorts in the week after. CAD continued to advance into marginally overbought territory, which likely contributed to the loonie’s weakness in the past few days.

GBP and NZD were the only two G10 currencies that saw their net positioning drop in the week ending 25 January, although there were no clear drivers behind such moves (the data flow in the UK and New Zealand was quite supportive for the local currencies).

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article