FX Positioning: Broad position-squaring

CFTC data shows that in the week ending 07 December, G10 currencies experienced some widespread position squaring as USD longs were unwound across the board. The overbought NZD was the only currency seeing a decline in its net positioning. GBP shorts kept consolidating on falling BoE rate hike bets

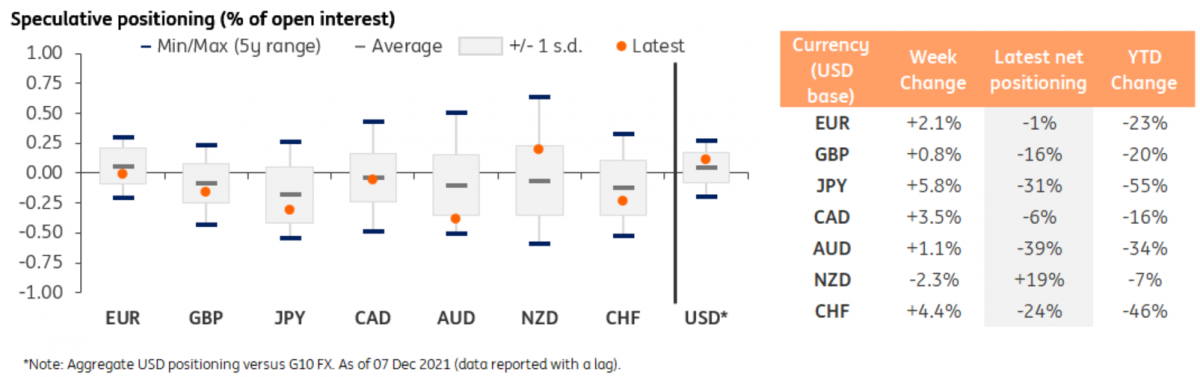

USD net-longs decline

CFTC positioning data indicates that the week ending 07 December coincided with a broad re-balancing in G10 positioning, with speculative markets unwinding some of their widespread net-long positions against the dollar. The net aggregate USD positioning against reported G10 currencies (i.e. G9 excluding NOK and SEK) declined after having climbed to October highs in the previous week.

USD net-longs are now worth 11% of open interest, according to our calculations. As shown in the table below, this level is above the 5-year average but still within the 1-standard-deviation band. All reported G10 currencies’ positioning (in percentage of open interest) were within their 1-standard-deviation ranges last week.

Major short-squeeze in JPY; GBP shorts consolidate

The dynamics shown in the data were not fully in line with spot changes, and may instead display some earlier moves which had not been previously reported due to the Thanksgiving holiday. EUR/USD positioning corrected higher by 2% of open interest and is now in neutral territory.

The widest change in positioning was recorded in JPY, where the short-squeeze was worth nearly 6% of open interest, bringing the net-positioning value close to its 5-year average. That mirrors (with a lag) the adverse impact of the Omicron variant on risk appetite which triggered a significant unwinding of JPY shorts. While still in net-short territory, there is now clearly less room for the yen to benefit from position squaring.

The other low-yielding safe-haven in G10, CHF, also saw a major unwinding of short positions. The pound’s net shorts decreased only marginally, showing some consolidation of bearish sentiment on the currency as Bank of England rate hike bets for the December meeting were scaled back. GBP positioning may not appear overstretched to the oversold side in the chart above (only slightly below its 5-year average), but we must remember that in recent years there was an unnatural tendency for speculators to stay short sterling given the many periods of Brexit-related risk. While some Brexit/trade tension risk has re-emerged recently, there is no indication that the FX market is building a Brexit-related risk premium into GBP, suggesting this was not a major factor behind the recent increase in GBP shorts.

CAD positioning normalises; NZD remains overbought

In the commodity FX space, CAD positioning likely benefitted from rising hawkish expectations ahead of the Bank of Canada meeting on 8 December, which then led to a marginally negative reaction in the loonie after the rate announcement.

AUD saw a contained short-squeeze and remained the most oversold currency in G10. We expect, however, to see evidence of a more significant unwinding of AUD net shorts in the next report, which should help explain the recent outperformance of the currency.

As part of the broad position-squaring event, the only overbought G10 currency, NZD, faced a deterioration in its net positioning versus the USD. While still significantly overbought (+19% of open interest), particularly considering the strong-USD environment, the Kiwi dollar’s positioning indicator was back within its 1-standard-deviation band. Last week’s NZD underperformance relative to its closest peer AUD is, in our view, due to the stark divergence in the two currencies’ positioning.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article