FX Positioning: A risk-on mirror

In the week 30 Oct/05 Nov, speculative investors have tried to capitalise on the supported global risk sentiment, betting on cyclical currencies whilst adding some shorts in low yielders. The positioning short squeeze in AUD was particularly pronounced

Big short-squeeze in AUD

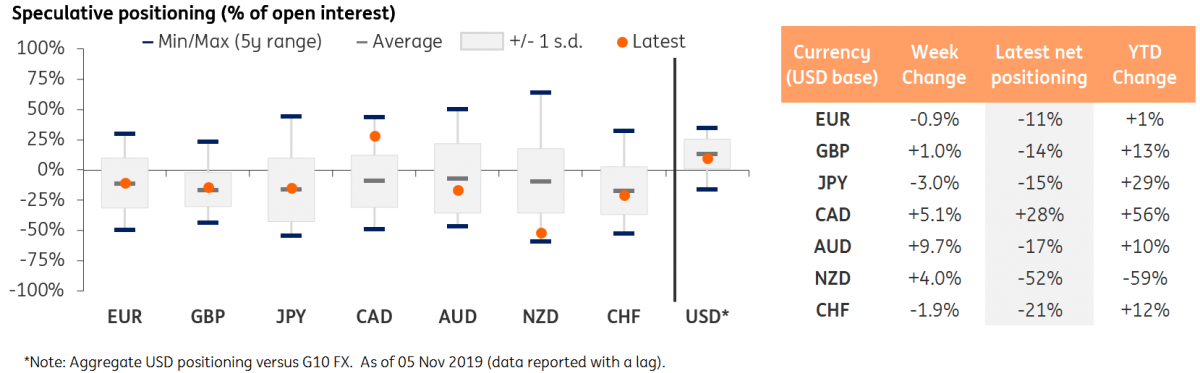

According to CFTC data for the week, 30 October - 05 November (summary in Fig. 1) show how speculative positioning in the G10 space moved largely in line with the overall supported risk-environment.

The three pro-cyclical currencies (CAD, AUD and NZD) all saw some speculative longs added/shorts removed, with the Aussie dollar leading the pack: AUD net positions saw a change of +9.7% of open interest (from -26% to -17%). Such variation is consistent with the positive week for AUD in the spot market (+0.4%) and is likely the consequence of the Reserve Bank of Australia's upbeat tone at the 5 November meeting, that fuelled expectations of a more extended pause in the Bank’s easing cycle.

Fig. 1 - G10 FX positioning overview

Elsewhere, the short-squeezing in NZD was more marginal (+4%), which leaves the net positioning still deep into short territory (-52% of open interest, the biggest G10 short). The speculative market still appears quite reluctant to bet on a risk-on-fuelled rebound in NZD, which is likely due to the uncertainty around the RBNZ monetary policy path. Markets are currently pricing in a 60% probability that the Bank will cut rates this Wednesday but (as highlighted in our preview: “One more cut from New Zealand’s central bank?”) we lean slightly in favour of a hold, which may prompt a more sizeable squaring in NZD shorts.

The third commodity currency, CAD, continues to see net long speculative positions being added (now piling up to 28% of open interest, the biggest long in G10), quite surprisingly given that the reference period covers the Bank of Canada meeting (30 Oct), that was universally seen as a dovish tilt in the Bank’s neutral policy stance.

According to such dynamic, we would not be surprised to see CAD positioning holding up fairly well even in next week's CFTC report, that will cover the disappointing Canadian payrolls released last Friday.

Tentatively adding shorts in funding currencies

Global risk sentiment has continued to benefit from the optimistic news flow about the Sino-American trade relationships over the last two weeks. However, markets did not rush away from G10 safe-havens as demonstrated too by the relatively small decrease (compared to the high-yielders) in JPY and CHF net positioning.

EUR/USD net speculative positions retracted marginally (-0.9% of open interest) into deeper negative territory and now amount to -11% of open interest. Latest dynamics in euro positioning tend to endorse the notion that the EUR is cementing its role as one of the preferred funding currencies, hence moving broadly in line with the other low-yielders JPY and CHF. Accordingly, we expect a continued resilience in risk sentiment as unlikely to aid any short-squeezing effect on EUR/USD.

Elsewhere, GBP positioning remained broadly stable around its 5-year average, signalling market’s wait-and-see approach ahead of the UK elections on December 12th. Investors seem to be pricing in a Conservative majority as the base-case scenario, which is widely seen as a market-friendly outcome. Accordingly, should the risk of a hung parliament start to emerge from the polls, another rise in GBP shorts may be on the cards.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article