Dollar weighed down by better alternatives and intervention

- 30 January

- FX

January has proved a soft month for the dollar. Bullish sentiment on the global economy continues to challenge the US exceptionalism narrative, while geopolitics, fiscal risks and now the threat of joint FX intervention are all hitting the dollar, too. Our preference remains for a broader dollar sell-off occurring later in the year

Dollar at its lows

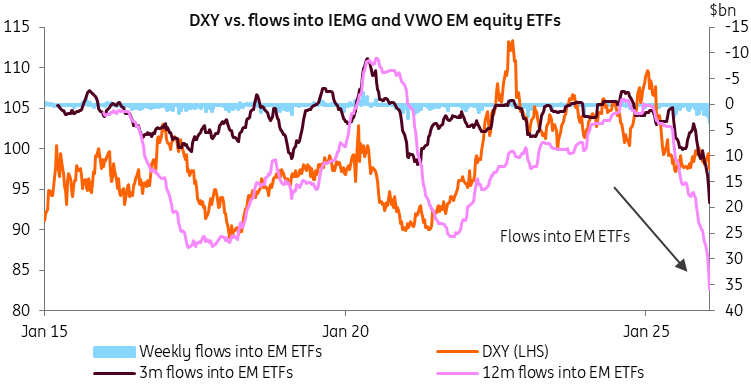

The DXY dollar index is ending January at its multi-quarter lows. We see several factors driving this trend. The first is the global investment environment. Investors certainly have a glass half-full view of global growth prospects this year. This is good news for both commodity exporting economies and emerging markets in general. In fact, we are starting to see some of the strongest cumulative portfolio flows to emerging markets in over a decade. Typically, money being put to work in emerging markets comes at the expense of the dollar. This trend looks set to continue.

Strong flows into emerging markets normally weigh on the dollar

The second is the uncertain political environment in the US. One takeaway from the Greenland turmoil and the equity sell-off was that the dollar struggled to demonstrate any safe-haven properties. While we doubt international investors will make wholesale changes to geographic portfolios based on politics alone, the uncertainty has inserted a little more risk premium into the dollar. However, the European buyside looks like it has more appropriate FX hedge ratios on US assets than it had before April last year. We cannot see increased hedging being worth another 10% drop in the dollar.

Another factor is the fiscal risk profile. Here Japan’s JGB sell-off hit both US Treasuries and UK Gilts and led to pressure on all three currencies. This factor will be with us all year. And finally, it seems like Japanese authorities – perhaps with the US too – have lost patience with the rise in USD/JPY and the instability it was causing for bond markets. Japan has the capacity to deploy up to $100bn in FX intervention, while any confirmation of US participation – which would mark the first joint action since 2011 – would really register on the market’s psyche.

The path ahead

We are bearish on the dollar this year on the back of declining rate differentials and some genuine growth opportunities outside of the US – including Europe. In the short term, however, the US economy is holding up well, Federal Reserve rate cuts look to be delayed, and high energy prices will be weighing on the terms of trade in Europe and Asia. Additionally, and as impressive as any joint US-Japan intervention is, USD/JPY fundamentals have yet to turn. Here, we can see intervention turning into a passive campaign in the 155-160 area with decreasing marginal returns.

Our preference is that EUR/USD can continue to trade in a broad 1.16-19 range through the first quarter. February is typically a seasonally positive month for the dollar and the US macro environment may prove more supportive. We then have EUR/USD moving up through 1.20 through late summer to a modest end-year target of 1.22. A sharp break-up through 1.20 in the first quarter would be a surprise. For USD/JPY, investors will be wary of a repeat of the 10-12% drop seen in the summer of 2024. Failure of the LDP to gain a majority at the 8 February election or prospects of a much earlier Bank of Japan rate hike could add momentum to such a move.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s Arnold moment – why strategy over spectacle matters

- This bundle contains 15 Articles